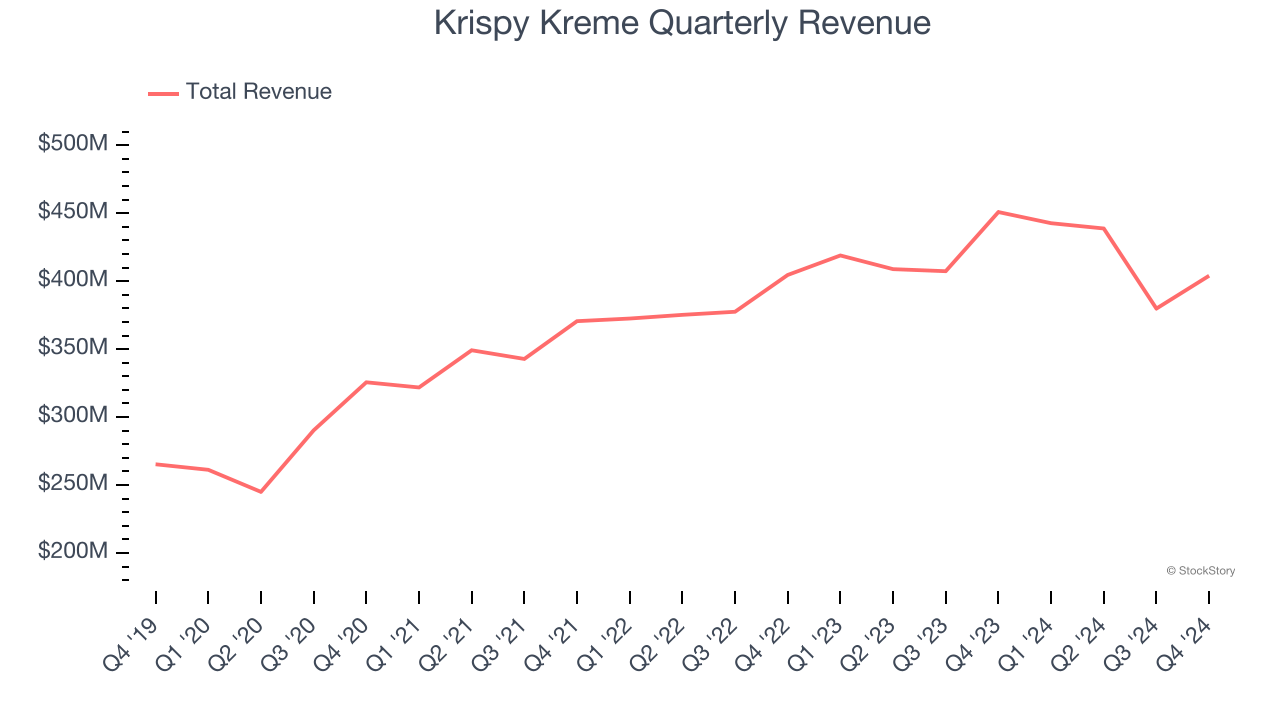

Doughnut chain Krispy Kreme (NASDAQ:DNUT) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 10.4% year on year to $404 million. The company’s full-year revenue guidance of $1.6 billion at the midpoint came in 10.4% below analysts’ estimates. Its non-GAAP profit of $0.01 per share was 89.8% below analysts’ consensus estimates.

Is now the time to buy Krispy Kreme? Find out by accessing our full research report, it’s free.

Krispy Kreme (DNUT) Q4 CY2024 Highlights:

- Revenue: $404 million vs analyst estimates of $411.1 million (10.4% year-on-year decline, 1.7% miss)

- Adjusted EPS: $0.01 vs analyst expectations of $0.10 (89.8% miss)

- Adjusted EBITDA: $45.92 million vs analyst estimates of $57.83 million (11.4% margin, 20.6% miss)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.6 billion at the midpoint, missing analyst estimates by 10.4% and implying -3.9% growth (vs -1% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $0.06 at the midpoint, missing analyst estimates by 80.4%

- EBITDA guidance for the upcoming financial year 2025 is $190 million at the midpoint, below analyst estimates of $236.8 million

- Operating Margin: -2.8%, down from -1.2% in the same quarter last year

- Free Cash Flow was -$6.87 million compared to -$31.31 million in the same quarter last year

