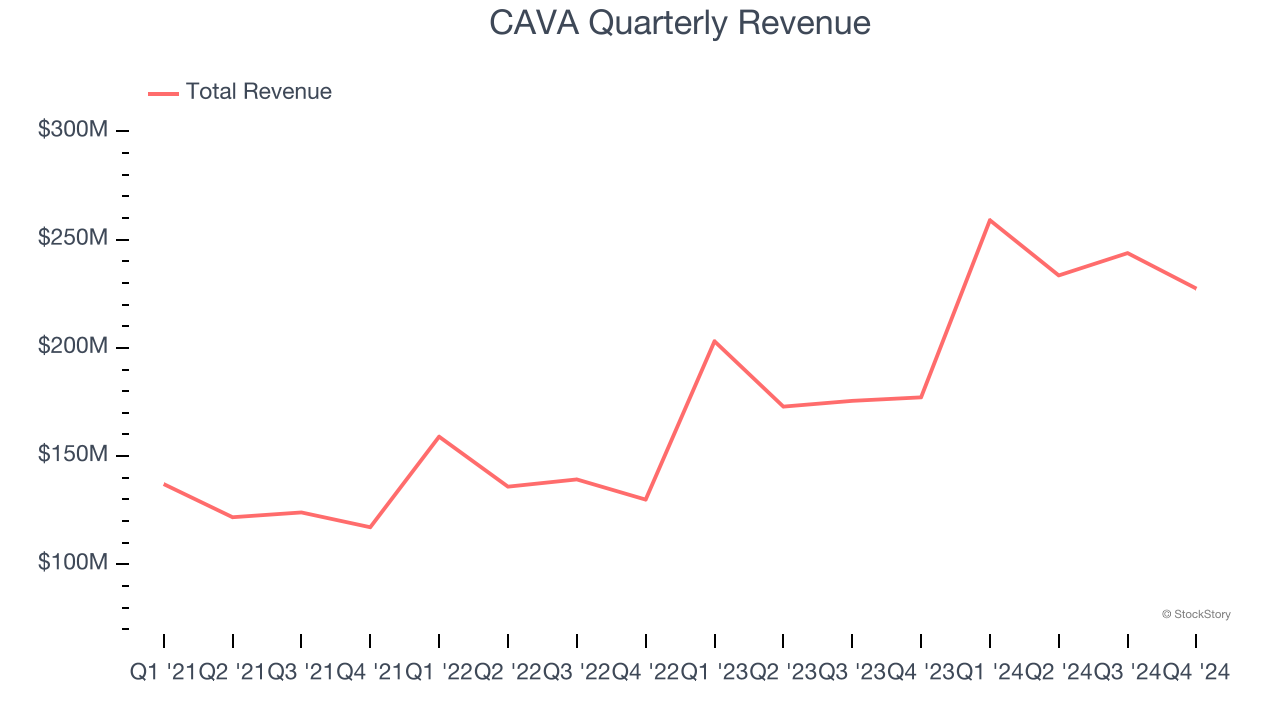

Mediterranean fast-casual restaurant chain CAVA (NYSE:CAVA) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 28.3% year on year to $227.4 million. Its GAAP profit of $0.66 per share was significantly above analysts’ consensus estimates.

Is now the time to buy CAVA? Find out by accessing our full research report, it’s free.

CAVA (CAVA) Q4 CY2024 Highlights:

- Revenue: $227.4 million vs analyst estimates of $222.4 million (28.3% year-on-year growth, 2.2% beat)

- EPS (GAAP): $0.66 vs analyst estimates of $0.07 (significant beat)

- Adjusted EBITDA: $25.1 million vs analyst estimates of $23.58 million (11% margin, 6.5% beat)

- EBITDA guidance for the upcoming financial year 2025 is $153.5 million at the midpoint, below analyst estimates of $163.5 million

- Operating Margin: 1.7%, up from -0.9% in the same quarter last year

- Free Cash Flow was $2.11 million, up from -$7.23 million in the same quarter last year

