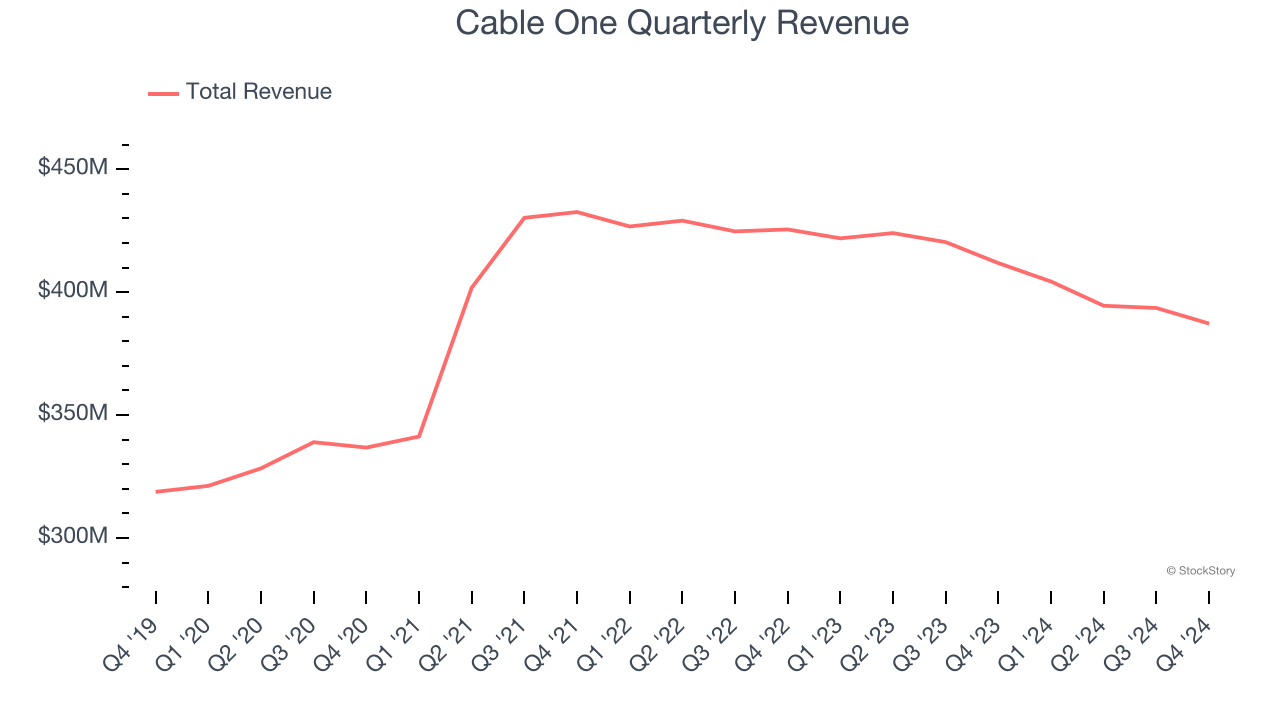

Internet, cable TV, and phone provider Cable One (NYSE:CABO) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 6% year on year to $387.2 million. Its GAAP loss of $18.71 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Cable One? Find out by accessing our full research report, it’s free.

Cable One (CABO) Q4 CY2024 Highlights:

- Revenue: $387.2 million vs analyst estimates of $389.4 million (6% year-on-year decline, 0.6% miss)

- EPS (GAAP): -$18.71 vs analyst estimates of $9.18 (significant miss due to other, non-recurring expenses not related to the regular operations of the business)

- Adjusted EBITDA: $211 million vs analyst estimates of $213.2 million (54.5% margin, 1% miss)

