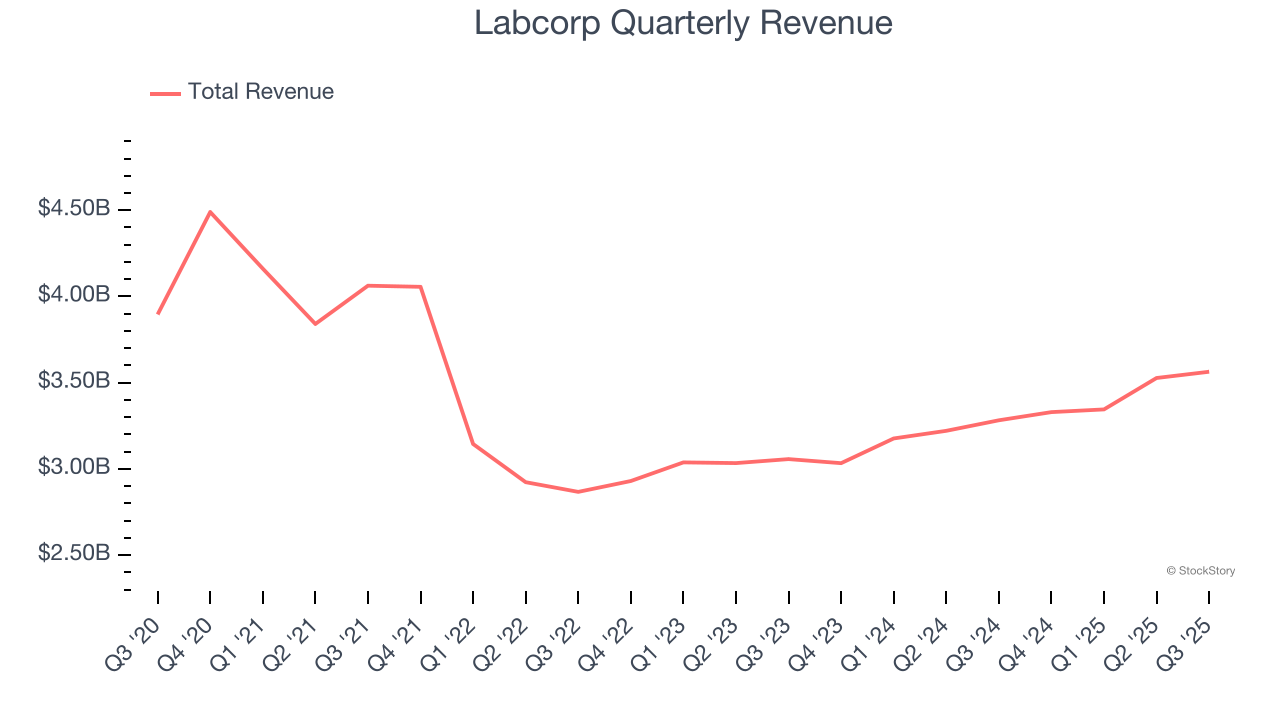

Healthcare diagnostics company Labcorp Holdings (NYSE:LH) met Wall Street’s revenue expectations in Q3 CY2025, with sales up 8.6% year on year to $3.56 billion. Its non-GAAP profit of $4.18 per share was 1% above analysts’ consensus estimates.

Is now the time to buy Labcorp? Find out by accessing our full research report, it’s free for active Edge members.

Labcorp (LH) Q3 CY2025 Highlights:

- Revenue: $3.56 billion vs analyst estimates of $3.56 billion (8.6% year-on-year growth, in line)

- Adjusted EPS: $4.18 vs analyst estimates of $4.14 (1% beat)

- Adjusted EBITDA: $596.8 million vs analyst estimates of $605.1 million (16.7% margin, 1.4% miss)

- Management slightly raised its full-year Adjusted EPS guidance to $16.33 at the midpoint

