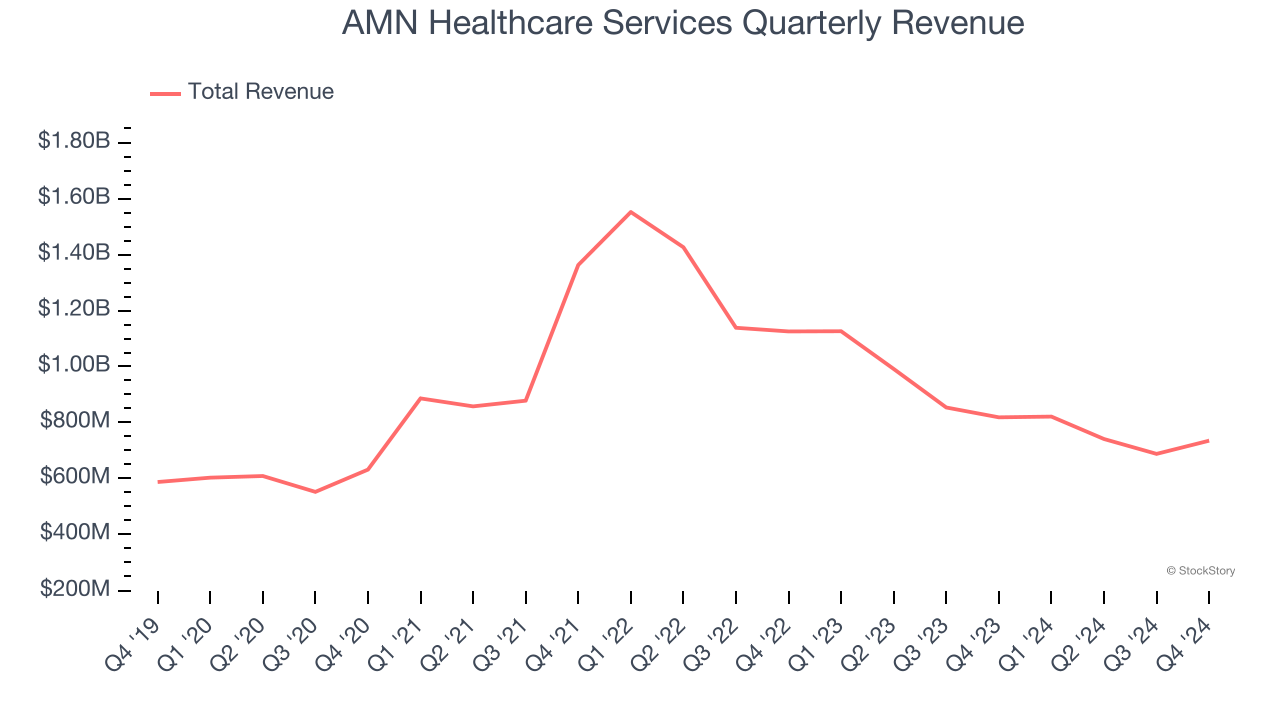

Healthcare staffing company AMN Healthcare Services (NYSE:AMN) beat Wall Street’s revenue expectations in Q4 CY2024, but sales fell by 10.2% year on year to $734.7 million. Guidance for next quarter’s revenue was better than expected at $670 million at the midpoint, 1% above analysts’ estimates. Its non-GAAP profit of $0.75 per share was 53.7% above analysts’ consensus estimates.

Is now the time to buy AMN Healthcare Services? Find out by accessing our full research report, it’s free.