- Operating Margin: 26.2%, down from 30.9% in the same quarter last year

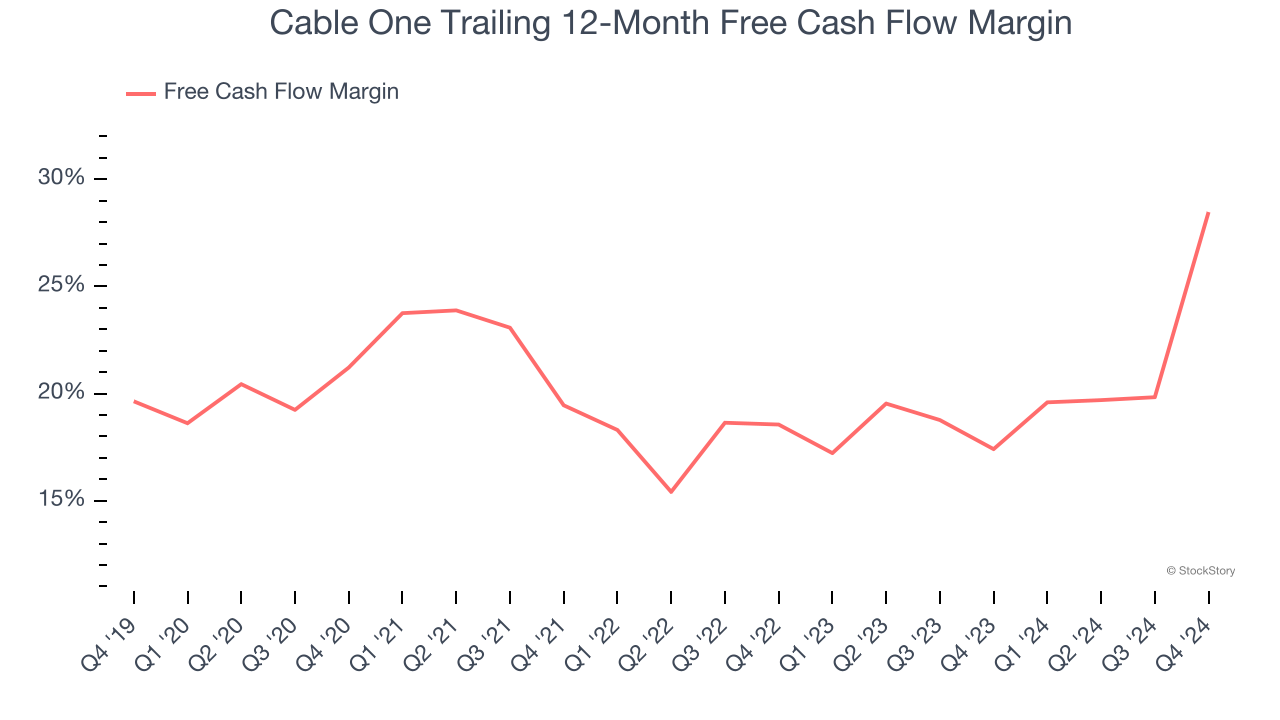

- Free Cash Flow Margin: 43.3%, up from 8.8% in the same quarter last year

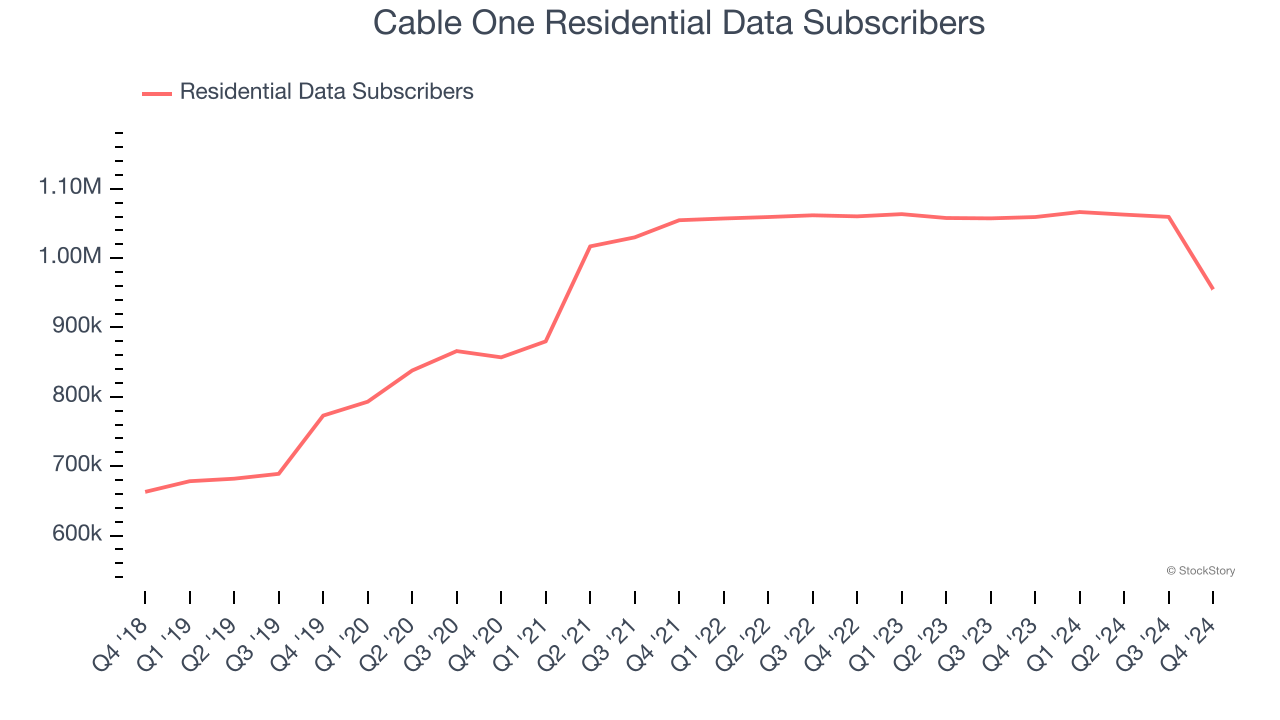

- Residential Data Subscribers: 955,000, down 104,300 year on year

- Market Capitalization: $1.47 billion

Company Overview

Founded in 1986, Cable One (NYSE:CABO) provides high-speed internet, cable television, and telephone services, primarily in smaller markets across the United States.

