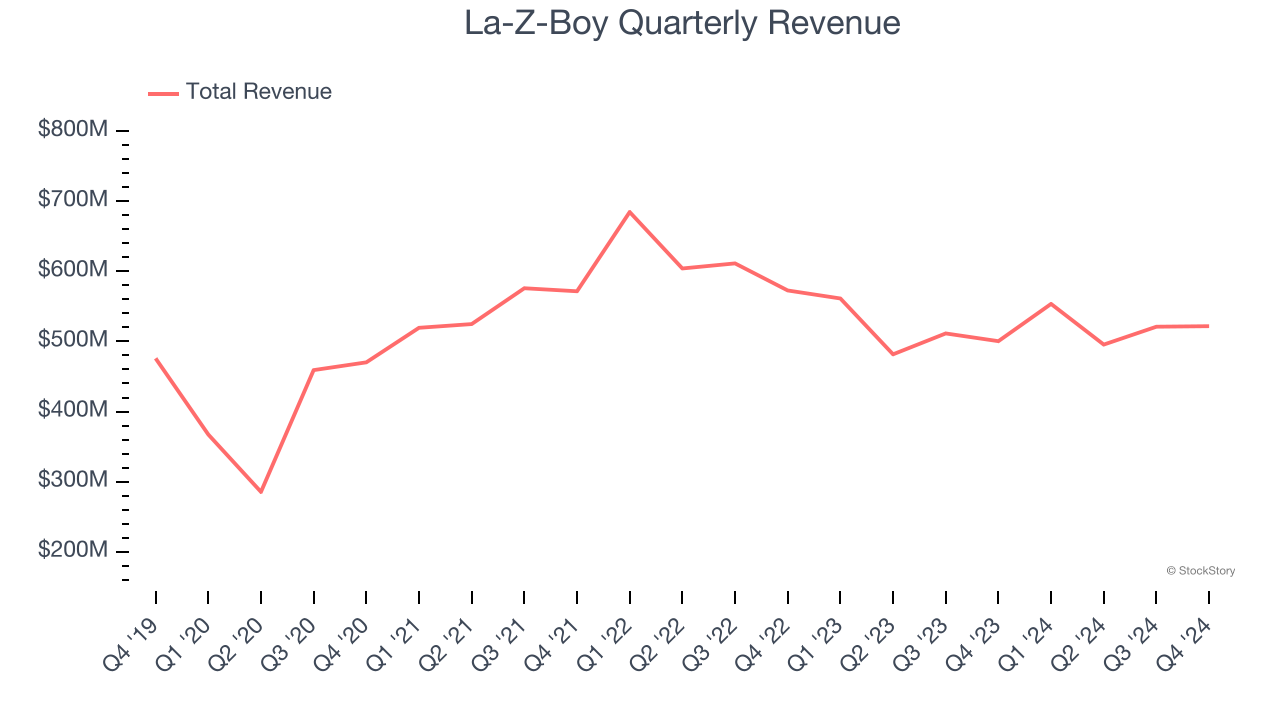

Furniture company La-Z-Boy (NYSE:LZB) announced better-than-expected revenue in Q4 CY2024, with sales up 4.3% year on year to $521.8 million. On the other hand, next quarter’s revenue guidance of $555 million was less impressive, coming in 1.6% below analysts’ estimates. Its non-GAAP profit of $0.68 per share was 2% above analysts’ consensus estimates.

Is now the time to buy La-Z-Boy? Find out by accessing our full research report, it’s free.

