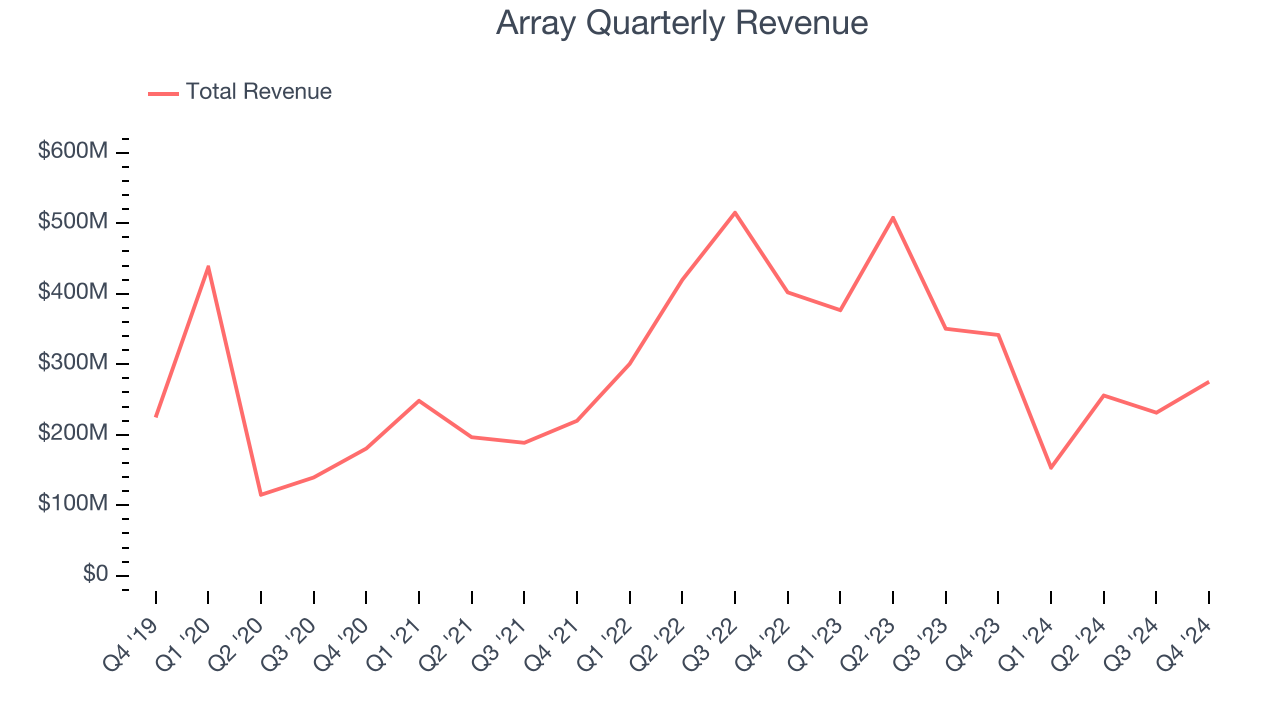

Solar tracking systems manufacturer Array (NASDAQ:ARRY) announced better-than-expected revenue in Q4 CY2024, but sales fell by 19.4% year on year to $275.2 million. The company expects next quarter’s revenue to be around $265 million, coming in 26.3% above analysts’ estimates. Its non-GAAP profit of $0.16 per share was in line with analysts’ consensus estimates.

Is now the time to buy Array? Find out by accessing our full research report, it’s free.

