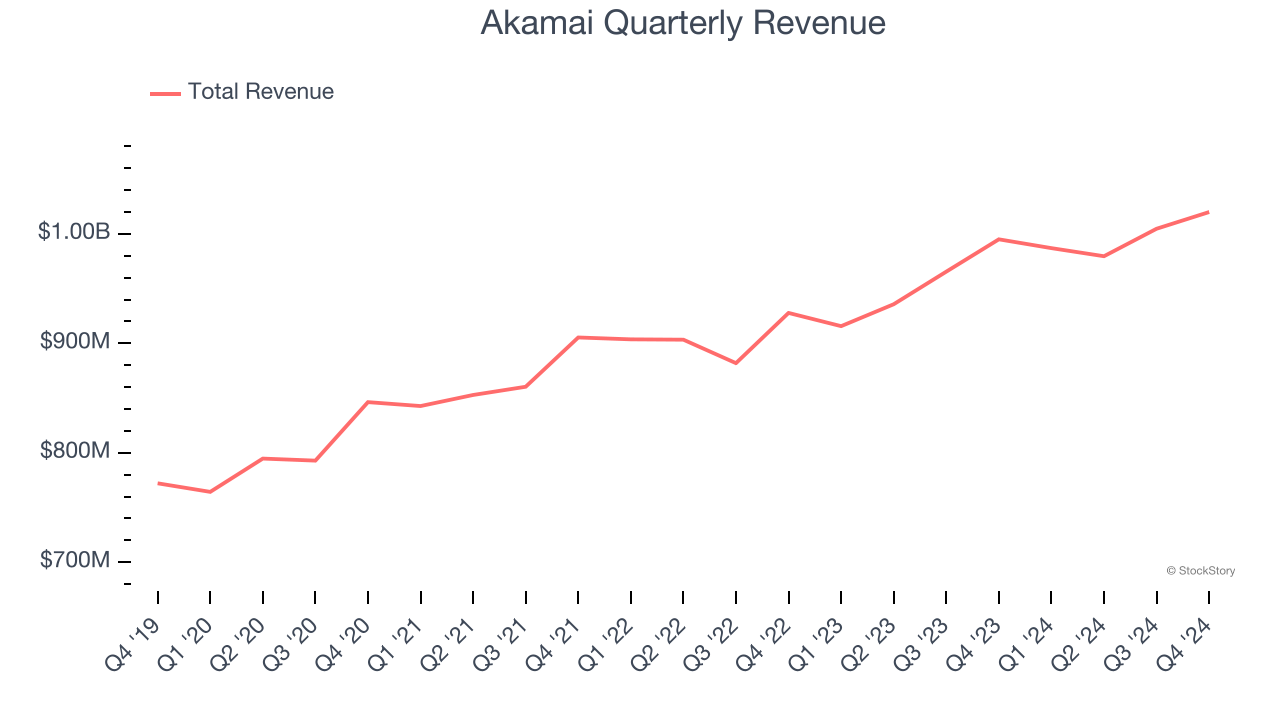

Web content delivery and security company Akamai (NASDAQ:AKAM) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 2.5% year on year to $1.02 billion. On the other hand, next quarter’s revenue guidance of $1.01 billion was less impressive, coming in 3.1% below analysts’ estimates. Its non-GAAP profit of $1.66 per share was 9% above analysts’ consensus estimates.

Is now the time to buy Akamai? Find out by accessing our full research report, it’s free.

Akamai (AKAM) Q4 CY2024 Highlights:

- Revenue: $1.02 billion vs analyst estimates of $1.02 billion (2.5% year-on-year growth, in line)

- Adjusted EPS: $1.66 vs analyst estimates of $1.52 (9% beat)

- Adjusted Operating Income: $298.1 million vs analyst estimates of $278.8 million (29.2% margin, 6.9% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $4.1 billion at the midpoint, missing analyst estimates by 3.8% and implying 2.7% growth (vs 4.8% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $6.20 at the midpoint, missing analyst estimates by 9.1%

- Operating Margin: 14.5%, down from 18.6% in the same quarter last year

- Free Cash Flow Margin: 17.7%, down from 20.6% in the previous quarter

- Market Capitalization: $15.06 billion

"Akamai delivered a solid fourth quarter, demonstrating robust profitability and sustained momentum across our security and cloud computing solutions," said Dr. Tom Leighton, Akamai's Chief Executive Officer.

Company Overview

Founded in 1999 by two engineers from MIT, Akamai (NASDAQ:AKAM) provides software for organizations to efficiently deliver web content to their customers.

Content Delivery

The amount of content on the internet is exploding, whether it is music, movies and or e-commerce stores. Consumer demand for this content creates network congestion, much like a digital traffic jam which drives demand for specialized content delivery networks (CDN) services that alleviate potential network bottlenecks.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Akamai’s sales grew at a weak 4.9% compounded annual growth rate over the last three years. This was below our standard for the software sector and is a rough starting point for our analysis.

This quarter, Akamai grew its revenue by 2.5% year on year, and its $1.02 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 2.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Akamai’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Akamai’s products and its peers.

Key Takeaways from Akamai’s Q4 Results

We enjoyed seeing Akamai beat analysts’ EBITDA expectations this quarter. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.4% to $92.75 immediately following the results.

Akamai may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.