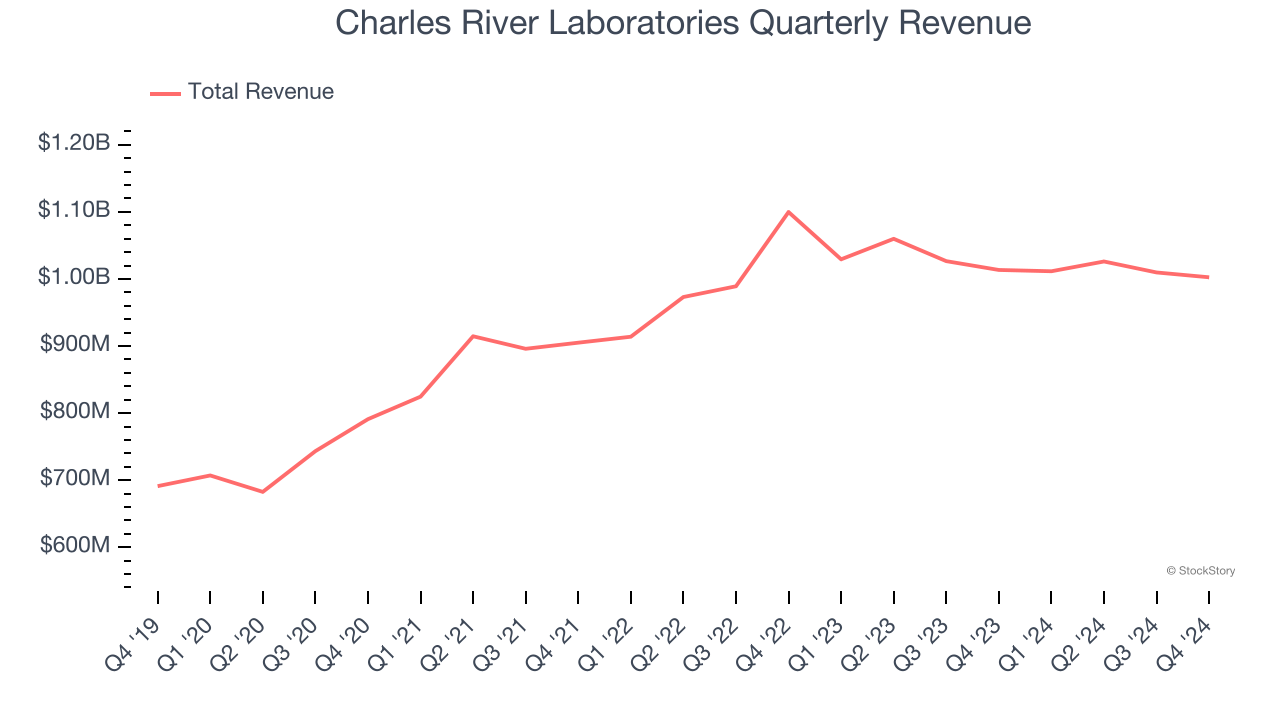

Lab services company Charles River Laboratories (NYSE:CRL) reported Q4 CY2024 results exceeding the market’s revenue expectations, but sales fell by 1.1% year on year to $1.00 billion. Its non-GAAP profit of $2.66 per share was 5.1% above analysts’ consensus estimates.

Is now the time to buy Charles River Laboratories? Find out by accessing our full research report, it’s free.

Charles River Laboratories (CRL) Q4 CY2024 Highlights:

- Revenue: $1.00 billion vs analyst estimates of $979.9 million (1.1% year-on-year decline, 2.3% beat)

- Adjusted EPS: $2.66 vs analyst estimates of $2.53 (5.1% beat)

- Adjusted EBITDA: -$48.35 million vs analyst estimates of $244.6 million (-4.8% margin, significant miss)

- Adjusted EPS guidance for the upcoming financial year 2025 is $9.35 at the midpoint, missing analyst estimates by 4.1%