Array (ARRY) Q4 CY2024 Highlights:

- Revenue: $275.2 million vs analyst estimates of $267.7 million (19.4% year-on-year decline, 2.8% beat)

- Adjusted EPS: $0.16 vs analyst estimates of $0.17 (in line)

- Adjusted EBITDA: $45.2 million vs analyst estimates of $48.38 million (16.4% margin, 6.6% miss)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.1 billion at the midpoint, missing analyst estimates by 2.3% and implying 20.1% growth (vs -40.6% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $0.65 at the midpoint, missing analyst estimates by 19%

- EBITDA guidance for the upcoming financial year 2025 is $190 million at the midpoint, below analyst estimates of $237.6 million

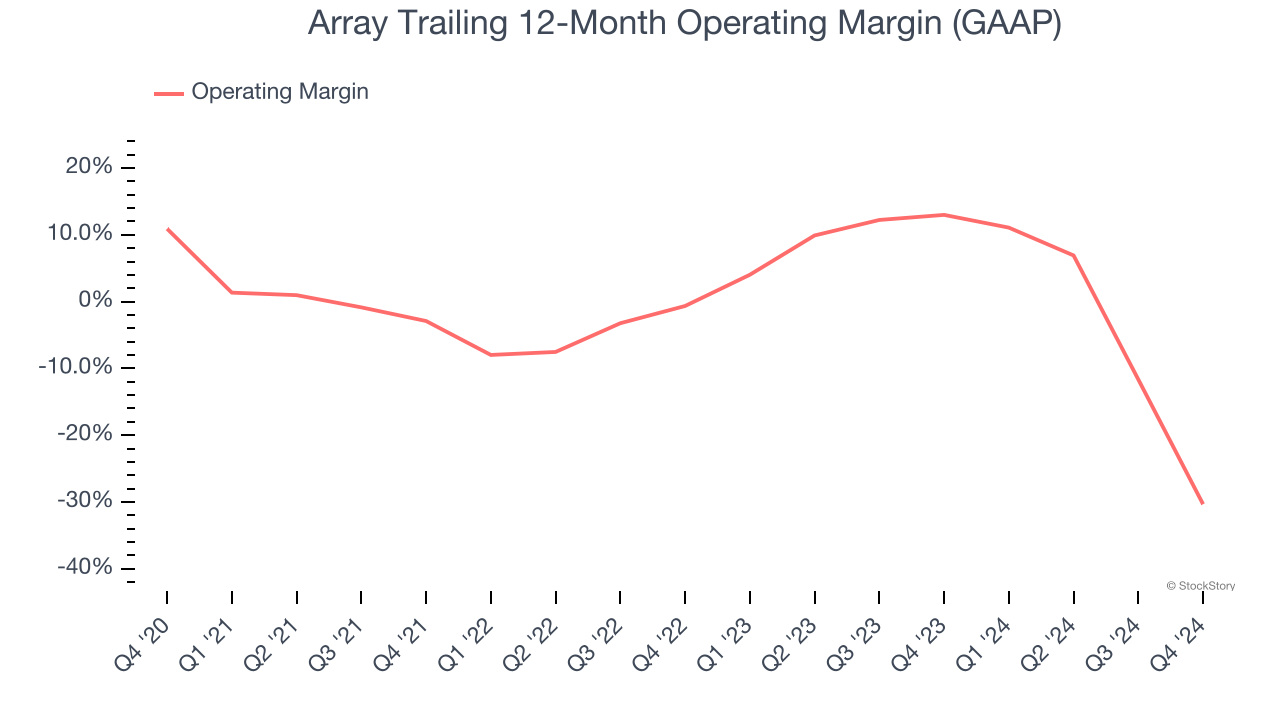

- Operating Margin: -51.7%, down from 6.1% in the same quarter last year

- Free Cash Flow Margin: 20.3%, down from 26% in the same quarter last year

- Market Capitalization: $1.04 billion

“ARRAY delivered strong fourth quarter and full year 2024 results, we exceeded the mid-point of our fourth quarter revenue guidance and achieved record gross margin on the full year. Our ongoing focus on operational execution continues to translate into robust profitability and healthy cash flow. We finished 2024 with an orderbook of $2 billion, representing 10% year-on-year growth. We are pleased with our results, which delivered significant progress in both market share and commercial growth. Thank you to our employees for their continued focus and hard work. Additionally, we are on track to deliver 100% domestic content solar trackers by the first half of 2025. Our OmniTrack™ product continues to gain traction in the market, and now accounts for over 20% of our orderbook. We are excited about our investment in Swap Robotics, a disruptive technology driving automation in PV installations. We believe the integration of Swap Robotics technology into our product portfolio will drive project efficiencies and cost savings for our customers,” said Chief Executive Officer, Kevin G. Hostetler.

