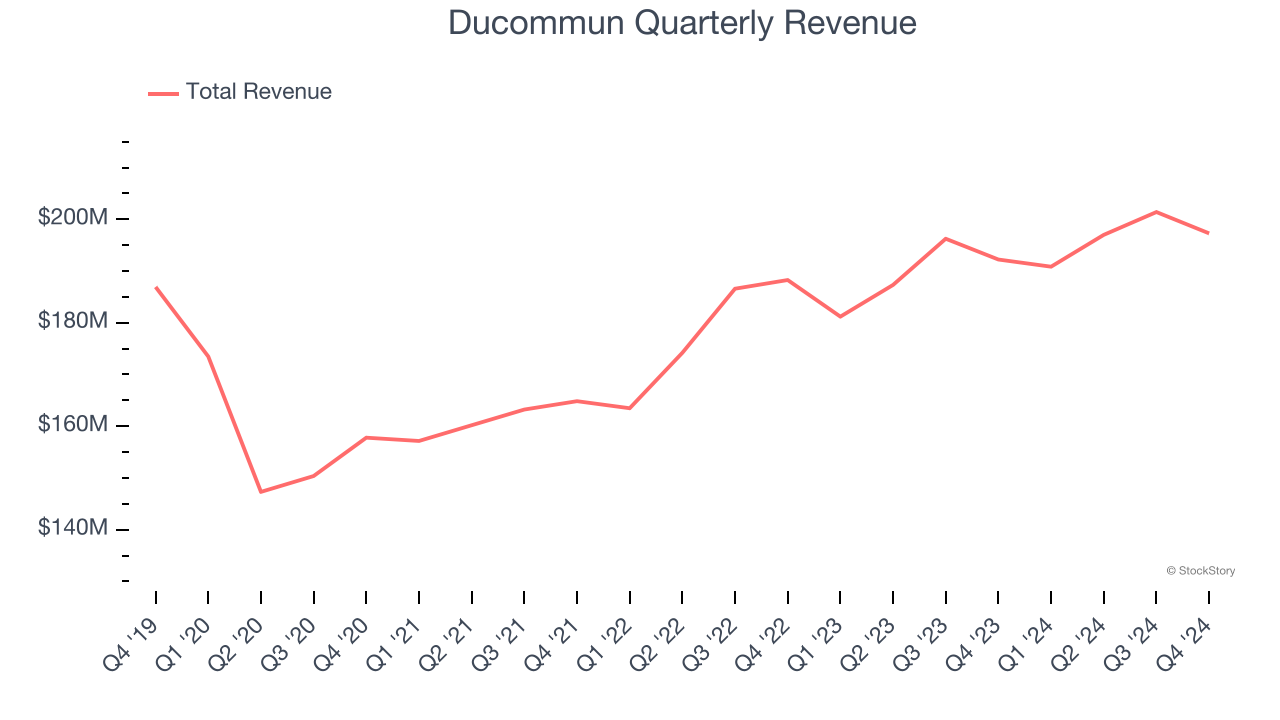

Aerospace and defense company Ducommun (NYSE:DCO) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 2.6% year on year to $197.3 million. Its non-GAAP profit of $0.75 per share was 7.9% below analysts’ consensus estimates.

Is now the time to buy Ducommun? Find out by accessing our full research report, it’s free.

Ducommun (DCO) Q4 CY2024 Highlights:

- Revenue: $197.3 million vs analyst estimates of $195.1 million (2.6% year-on-year growth, 1.1% beat)

- Adjusted EPS: $0.75 vs analyst expectations of $0.81 (7.9% miss)

- Adjusted EBITDA: $27.3 million vs analyst estimates of $30.42 million (13.8% margin, 10.2% miss)

