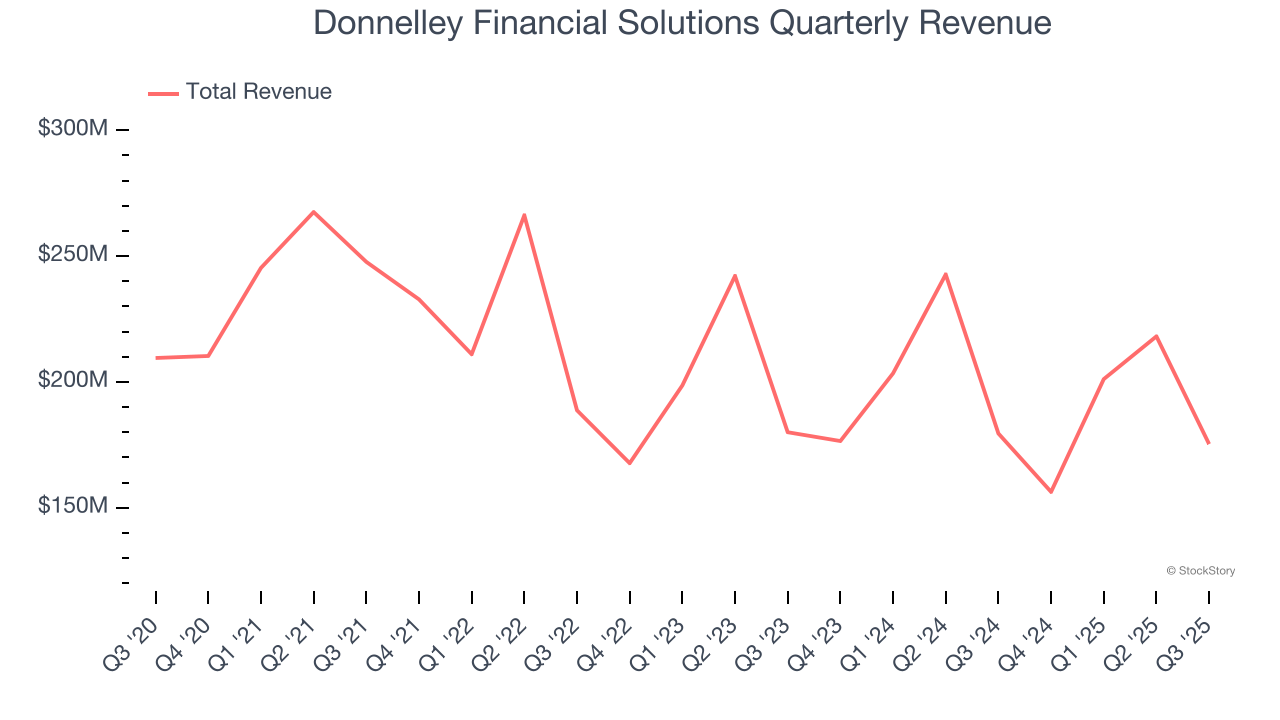

Financial regulatory software provider Donnelley Financial Solutions (NYSE:DFIN) reported Q3 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 2.3% year on year to $175.3 million. On the other hand, next quarter’s revenue guidance of $155 million was less impressive, coming in 6.3% below analysts’ estimates. Its non-GAAP profit of $0.86 per share was 50% above analysts’ consensus estimates.

Is now the time to buy Donnelley Financial Solutions? Find out by accessing our full research report, it’s free for active Edge members.

Donnelley Financial Solutions (DFIN) Q3 CY2025 Highlights:

- Revenue: $175.3 million vs analyst estimates of $169.7 million (2.3% year-on-year decline, 3.3% beat)

- Pre-tax Profit: -$57.9 million (-33% margin, 476% year-on-year decline)

- Adjusted EPS: $0.86 vs analyst estimates of $0.57 (50% beat)

- Revenue Guidance for Q4 CY2025 is $155 million at the midpoint, below analyst estimates of $165.4 million

- Market Capitalization: $1.42 billion

Company Overview

Born from the need to navigate increasingly complex financial regulations in the digital age, Donnelley Financial Solutions (NYSE:DFIN) provides software and technology-enabled services that help companies comply with SEC regulations and manage financial transactions and reporting requirements.