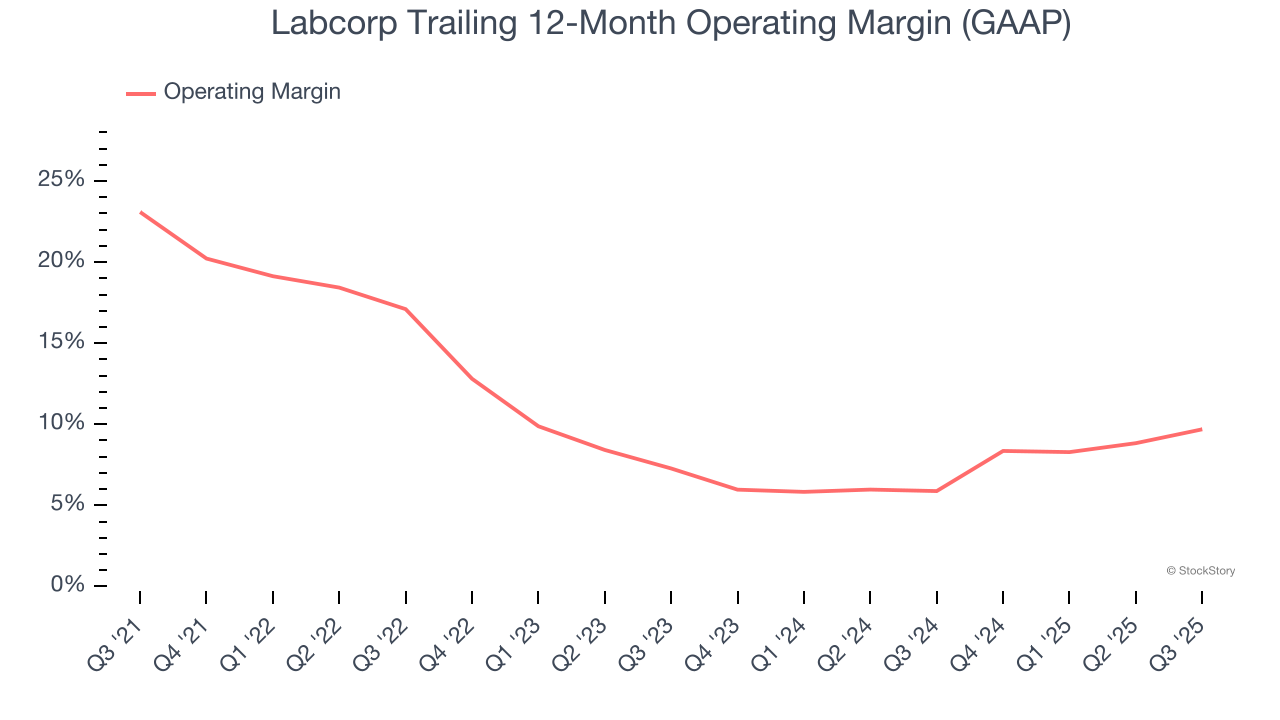

- Operating Margin: 11.1%, up from 7.7% in the same quarter last year

- Free Cash Flow Margin: 7.9%, up from 4.9% in the same quarter last year

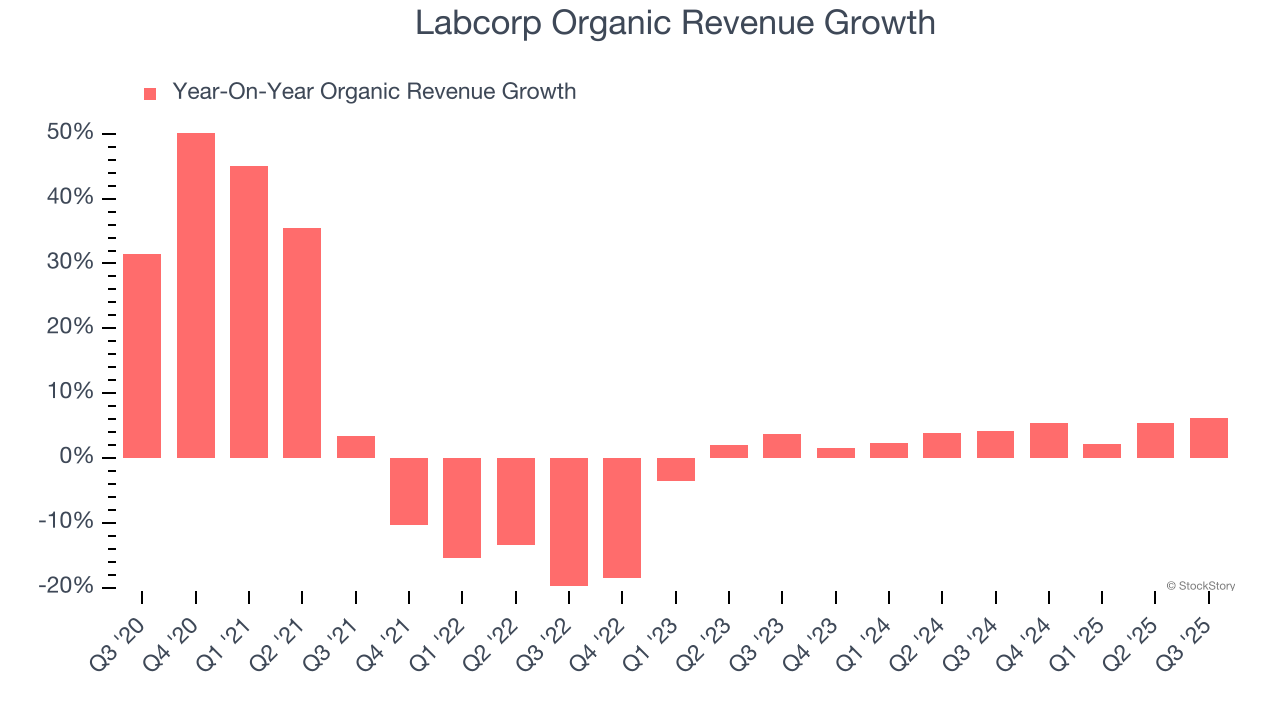

- Organic Revenue rose 6.2% year on year vs analyst estimates of 5.2% growth (95.4 basis point beat)

- Market Capitalization: $22.91 billion

"Labcorp's third-quarter performance reflects continued momentum in our Diagnostics and Central Laboratory businesses, resulting in strong revenue growth and margin improvement," said Adam Schechter, Chairman and CEO of Labcorp.

Company Overview

With over 600 million tests performed annually and involvement in 90% of FDA-approved drugs in 2023, Labcorp (NYSE:LH) provides laboratory testing services and drug development solutions to doctors, hospitals, pharmaceutical companies, and patients worldwide.

Revenue Growth

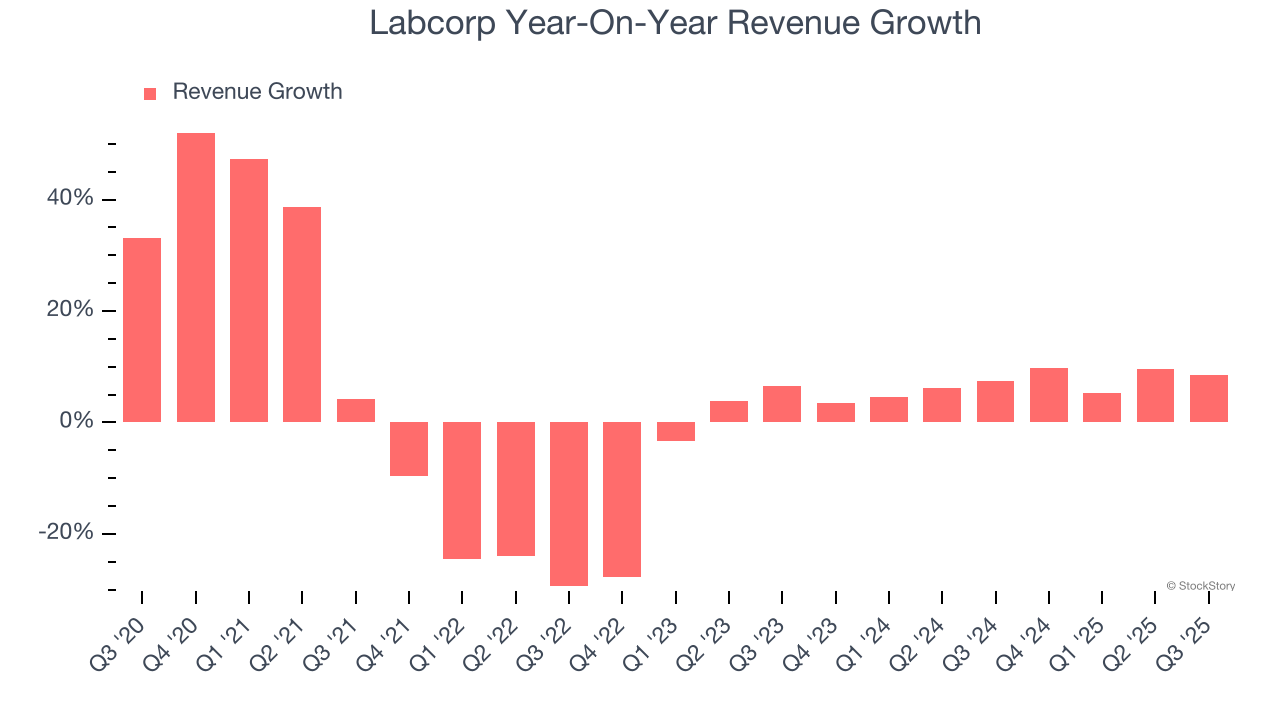

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Labcorp’s 2% annualized revenue growth over the last five years was tepid. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Labcorp’s annualized revenue growth of 6.8% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Labcorp’s organic revenue averaged 3.9% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Labcorp grew its revenue by 8.6% year on year, and its $3.56 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, similar to its two-year rate. We still think its growth trajectory is satisfactory given its scale and indicates the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Labcorp has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 13.2%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Labcorp’s operating margin decreased by 13.4 percentage points over the last five years, but it rose by 2.4 percentage points on a two-year basis. Still, shareholders will want to see Labcorp become more profitable in the future.