Company Overview

Going public in October 2020, Array (NASDAQ:ARRY) is a global manufacturer of ground-mounting tracking systems for utility and distributed generation solar energy projects.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Array’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

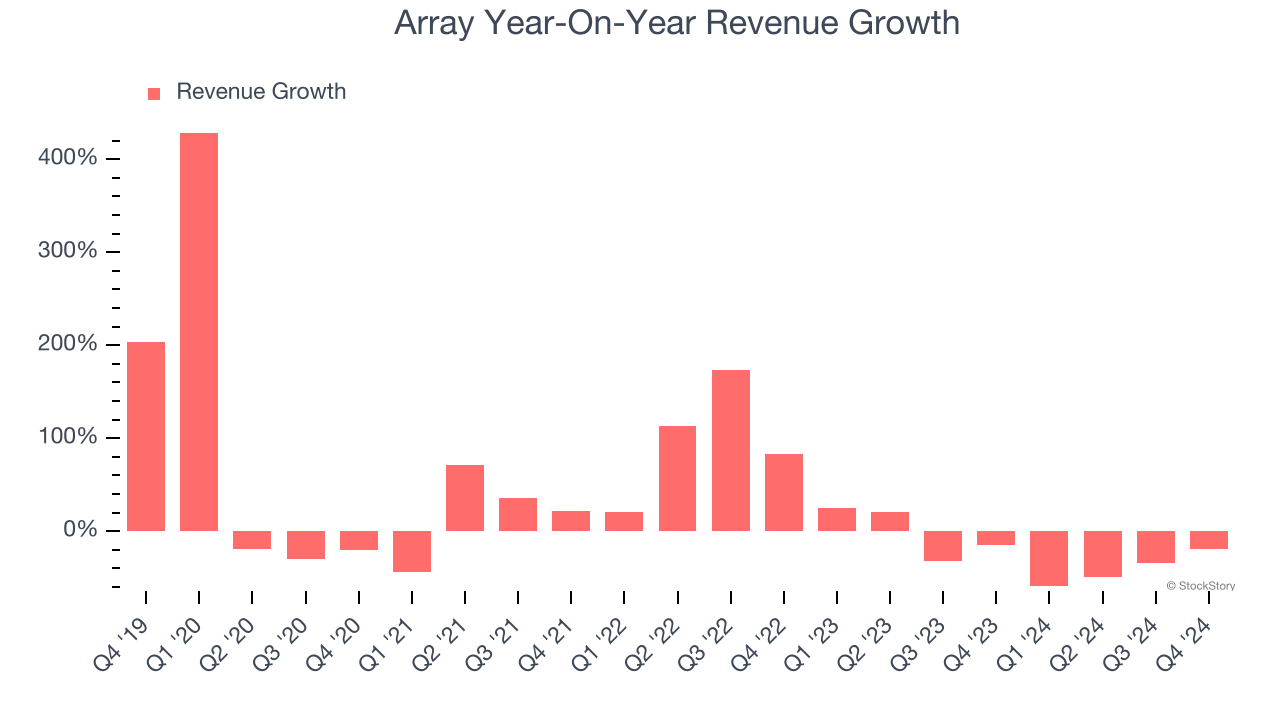

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Array’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 25.2% annually. Array isn’t alone in its struggles as the Renewable Energy industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Array’s revenue fell by 19.4% year on year to $275.2 million but beat Wall Street’s estimates by 2.8%. Company management is currently guiding for a 72.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Array was roughly breakeven when averaging the last five years of quarterly operating profits, one of the worst outcomes in the industrials sector. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Array’s operating margin decreased by 41.2 percentage points over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. . Array’s performance was poor no matter how you look at it - it shows costs were rising and that it couldn’t pass them onto its customers.