Revenue Growth

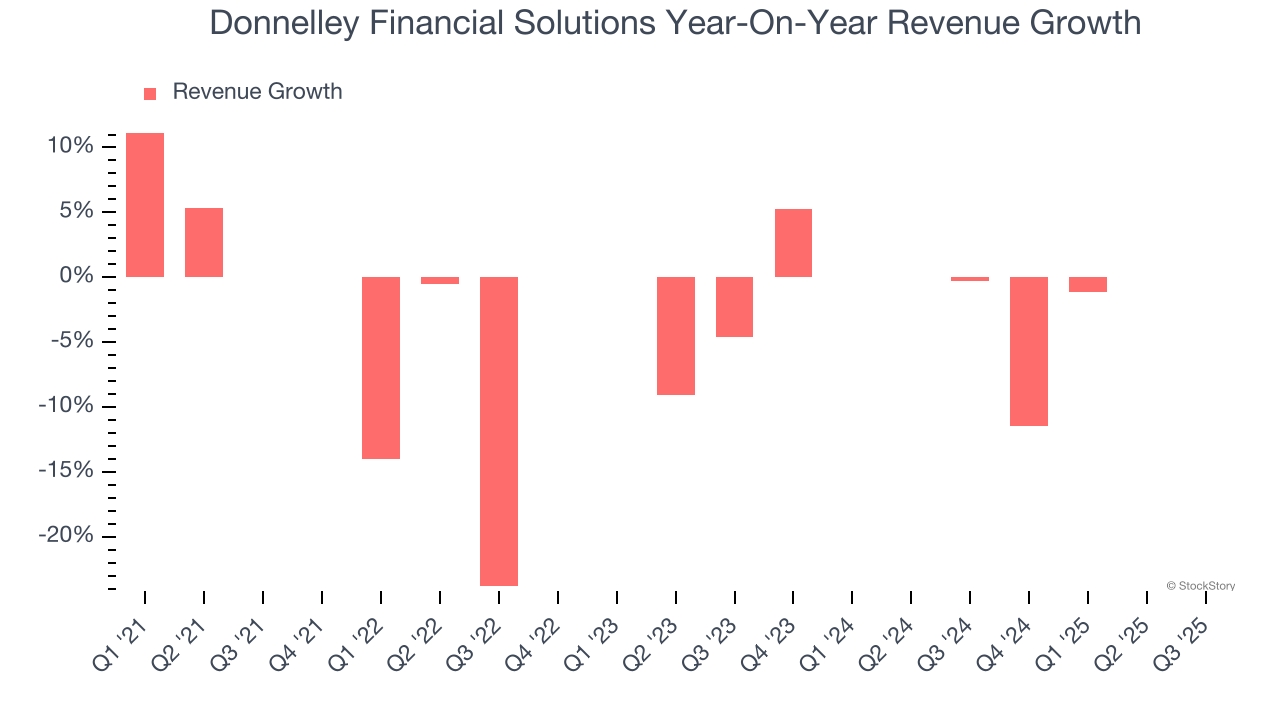

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Donnelley Financial Solutions’s demand was weak over the last five years as its revenue fell at a 2.8% annual rate. This wasn’t a great result and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Donnelley Financial Solutions’s annualized revenue declines of 2.4% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Donnelley Financial Solutions’s revenue fell by 2.3% year on year to $175.3 million but beat Wall Street’s estimates by 3.3%. Company management is currently guiding for flat sales next quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Key Takeaways from Donnelley Financial Solutions’s Q3 Results

It was good to see Donnelley Financial Solutions beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $51.70 immediately following the results.

Big picture, is Donnelley Financial Solutions a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.