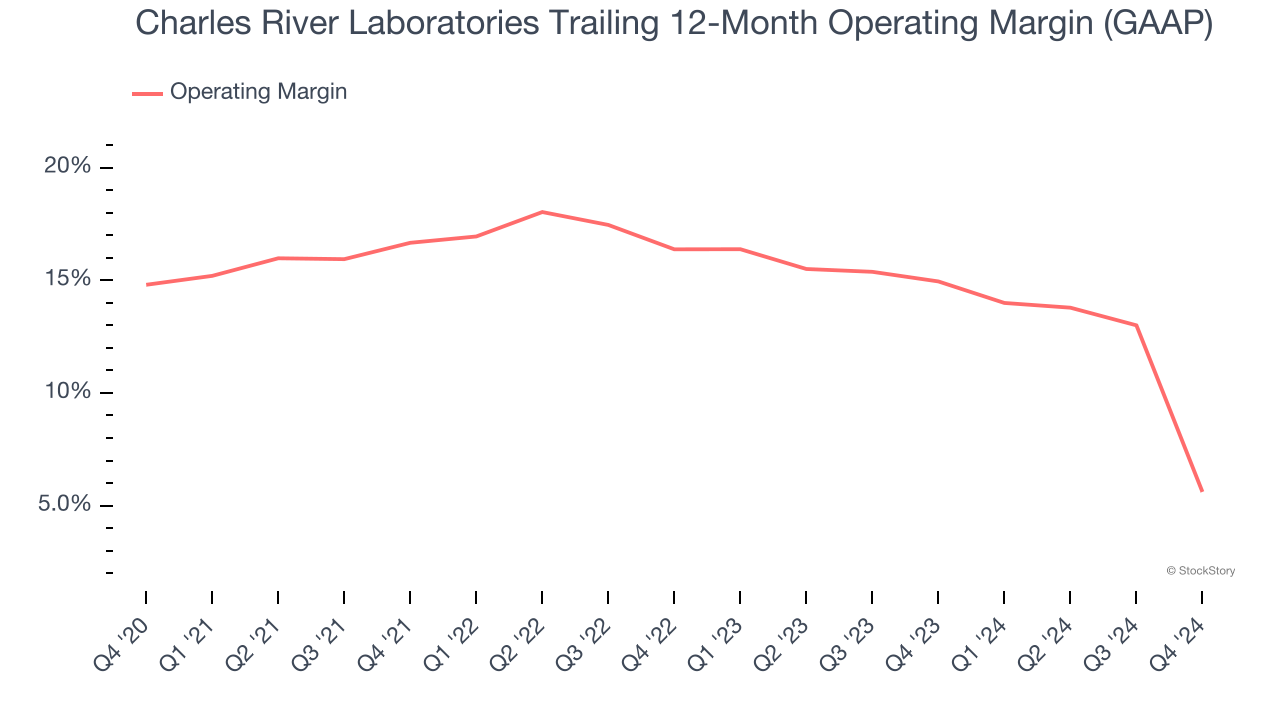

- Operating Margin: -16.7%, down from 13.1% in the same quarter last year

- Free Cash Flow Margin: 8.4%, down from 14.1% in the same quarter last year

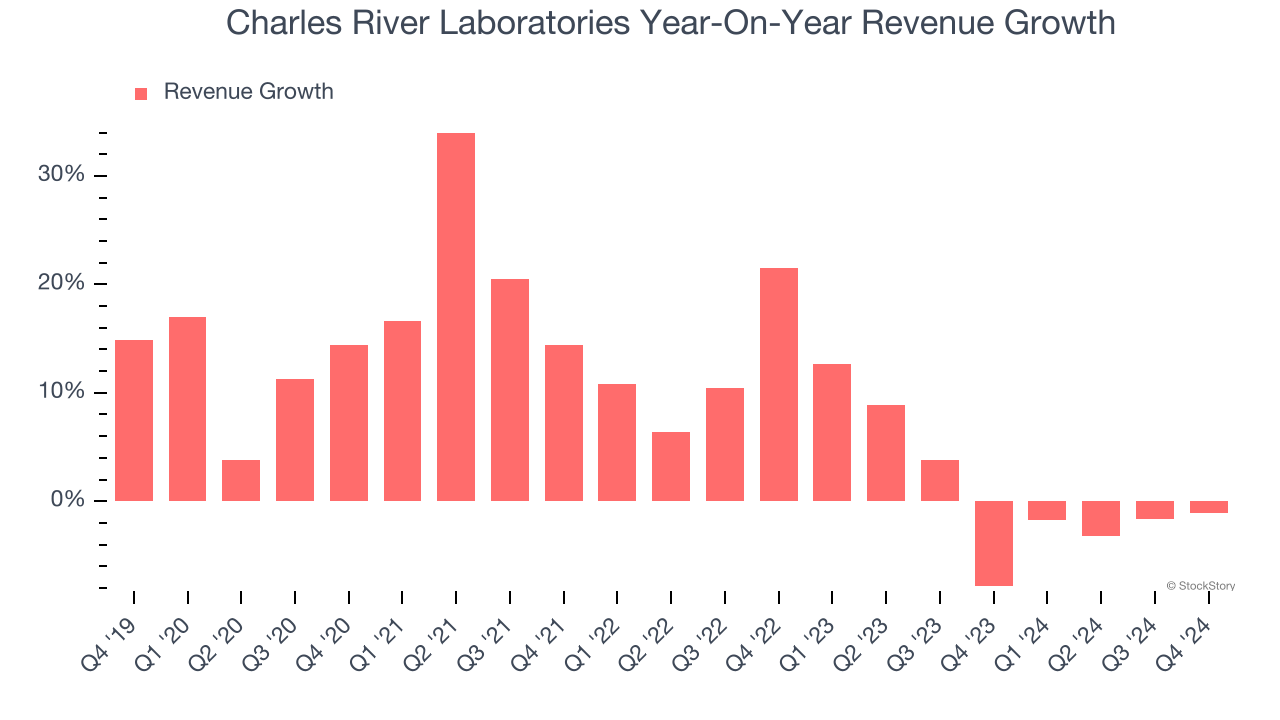

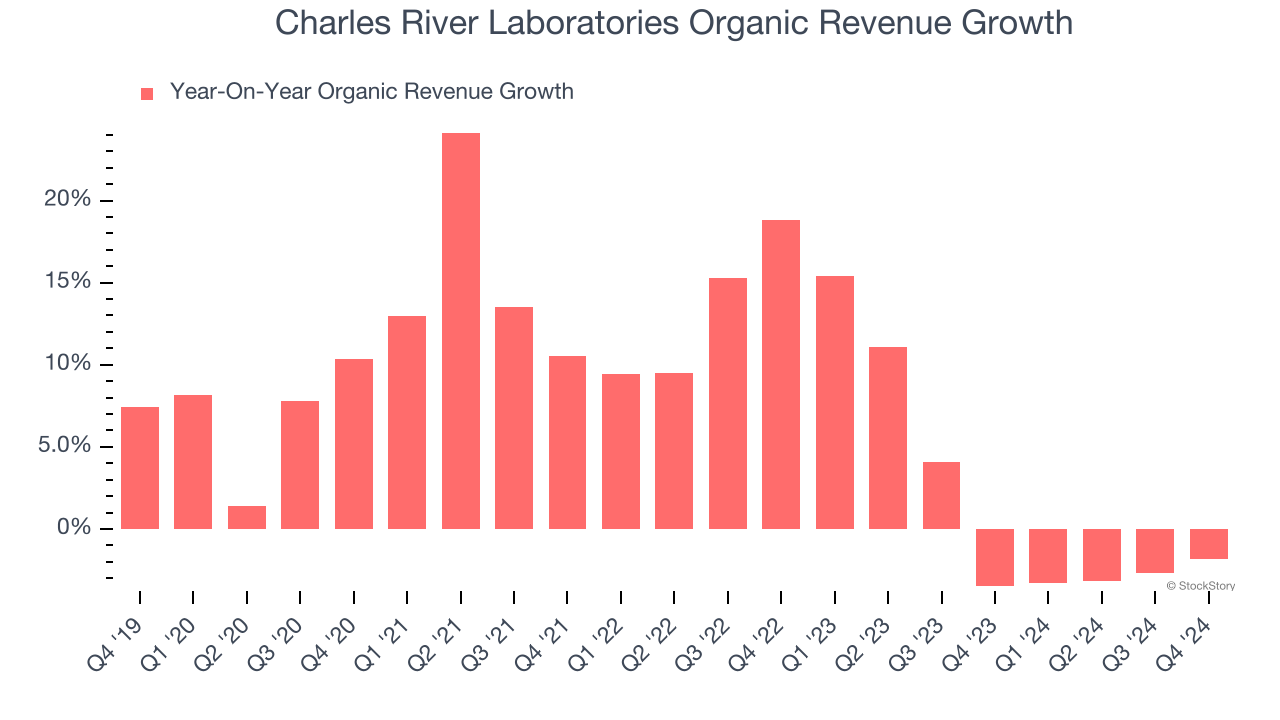

- Organic Revenue fell 1.8% year on year (-3.5% in the same quarter last year)

- Market Capitalization: $7.87 billion

James C. Foster, Chair, President and Chief Executive Officer, said, “Throughout 2024, we have launched initiatives to generate more revenue, aggressively reduce costs, and further strengthen our business. As we move into 2025, we see many of our global biopharmaceutical clients continuing to move forward with their restructuring and pipeline reprioritization activities, which are expected to constrain early-stage spending by many of these clients again in 2025. We believe these trends are stabilizing, and therefore, our view of the global biopharmaceutical demand environment remains unchanged. In addition, small and mid-sized biotechnology clients continued to benefit from a more favorable funding environment in 2024, and we expect biotechnology demand trends will be stable to slightly improved this year.”