- Operating Margin: 5.3%, in line with the same quarter last year

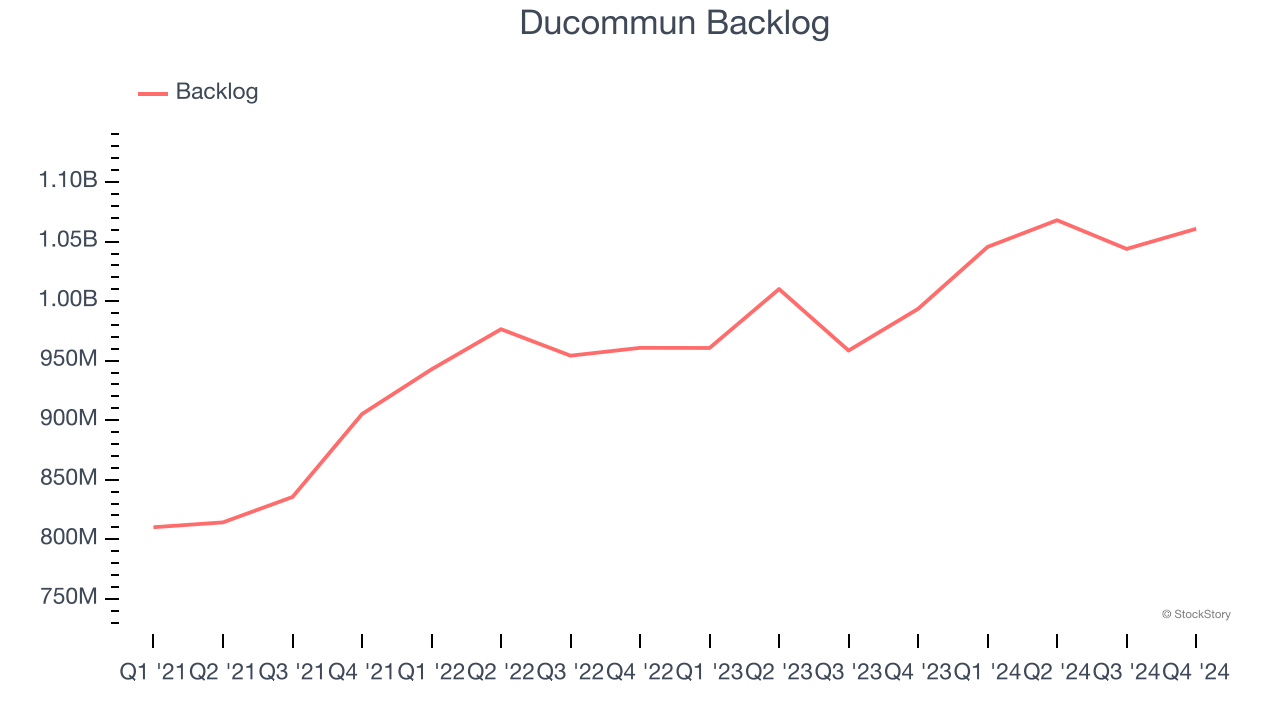

- Backlog: $1.06 billion at quarter end, up 6.8% year on year

- Market Capitalization: $906.9 million

“We made excellent progress in our VISION 2027 commitments in 2024 with the bright spots being earnings, EBITDA margins and reaching 23% of revenue for Engineered Products. In addition, I am very happy to report that the Company reached an all-time revenue record for the second consecutive year in 2024. In Q4 we continued the top-line growth story for Ducommun, led by our military and space business,” said Stephen G. Oswald, chairman, president and chief executive officer.

Company Overview

California’s oldest company, Ducommun (NYSE:DCO) is a provider of engineering and manufacturing services for high-performance products primarily within the aerospace and defense industries.

Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Sales Growth

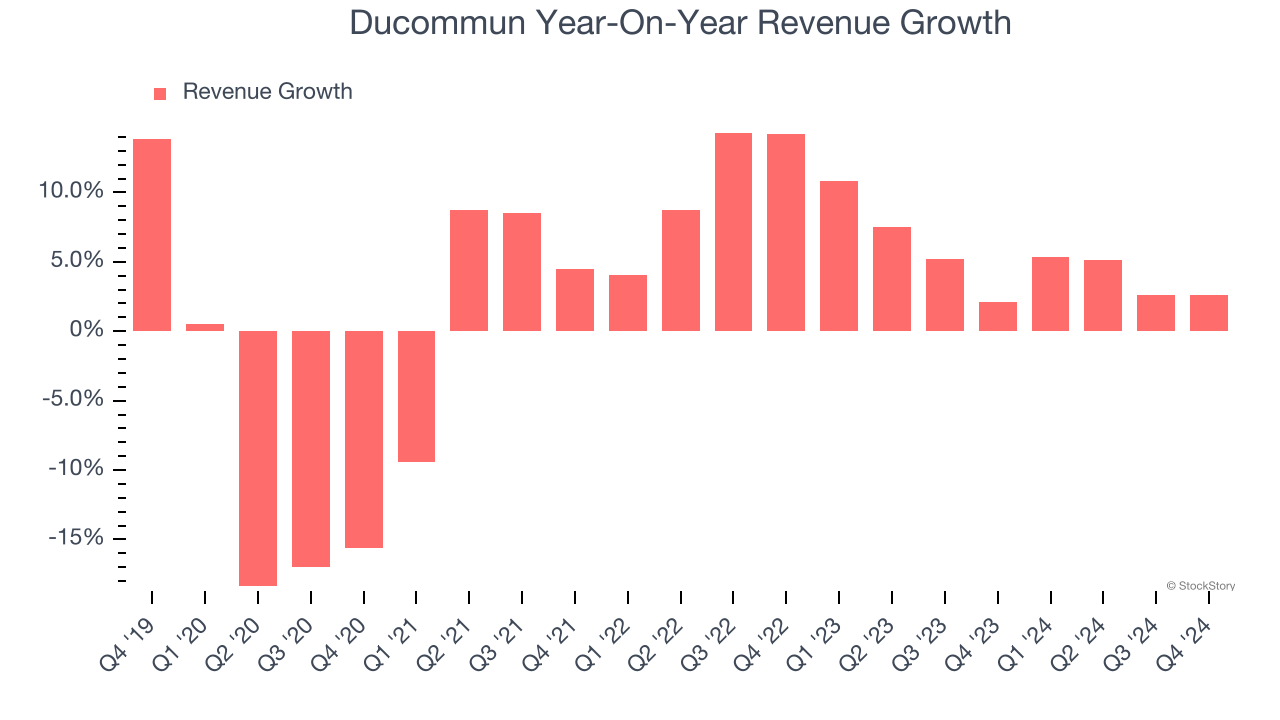

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Ducommun’s sales grew at a sluggish 1.8% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Ducommun’s annualized revenue growth of 5.1% over the last two years is above its five-year trend, but we were still disappointed by the results.

Ducommun also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Ducommun’s backlog reached $1.06 billion in the latest quarter and averaged 4.9% year-on-year growth over the last two years. Because this number is in line with its revenue growth, we can see the company effectively balanced its new order intake and fulfillment processes.

This quarter, Ducommun reported modest year-on-year revenue growth of 2.6% but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

