Specialized equipment manufacturer for infrastructure and vegetation management Alamo Group (NYSE:ALG) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 7.7% year on year to $385.3 million. Its non-GAAP profit of $2.39 per share was 4.9% above analysts’ consensus estimates.

Is now the time to buy Alamo? Find out by accessing our full research report, it’s free.

Alamo (ALG) Q4 CY2024 Highlights:

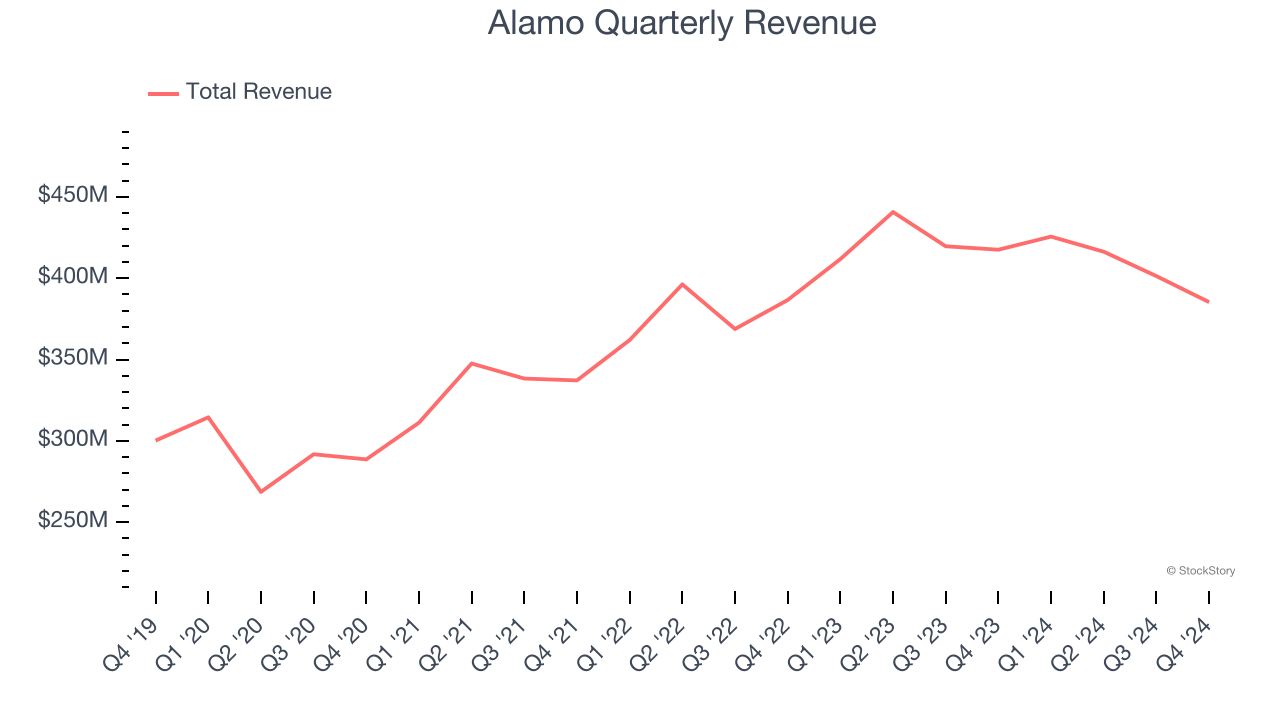

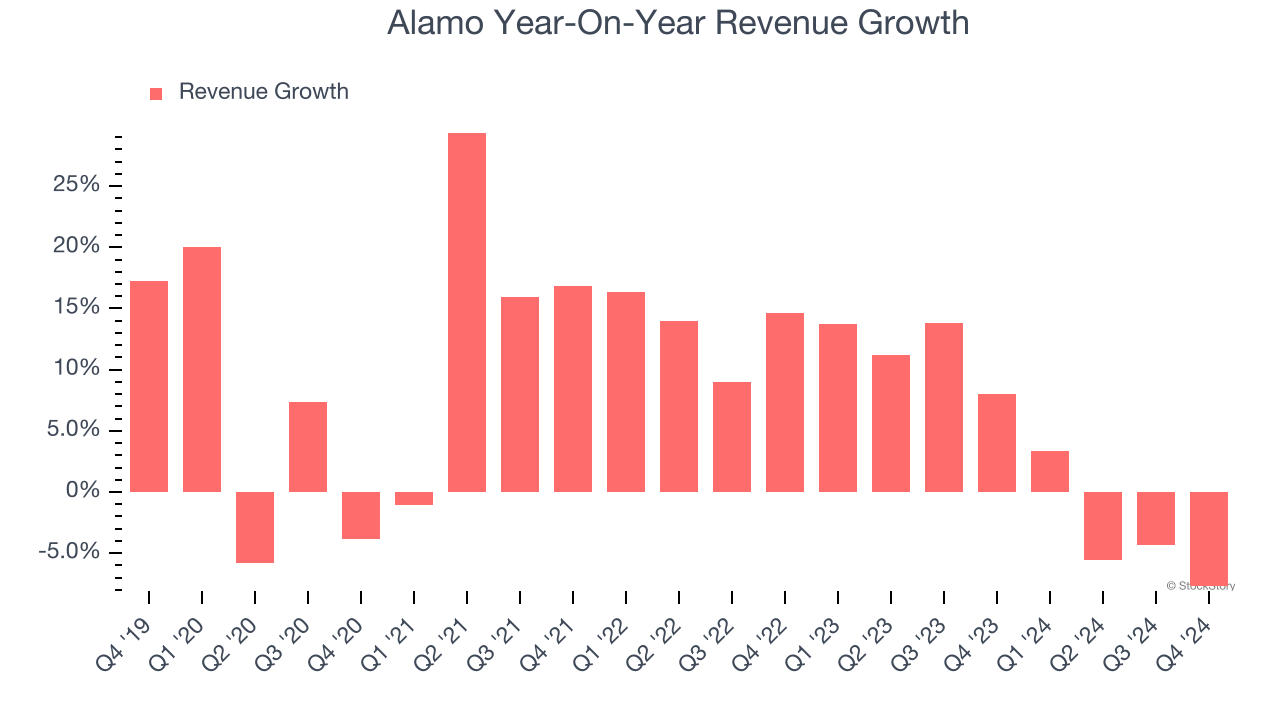