AMN Healthcare Services (AMN) Q4 CY2024 Highlights:

- Revenue: $734.7 million vs analyst estimates of $694.4 million (10.2% year-on-year decline, 5.8% beat)

- Adjusted EPS: $0.75 vs analyst estimates of $0.49 (53.7% beat)

- Adjusted EBITDA: $75.12 million vs analyst estimates of $65.12 million (10.2% margin, 15.4% beat)

- Revenue Guidance for Q1 CY2025 is $670 million at the midpoint, above analyst estimates of $663.3 million

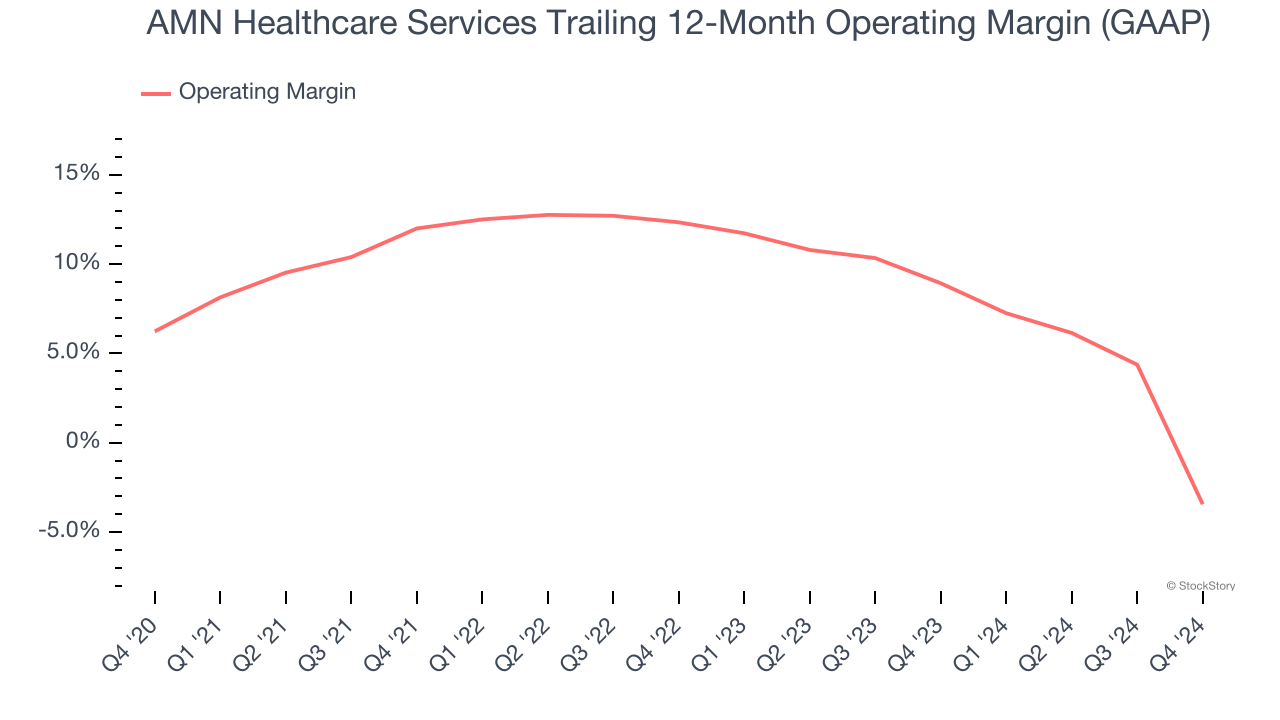

- Operating Margin: -27.6%, down from 4.2% in the same quarter last year

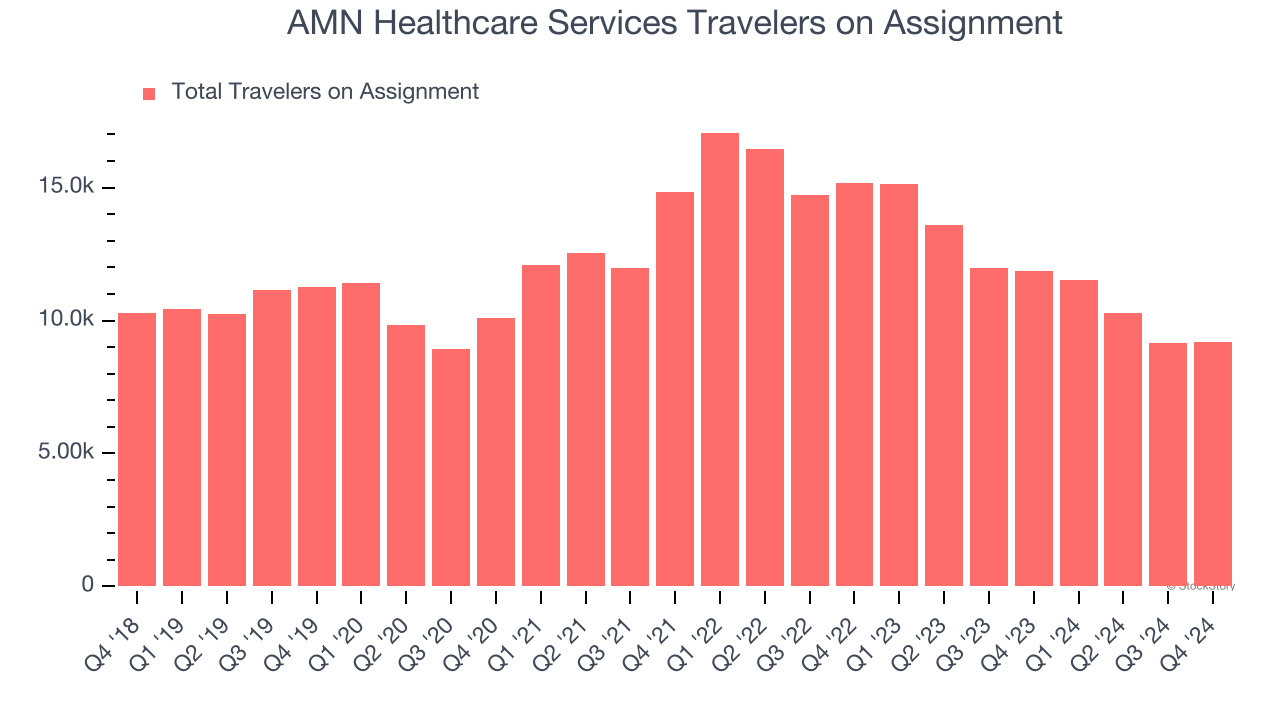

- Traveler on Assignment fell 22.4% year on year, in line with the same quarter last year

- Market Capitalization: $907.7 million

“AMN recorded a solid fourth quarter that outperformed our expectations, and we continue to see a more normalized operating environment compared with the past two years,” said Cary Grace, AMN President and Chief Executive Officer.

Company Overview

Founded in 1985, AMN Healthcare Services (NYSE:AMN) provides workforce and staffing services for the healthcare industry, specializing in placing nurses, physicians, and other health in various care settings.

Specialized Medical & Nursing Services

The skilled nursing services industry provides specialized care for patients requiring medical or rehabilitative support after hospital stays or for chronic conditions. These companies benefit from stable demand driven by an aging population and recurring revenue from Medicare, Medicaid, and private insurance. However, the industry faces challenges such as thin margins due to high labor costs and stringent regulatory requirements. Looking ahead, the industry is supported by tailwinds from an aging population, which means higher chronic disease prevalence. Advances in medical technology, including using AI to better predict, diagnose, and treat illnesses, may reduce hospital readmissions and improve outcomes. However, headwinds such as labor shortages, wage inflation, and potential government reimbursement cuts pose challenges. Adapting to value-based care models may further squeeze margins by requiring investments in training, technology, and compliance.