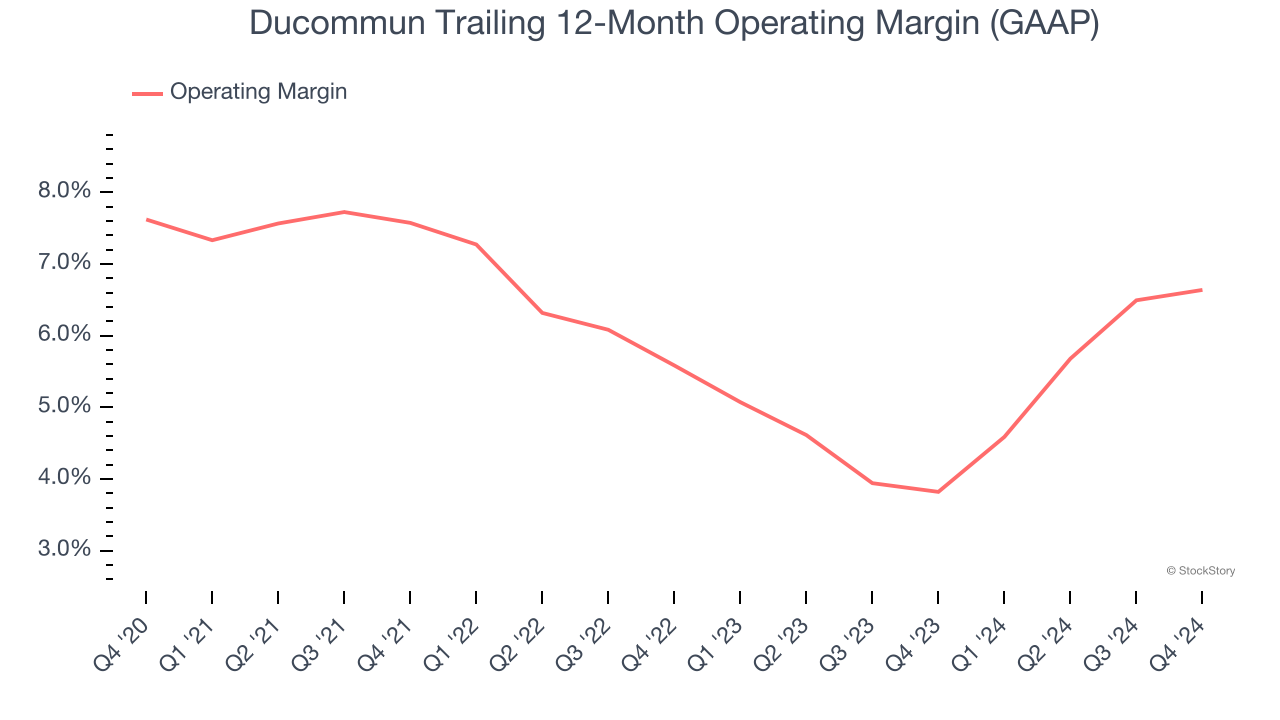

Operating Margin

Ducommun was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.2% was weak for an industrials business.

Analyzing the trend in its profitability, Ducommun’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Ducommun generated an operating profit margin of 5.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

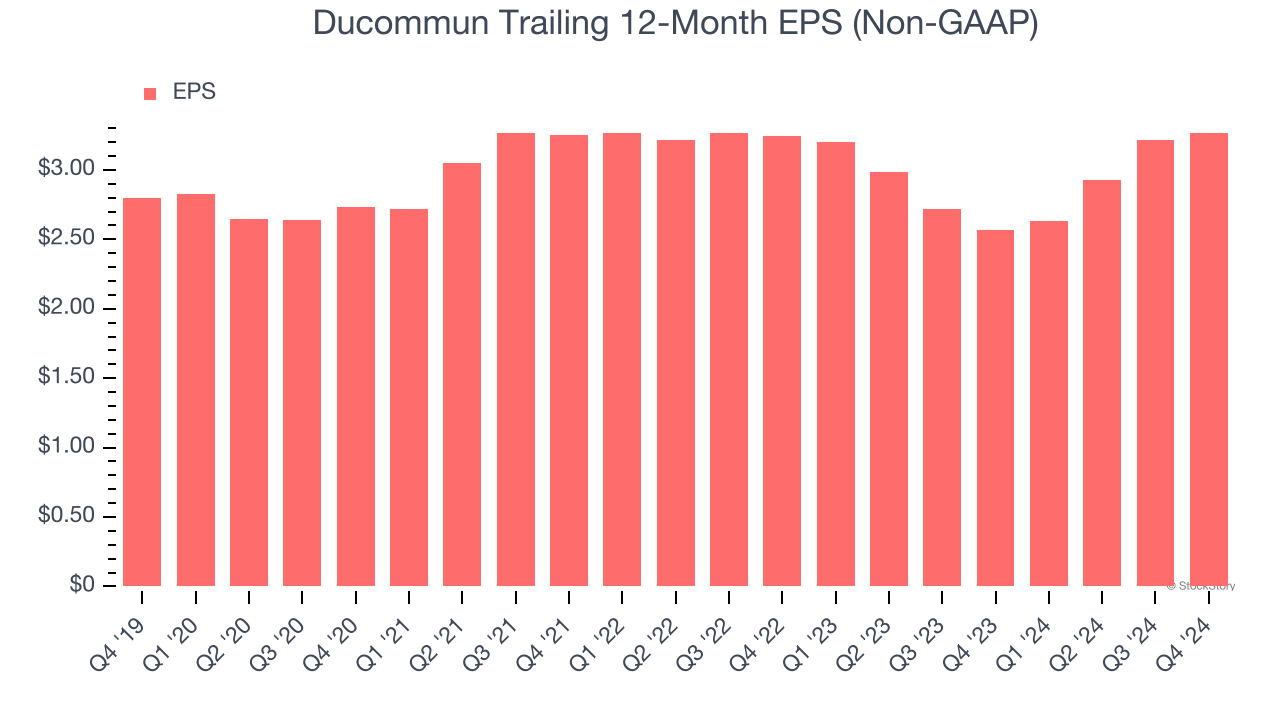

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Ducommun’s EPS grew at a weak 3.1% compounded annual growth rate over the last five years. This performance was better than its flat revenue, but we take it with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Ducommun’s flat two-year EPS performance was subpar and lower than its 5.1% two-year revenue growth.

In Q4, Ducommun reported EPS at $0.75, up from $0.70 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Ducommun’s full-year EPS of $3.27 to grow 20.4%.

Key Takeaways from Ducommun’s Q4 Results

It was good to see Ducommun narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed significantly and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.7% to $60.30 immediately following the results.

Ducommun’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.