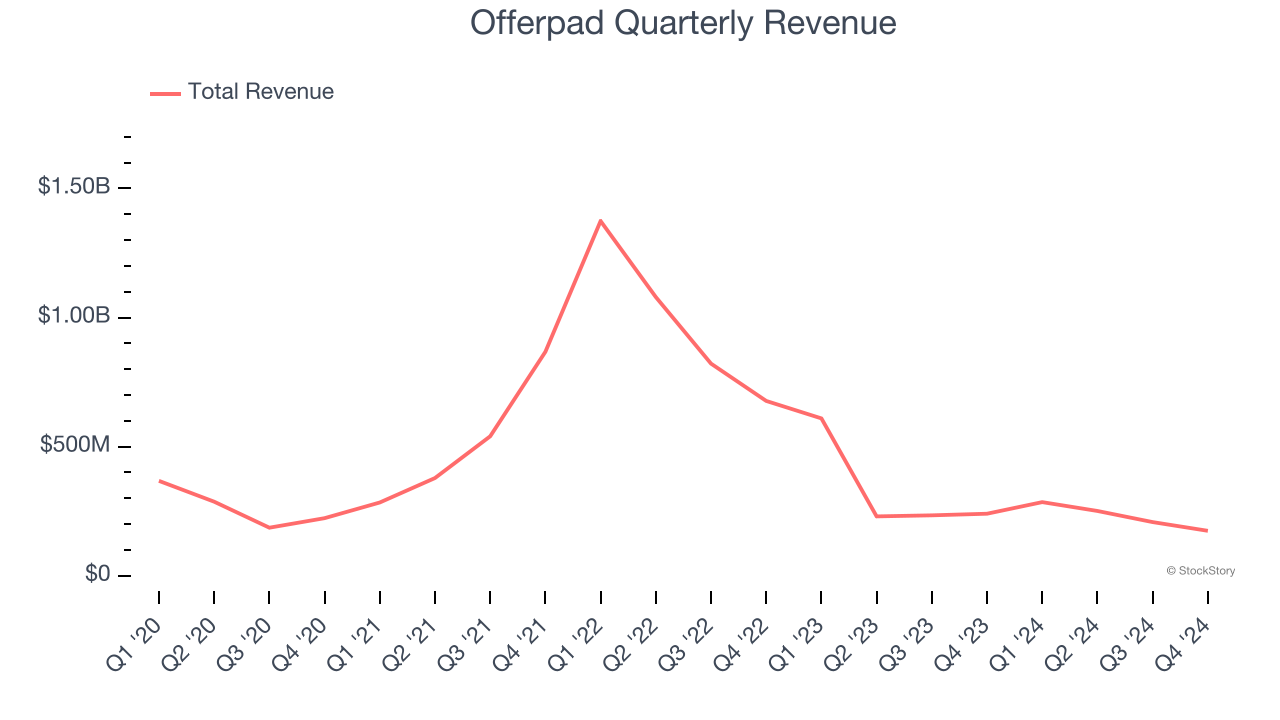

Technology real estate company Offerpad (NYSE:OPAD) met Wall Street’s revenue expectations in Q4 CY2024, but sales fell by 27.5% year on year to $174.3 million. On the other hand, next quarter’s revenue guidance of $160 million was less impressive, coming in 38.6% below analysts’ estimates. Its GAAP loss of $0.63 per share was 31.2% below analysts’ consensus estimates.

Is now the time to buy Offerpad? Find out by accessing our full research report, it’s free.