Sales Growth

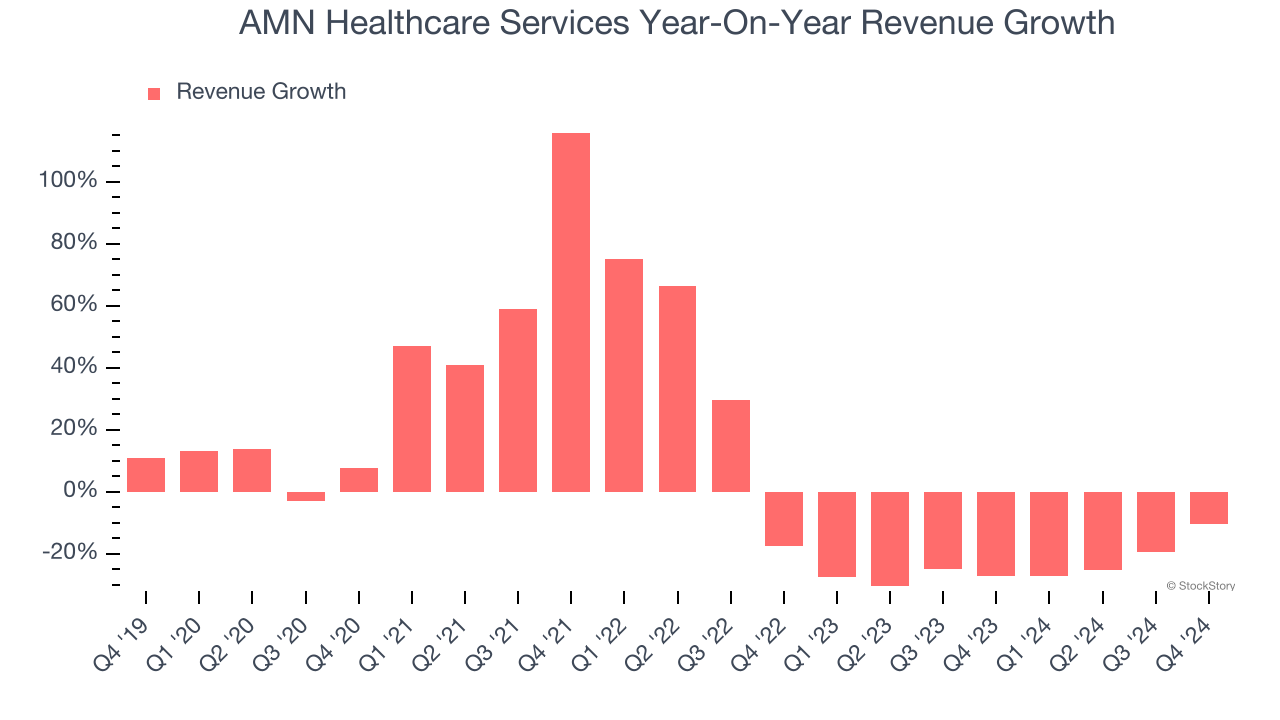

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, AMN Healthcare Services’s sales grew at a mediocre 6.1% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. AMN Healthcare Services’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 24.6% annually.

We can better understand the company’s revenue dynamics by analyzing its number of travelers on assignment, which reached 9,206 in the latest quarter. Over the last two years, AMN Healthcare Services’s travelers on assignment averaged 20.4% year-on-year declines. Because this number is better than its revenue growth, we can see the company’s average price decreased.

This quarter, AMN Healthcare Services’s revenue fell by 10.2% year on year to $734.7 million but beat Wall Street’s estimates by 5.8%. Company management is currently guiding for a 18.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 10% over the next 12 months. While this projection is better than its two-year trend, it's hard to get excited about a company that is struggling with demand.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

AMN Healthcare Services was profitable over the last five years but held back by its large cost base. Its average operating margin of 8.2% was weak for a healthcare business.

Looking at the trend in its profitability, AMN Healthcare Services’s operating margin decreased by 9.7 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 15.8 percentage points on a two-year basis. We’re disappointed in these results because it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, AMN Healthcare Services generated an operating profit margin of negative 27.6%, down 31.7 percentage points year on year. This contraction shows it was recently less efficient because its expenses increased relative to its revenue.