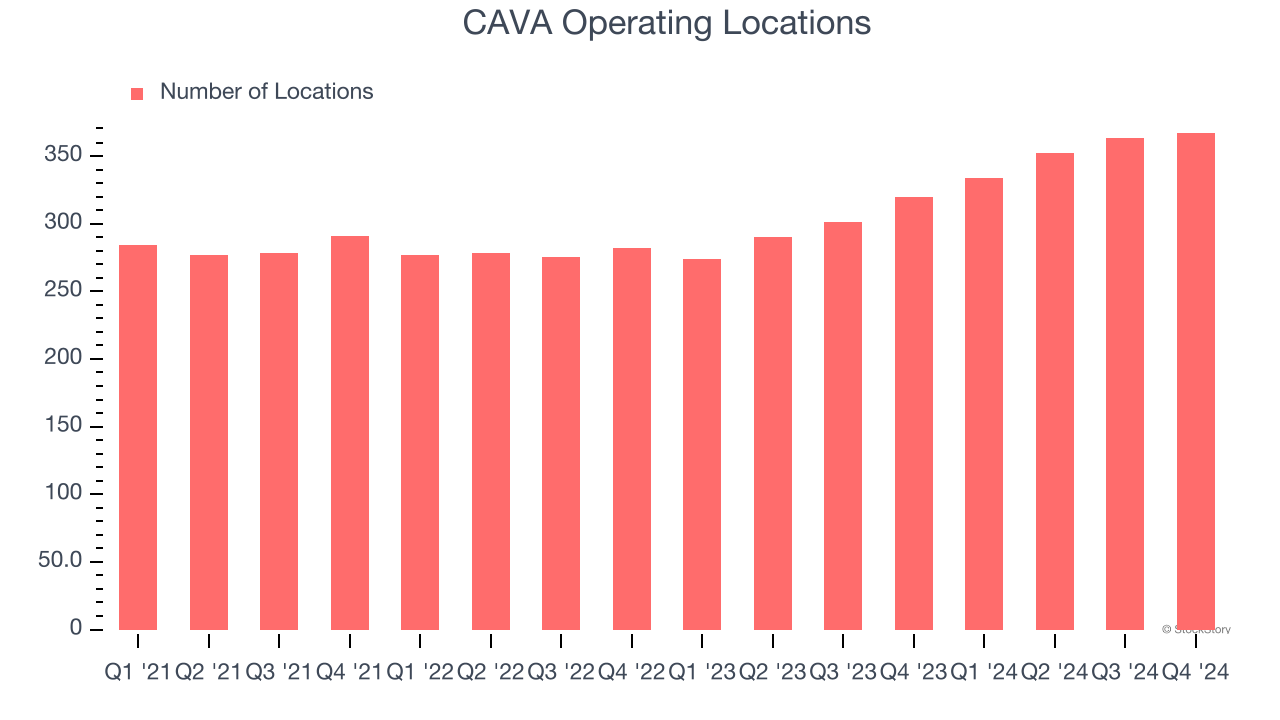

- Locations: 367 at quarter end, up from 320 in the same quarter last year

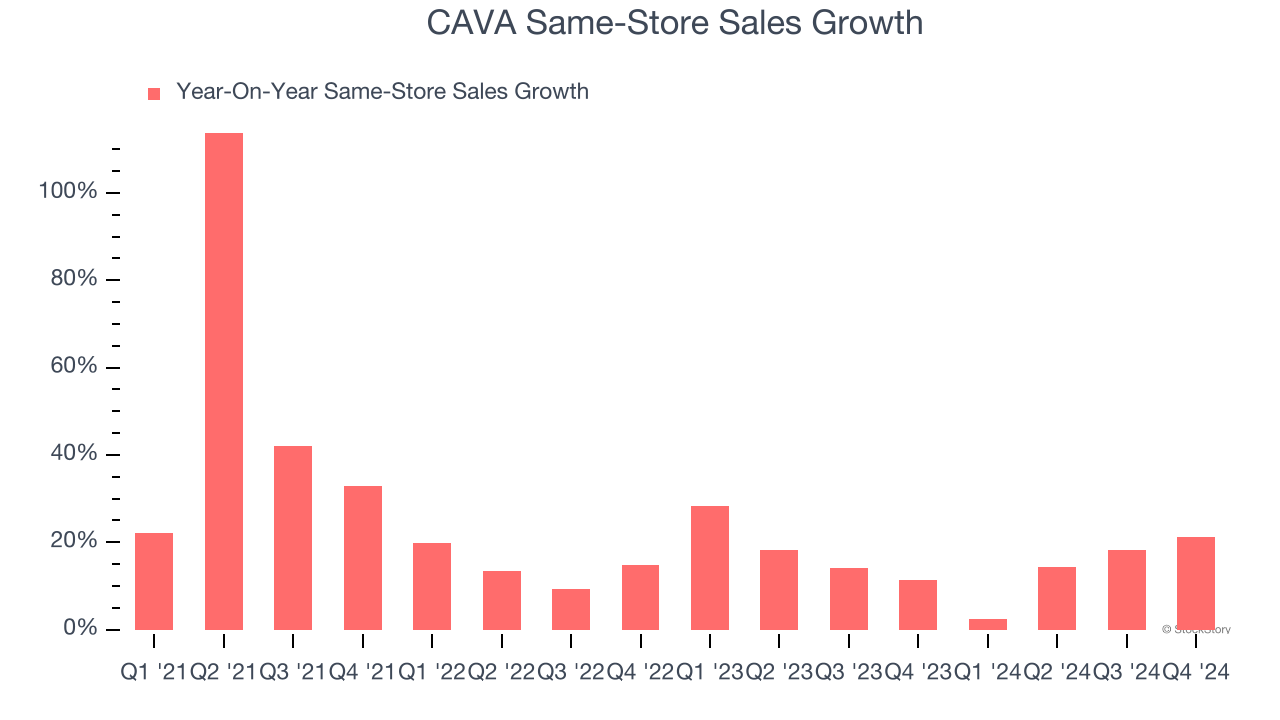

- Same-Store Sales rose 21.2% year on year (11.4% in the same quarter last year)

- Market Capitalization: $11.94 billion

“2024 was another year of extraordinary growth and success for CAVA as we established Mediterranean as the next major cultural cuisine category and delivered our unique value proposition, that is clearly resonating with modern consumers. CAVA Same Restaurant Sales grew 13.4% in 2024, including traffic growth of nearly 9%. We opened 58 net new restaurants and, driven by our powerful unit economic engine, generated average unit volume of $2.9 million. In addition, we continued to execute across our strategic initiatives. The launch of our grilled steak main exceeded our expectations, we rolled out a new labor model to deliver a better operator and guest experience, and, through our reimagined loyalty program, we gave guests more reasons to come to CAVA and come back more often,” said Brett Schulman, Co-Founder and CEO.

Company Overview

Starting from a single Washington, D.C. location, CAVA (NYSE:CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $963.7 million in revenue over the past 12 months, CAVA is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, CAVA’s 24.4% annualized revenue growth over the last three years (we compare to 2019 to normalize for COVID-19 impacts) was incredible as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, CAVA reported robust year-on-year revenue growth of 28.3%, and its $227.4 million of revenue topped Wall Street estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 22.5% over the next 12 months, a slight deceleration versus the last three years. Still, this projection is noteworthy and indicates the market is baking in success for its menu offerings.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

CAVA sported 367 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 13.1% annual growth, among the fastest in the restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

CAVA has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 16%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, CAVA’s same-store sales rose 21.2% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from CAVA’s Q4 Results

We were impressed by how significantly CAVA blew past analysts’ EPS and EBITDA expectations this quarter. We were also excited its same-store sales outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Zooming out, we think this was a solid quarter, but the areas below expectations seem to be driving the move. Shares traded down 3.5% to $95.82 immediately after reporting.

Is CAVA an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.