Offerpad (OPAD) Q4 CY2024 Highlights:

- Revenue: $174.3 million vs analyst estimates of $173.8 million (27.5% year-on-year decline, in line)

- EPS (GAAP): -$0.63 vs analyst expectations of -$0.48 (31.2% miss)

- Adjusted EBITDA: -$11.48 million vs analyst estimates of -$7 million (-6.6% margin, miss)

- Revenue Guidance for Q1 CY2025 is $160 million at the midpoint, below analyst estimates of $260.4 million

- Operating Margin: -7.8%, down from -4.7% in the same quarter last year

- Free Cash Flow was $29.07 million, up from -$15.36 million in the same quarter last year

- Homes Sold: 503, down 209 year on year

- Market Capitalization: $61.27 million

“In the fourth quarter, revenue exceeded the midpoint of our guidance, supported by a balanced mix of offerings. This performance was achieved with the support of our Renovate business surpassing $18 million in revenue for the year and our improved advertising efficiencies driven by our Agent Partnership Program growing to nearly a third of our acquisitions,” said Brian Bair, Offerpad’s CEO.

Company Overview

Known for giving homeowners cash offers within 24 hours, Offerpad (NYSE:OPAD) operates a tech-enabled platform specializing in direct home buying and selling solutions.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

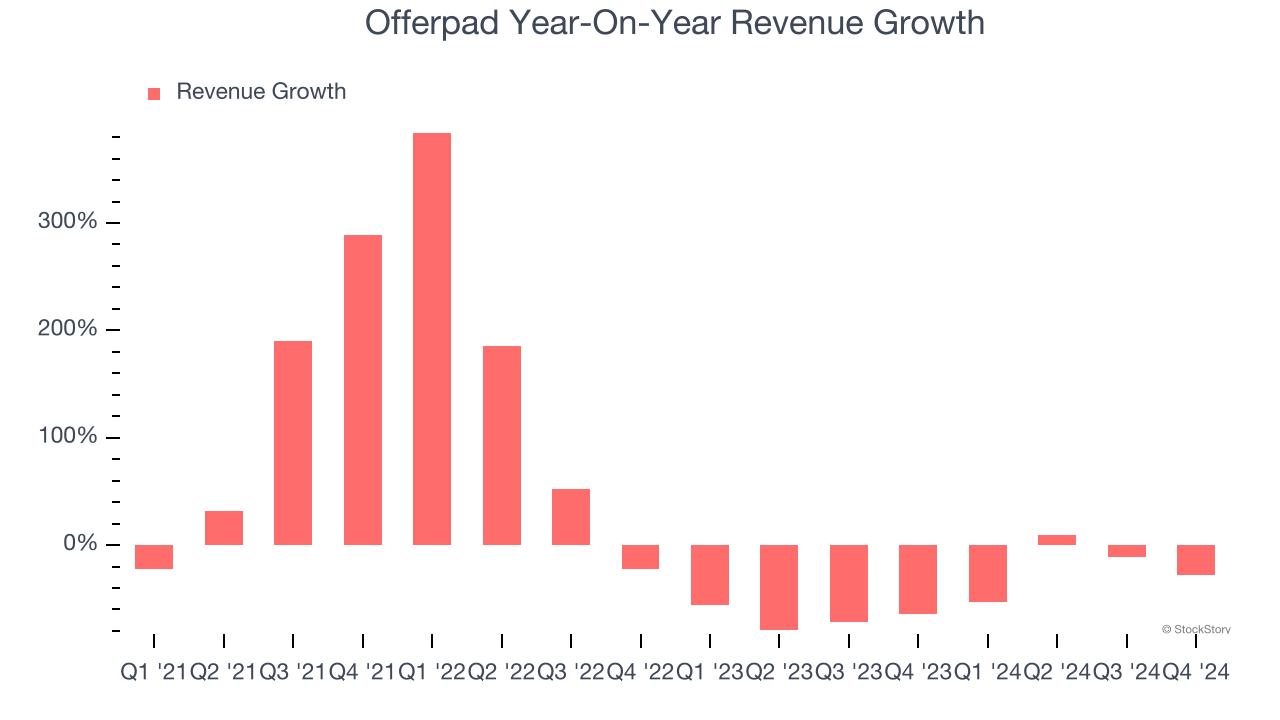

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Offerpad struggled to consistently generate demand over the last four years as its sales dropped at a 3.6% annual rate. This was below our standards and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Offerpad’s recent history shows its demand has stayed suppressed as its revenue has declined by 51.8% annually over the last two years.