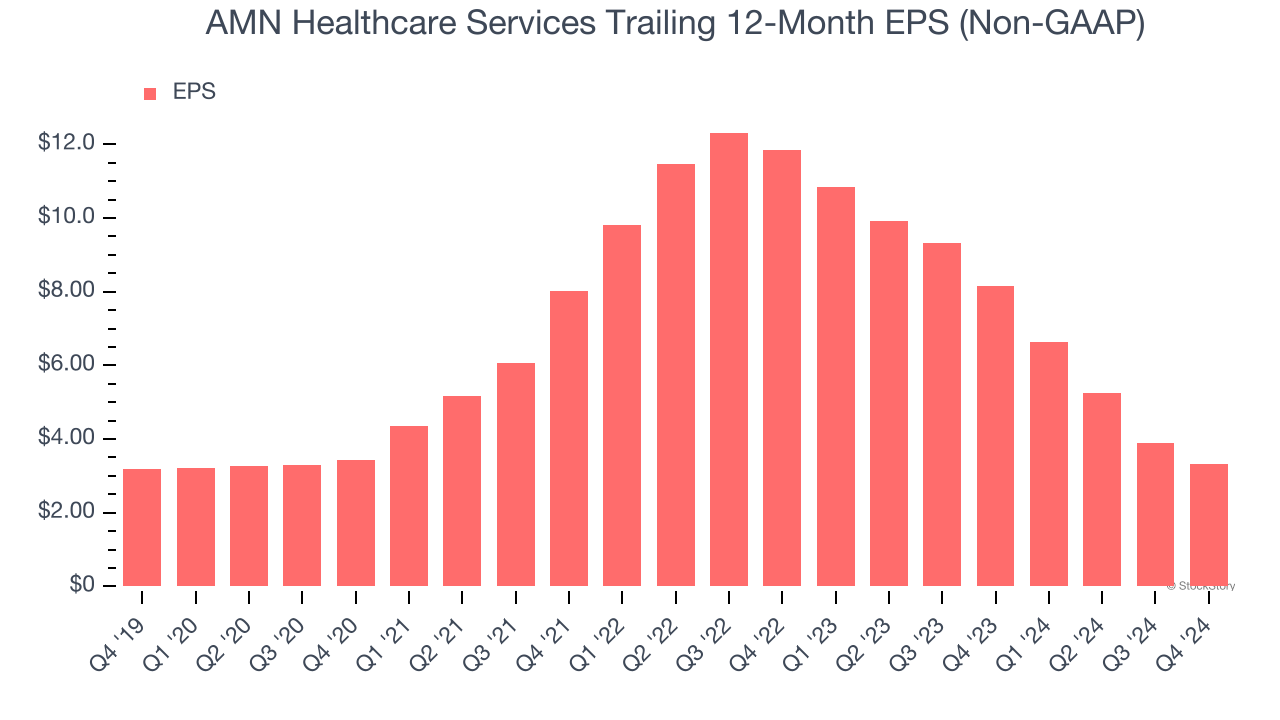

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

AMN Healthcare Services’s flat EPS over the last five years was below its 6.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into AMN Healthcare Services’s earnings to better understand the drivers of its performance. As we mentioned earlier, AMN Healthcare Services’s operating margin declined by 9.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, AMN Healthcare Services reported EPS at $0.75, down from $1.32 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects AMN Healthcare Services’s full-year EPS of $3.31 to shrink by 53.9%.

Key Takeaways from AMN Healthcare Services’s Q4 Results

We were impressed by how significantly AMN Healthcare Services blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also excited its full-year revenue guidance outperformed Wall Street’s estimates. On the other hand, its travelers on assignment missed significantly. Still, we think this was a solid quarter with some key areas of upside. The stock traded up 3.2% to $26.68 immediately after reporting.

AMN Healthcare Services put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.