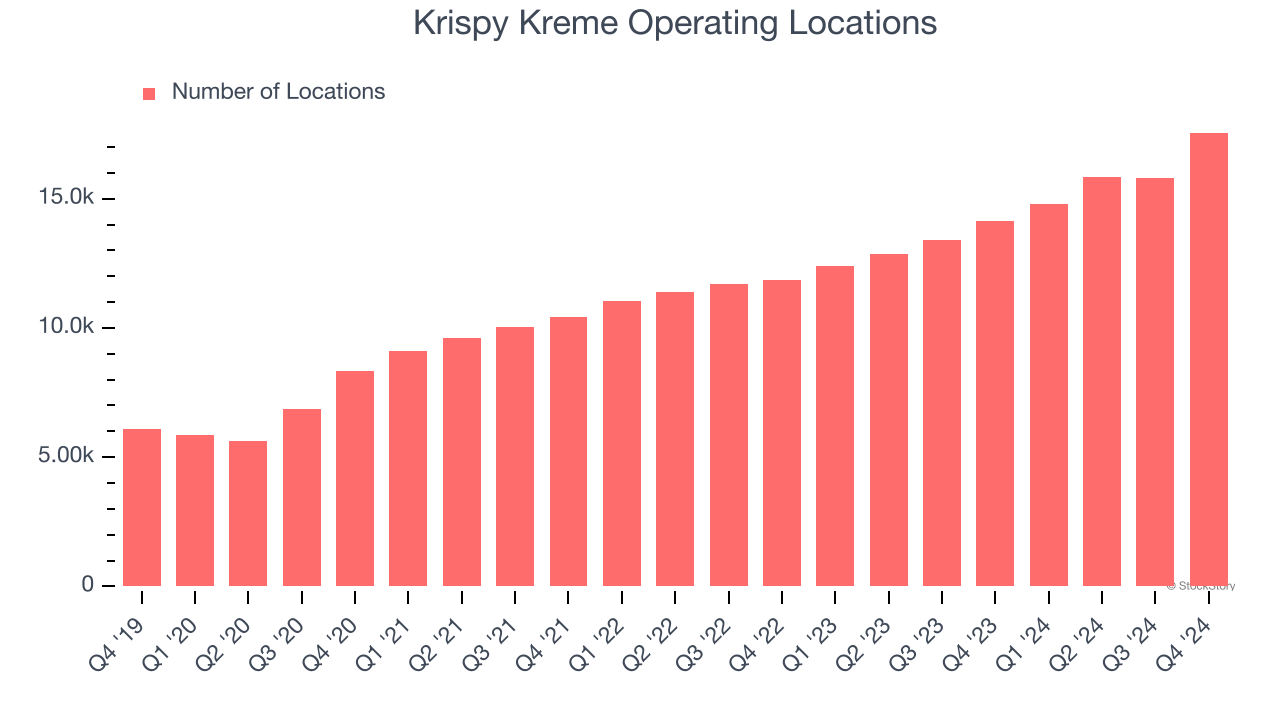

- Locations: 17,557 at quarter end, up from 14,136 in the same quarter last year

- Market Capitalization: $1.55 billion

“We delivered an 18th consecutive quarter of year-over-year organic sales growth. Excluding the estimated cybersecurity incident impact, results were largely in line with our expectations,” said Josh Charlesworth, Krispy Kreme CEO.

Company Overview

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ:DNUT) is one of the most beloved and well-known fast-food chains in the world.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.67 billion in revenue over the past 12 months, Krispy Kreme is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Krispy Kreme’s sales grew at a solid 11.7% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and expanded its reach.

This quarter, Krispy Kreme missed Wall Street’s estimates and reported a rather uninspiring 10.4% year-on-year revenue decline, generating $404 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last five years. This projection doesn't excite us and suggests its menu offerings will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Krispy Kreme operated 17,557 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 18% annual growth, much faster than the broader restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Key Takeaways from Krispy Kreme’s Q4 Results

We struggled to find many positives in these results as the company missed across all key metrics. Its full-year revenue, EPS, and EBITDA guidance also fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 9.4% to $8.27 immediately following the results.

Krispy Kreme’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.