Company Overview

Founded in 1947, Charles River Laboratories (NYSE:CRL) provides laboratory services related to drug discovery, development solutions, and safety assessments for pharmaceutical and biotechnology companies.

Drug Development Inputs & Services

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Luckily, Charles River Laboratories’s sales grew at a decent 9.1% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Charles River Laboratories’s recent history shows its demand slowed as its revenue was flat over the last two years.

Charles River Laboratories also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Charles River Laboratories’s organic revenue averaged 2% year-on-year growth. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Charles River Laboratories’s revenue fell by 1.1% year on year to $1.00 billion but beat Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to decline by 4.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Charles River Laboratories has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 13.5%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Charles River Laboratories’s operating margin decreased by 9.2 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 10.8 percentage points on a two-year basis. We’re disappointed in these results because it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Charles River Laboratories generated an operating profit margin of negative 16.7%, down 29.8 percentage points year on year. This contraction shows it was recently less efficient because its expenses increased relative to its revenue.

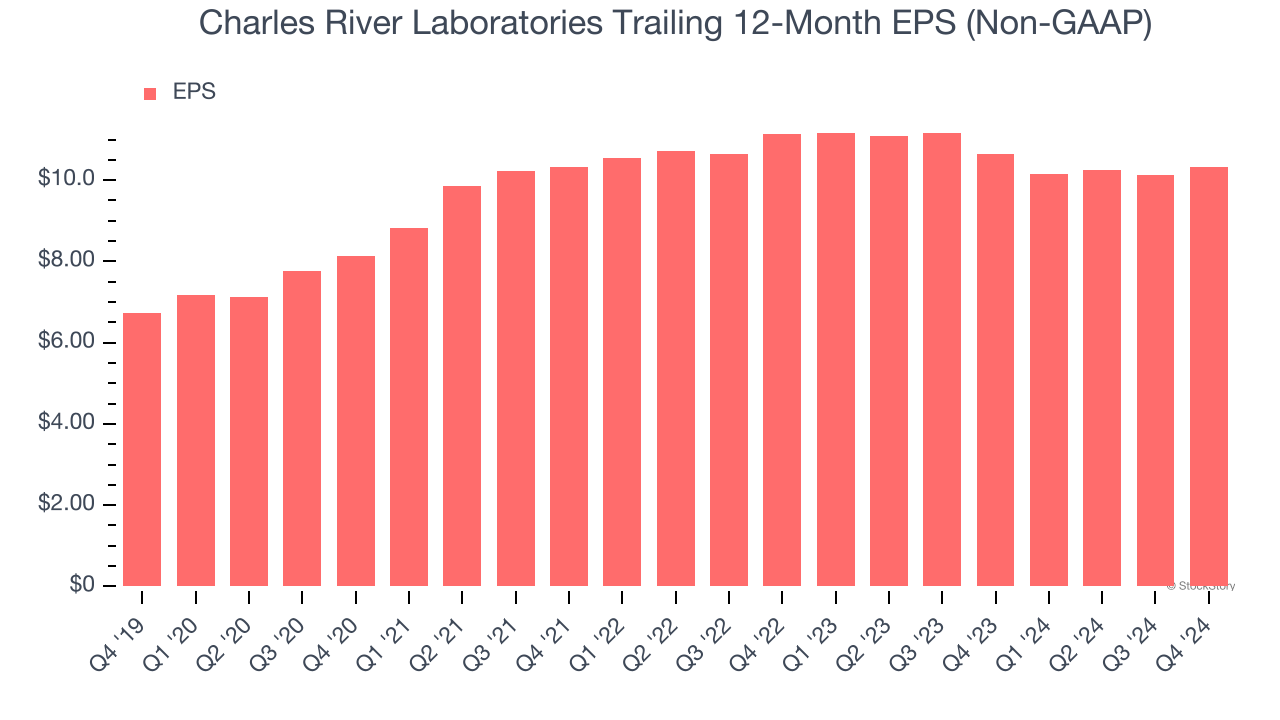

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Charles River Laboratories’s solid 8.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, Charles River Laboratories reported EPS at $2.66, up from $2.46 in the same quarter last year. This print beat analysts’ estimates by 5.1%. Over the next 12 months, Wall Street expects Charles River Laboratories’s full-year EPS of $10.32 to shrink by 5.8%.

Key Takeaways from Charles River Laboratories’s Q4 Results

We enjoyed seeing Charles River Laboratories exceed analysts’ organic revenue and EPS expectations. On the other hand, its full-year EPS guidance missed Wall Street’s estimates, making this a weaker quarter. The stock remained flat at $153.90 immediately following the results.

So do we think Charles River Laboratories is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.