In Q3, Labcorp generated an operating margin profit margin of 11.1%, up 3.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

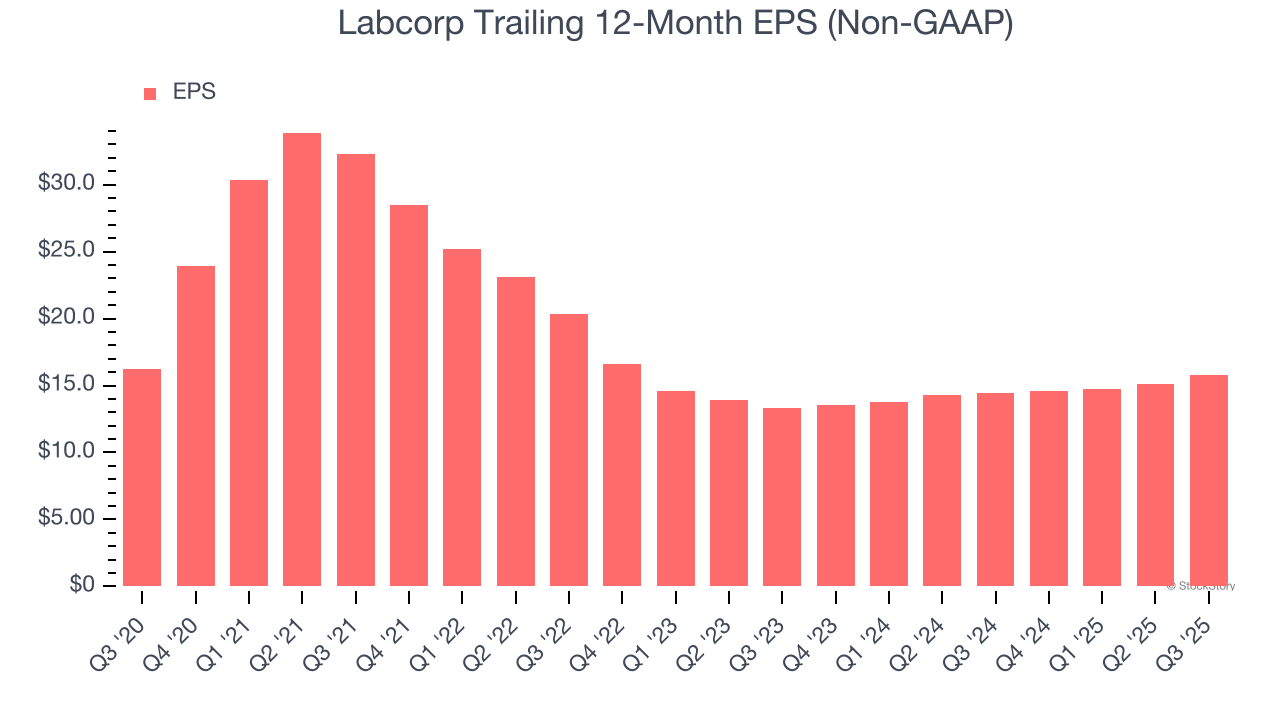

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Labcorp’s flat EPS over the last five years was below its 2% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Labcorp’s earnings to better understand the drivers of its performance. As we mentioned earlier, Labcorp’s operating margin expanded this quarter but declined by 13.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Labcorp reported adjusted EPS of $4.18, up from $3.50 in the same quarter last year. This print beat analysts’ estimates by 1%. Over the next 12 months, Wall Street expects Labcorp’s full-year EPS of $15.82 to grow 8.8%.

Key Takeaways from Labcorp’s Q3 Results

It was good to see Labcorp narrowly top analysts’ organic revenue expectations this quarter. Full-year EPS was slightly raised. Zooming out, we think this was a decent quarter. The market seemed to be hoping for more, and the stock traded down 2.4% to $269 immediately following the results.

Is Labcorp an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.