Offerpad also discloses its number of homes sold and homes purchased, which clocked in at 503 and 384 in the latest quarter. Over the last two years, Offerpad’s homes sold averaged 42.4% year-on-year declines while its homes purchased averaged 20.8% year-on-year declines.

This quarter, Offerpad reported a rather uninspiring 27.5% year-on-year revenue decline to $174.3 million of revenue, in line with Wall Street’s estimates. Company management is currently guiding for a 43.9% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 34.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

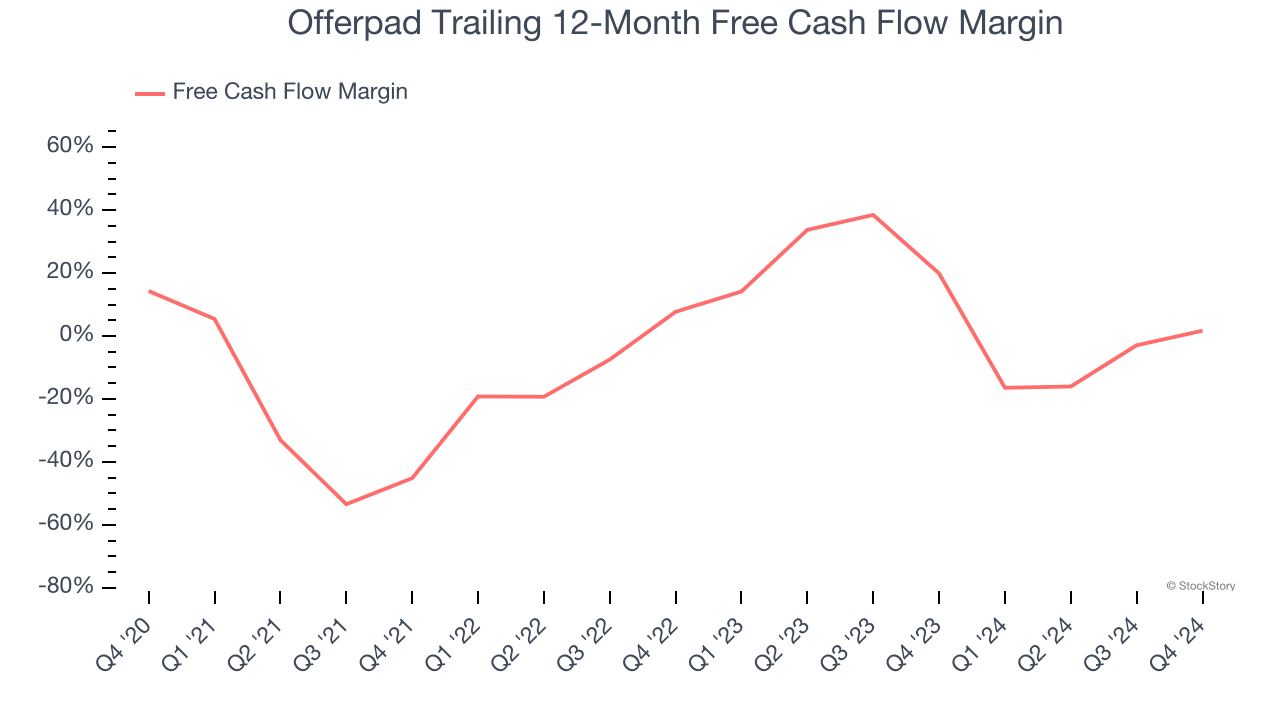

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Offerpad has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.4% over the last two years, slightly better than the broader consumer discretionary sector.

Offerpad’s free cash flow clocked in at $29.07 million in Q4, equivalent to a 16.7% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Offerpad will flip from cash-producing to cash-burning. Their consensus estimates imply its free cash flow margin of 1.7% for the last 12 months will decrease to negative 2.8%.

Key Takeaways from Offerpad’s Q4 Results

We struggled to find many positives in these results. Its revenue guidance for next quarter missed significantly and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 4.1% to $2.08 immediately after reporting.

The latest quarter from Offerpad’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.