La-Z-Boy (LZB) Q4 CY2024 Highlights:

- Revenue: $521.8 million vs analyst estimates of $515.8 million (4.3% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.68 vs analyst estimates of $0.67 (2% beat)

- Revenue Guidance for Q1 CY2025 is $555 million at the midpoint, below analyst estimates of $563.9 million

- Operating Margin: 6.7%, in line with the same quarter last year

- Free Cash Flow Margin: 7.3%, similar to the same quarter last year

- Market Capitalization: $1.85 billion

Melinda D. Whittington, Board Chair, President and Chief Executive Officer of La-Z-Boy Incorporated, said, “Our third quarter results reflect the steady progress we have made to build a more agile business, create our own momentum, and drive growth in what is still a challenged environment. We delivered sales growth across each of our segments, punctuated by strong Retail same-store sales. This was driven by solid conversion rates, average ticket, and design sales, all of which improved again year-over-year. Additionally, within our Wholesale segment, our core North America La-Z-Boy brand continues to post sales growth and margin expansion. Our vertically integrated model reinforces the unique strength of our iconic brand and positions us to disproportionately benefit when the market rebounds. We are a trusted solution for a growing number of consumers and will remain steadfast in our mission of bringing the transformational power of comfort to people, homes, and communities.

Company Overview

The prized possession of every mancave, La-Z-Boy (NYSE:LZB) is a furniture company specializing in recliners, sofas, and seats.

Home Furnishings

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

Sales Growth

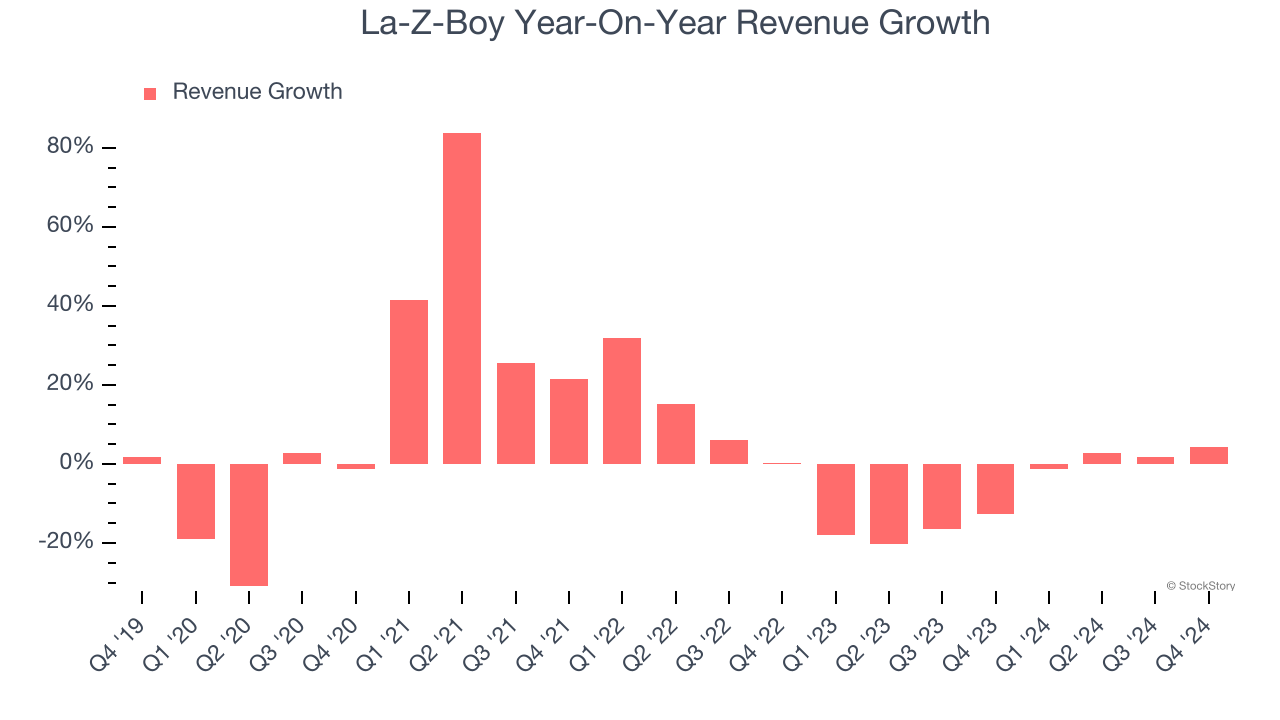

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, La-Z-Boy’s sales grew at a sluggish 3.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. La-Z-Boy’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8% annually.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Wholesale and Retail, which are 61.5% and 38.5% of core revenues. Over the last two years, La-Z-Boy’s Wholesale revenue (sales to retailers) averaged 9% year-on-year declines while its Retail revenue (direct sales to consumers) averaged 4.4% declines.