Wireless, Cable and Satellite

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

Sales Growth

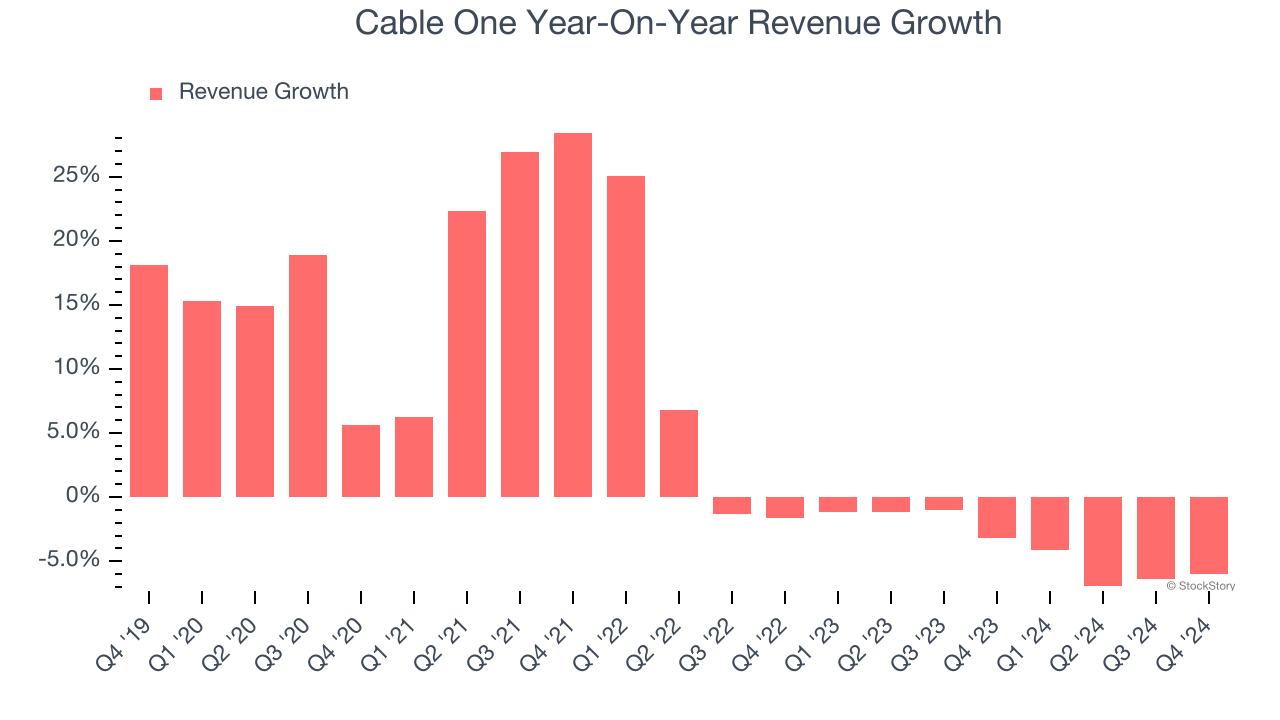

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Cable One’s 6.2% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Cable One’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.8% annually.

We can better understand the company’s revenue dynamics by analyzing its number of residential data subscribers and residential video subscribers, which clocked in at 955,000 and 107,400 in the latest quarter. Over the last two years, Cable One’s residential data subscribers averaged 1.1% year-on-year declines while its residential video subscribers averaged 23.9% year-on-year declines.

This quarter, Cable One missed Wall Street’s estimates and reported a rather uninspiring 6% year-on-year revenue decline, generating $387.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 2.4% over the next 12 months, similar to its two-year rate. While this projection is better than its two-year trend, it's hard to get excited about a company that is struggling with demand.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Cable One has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the consumer discretionary sector, averaging 22.8% over the last two years.

Cable One’s free cash flow clocked in at $167.6 million in Q4, equivalent to a 43.3% margin. This result was good as its margin was 34.5 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Cable One’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 28.5% for the last 12 months will decrease to 19.9%.

Key Takeaways from Cable One’s Q4 Results

We struggled to find many positives in these results. Its number of residential data subscribers missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $266.50 immediately after reporting.

Cable One’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.