- Revenue: $385.3 million vs analyst estimates of $396.9 million (7.7% year-on-year decline, 2.9% miss)

- Adjusted EPS: $2.39 vs analyst estimates of $2.28 (4.9% beat)

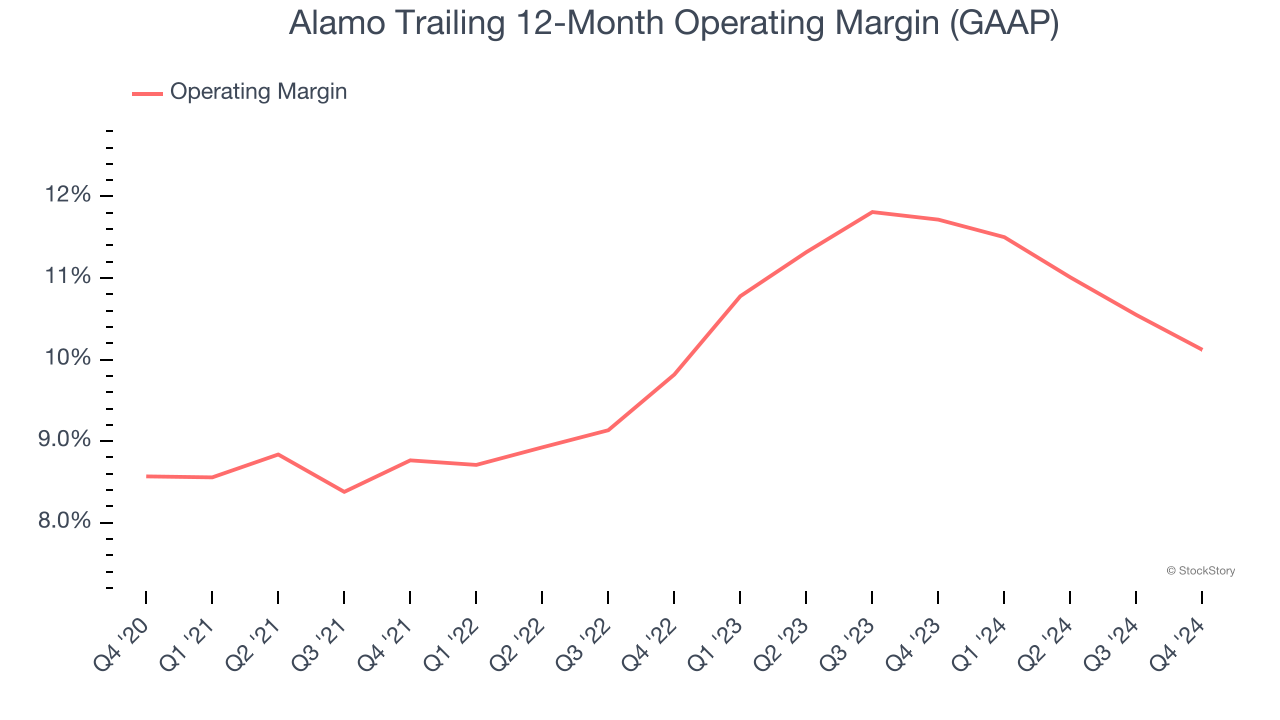

- Operating Margin: 8.9%, down from 10.7% in the same quarter last year

- Market Capitalization: $2.23 billion

Company Overview

Expanding its markets through acquisitions since its founding, Alamo (NSYE:ALG) designs, manufactures, and services vegetation management and infrastructure maintenance equipment for governmental, industrial, and agricultural use.