This quarter, La-Z-Boy reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 1.2%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

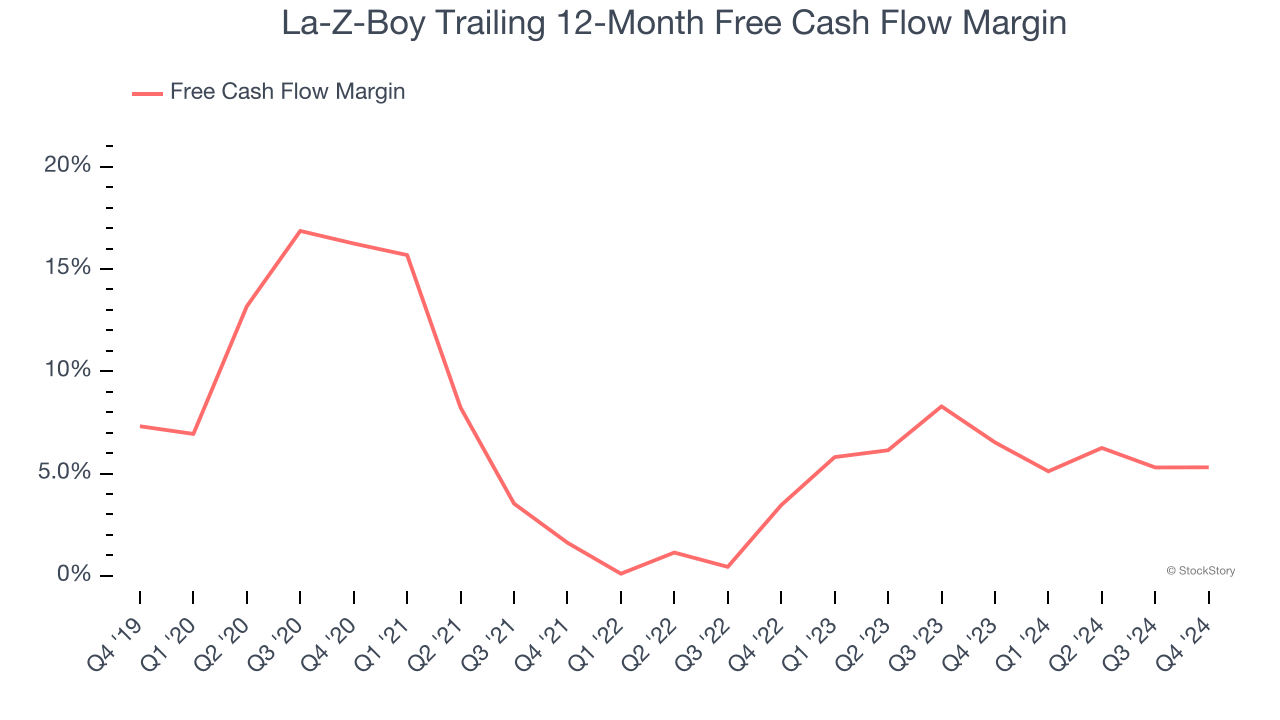

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

La-Z-Boy has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.9%, subpar for a consumer discretionary business.

La-Z-Boy’s free cash flow clocked in at $38.25 million in Q4, equivalent to a 7.3% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

Over the next year, analysts’ consensus estimates show they’re expecting La-Z-Boy’s free cash flow margin of 5.3% for the last 12 months to remain the same.

Key Takeaways from La-Z-Boy’s Q4 Results

It was good to see La-Z-Boy narrowly top analysts’ revenue expectations this quarter. We were also happy its Retail revenue narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed. Overall, this quarter was mixed. The stock remained flat at $45 immediately after reporting.

Is La-Z-Boy an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.