In Q4, Array generated a negative 51.7% operating margin. The company's consistent lack of profits raise a flag.

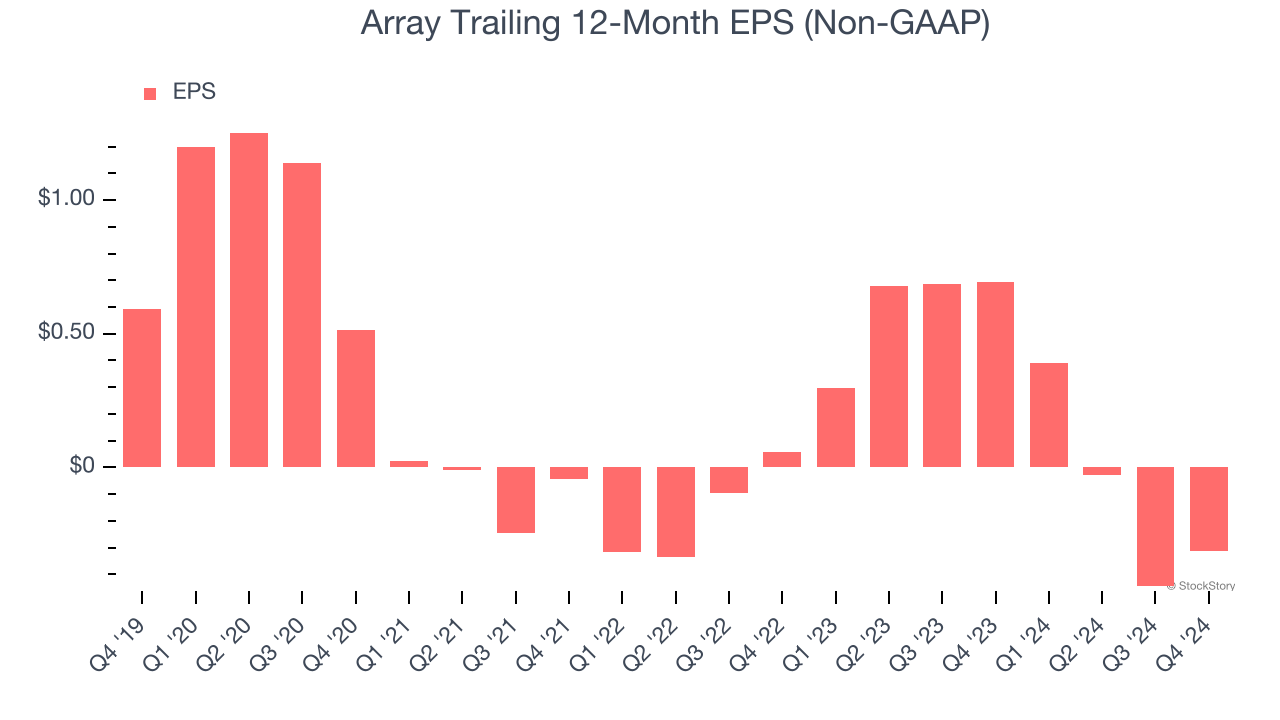

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Array, its EPS declined by 20.4% annually over the last five years while its revenue grew by 7.2%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Array’s earnings to better understand the drivers of its performance. As we mentioned earlier, Array’s operating margin declined by 41.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Array, its two-year annual EPS declines of 169% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Array reported EPS at $0.16, up from $0.03 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Array’s full-year EPS of negative $0.31 will flip to positive $0.78.

Key Takeaways from Array’s Q4 Results

We were impressed by Array’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed significantly and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 12.1% to $5.76 immediately after reporting.

Array underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.