Agricultural Machinery

Agricultural machinery companies are investing to develop and produce more precise machinery, automated systems, and connected equipment that collects analyzable data to help farmers and other customers improve yields and increase efficiency. On the other hand, agriculture is seasonal and natural disasters or bad weather can impact the entire industry. Additionally, macroeconomic factors such as commodity prices or changes in interest rates–which dictate the willingness of these companies or their customers to invest–can impact demand for agricultural machinery.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, Alamo grew its sales at a decent 7.8% compounded annual growth rate. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Alamo’s recent history shows its demand slowed as its annualized revenue growth of 3.7% over the last two years is below its five-year trend.

This quarter, Alamo missed Wall Street’s estimates and reported a rather uninspiring 7.7% year-on-year revenue decline, generating $385.3 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Alamo has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 9.9%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Alamo’s operating margin rose by 1.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Alamo generated an operating profit margin of 8.9%, down 1.8 percentage points year on year. Since Alamo’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

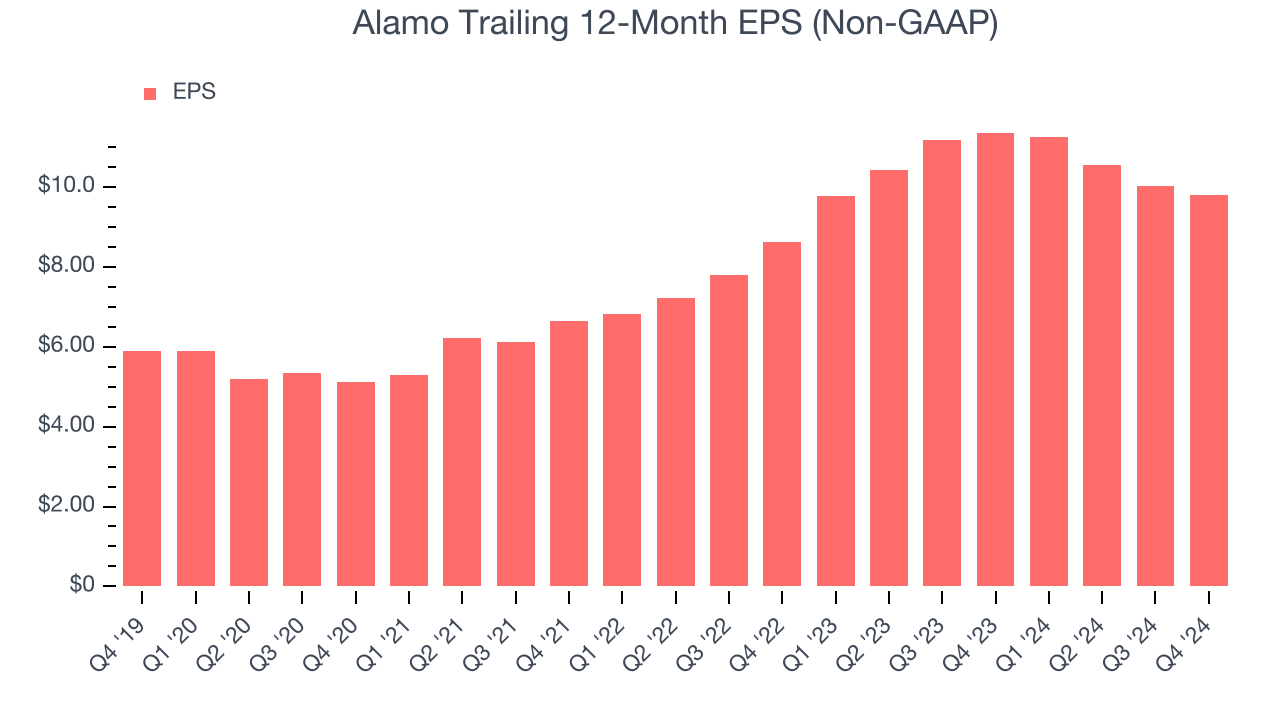

Alamo’s EPS grew at a solid 10.7% compounded annual growth rate over the last five years, higher than its 7.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Alamo’s earnings can give us a better understanding of its performance. As we mentioned earlier, Alamo’s operating margin declined this quarter but expanded by 1.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Alamo, its two-year annual EPS growth of 6.6% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Alamo reported EPS at $2.39, down from $2.63 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.9%. Over the next 12 months, Wall Street expects Alamo’s full-year EPS of $9.79 to grow 10.4%.

Key Takeaways from Alamo’s Q4 Results

It was encouraging to see Alamo beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed significantly, making this a weaker quarter. The stock remained flat at $184.26 immediately after reporting.

Is Alamo an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.