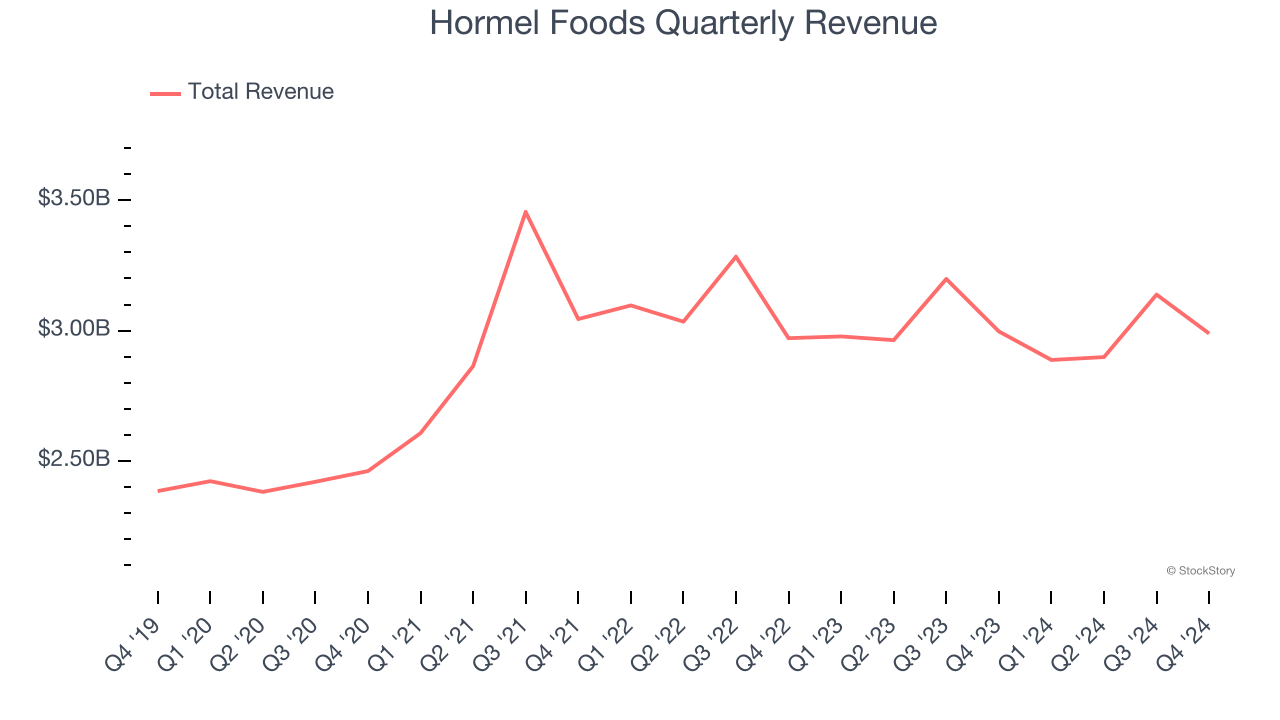

Packaged foods company Hormel (NYSE:HRL) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, but sales were flat year on year at $2.99 billion. The company expects the full year’s revenue to be around $12.05 billion, close to analysts’ estimates. Its non-GAAP profit of $0.35 per share was 8% below analysts’ consensus estimates.

Is now the time to buy Hormel Foods? Find out by accessing our full research report, it’s free.

Hormel Foods (HRL) Q4 CY2024 Highlights:

- Revenue: $2.99 billion vs analyst estimates of $2.95 billion (flat year on year, 1.3% beat)

- Adjusted EPS: $0.35 vs analyst expectations of $0.38 (8% miss)

- Adjusted EBITDA: $294.2 million vs analyst estimates of $342.6 million (9.8% margin, 14.1% miss)

- The company reconfirmed its revenue guidance for the full year of $12.05 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $1.65 at the midpoint

- Operating Margin: 7.6%, down from 9.5% in the same quarter last year

- Free Cash Flow Margin: 7.9%, down from 11.9% in the same quarter last year

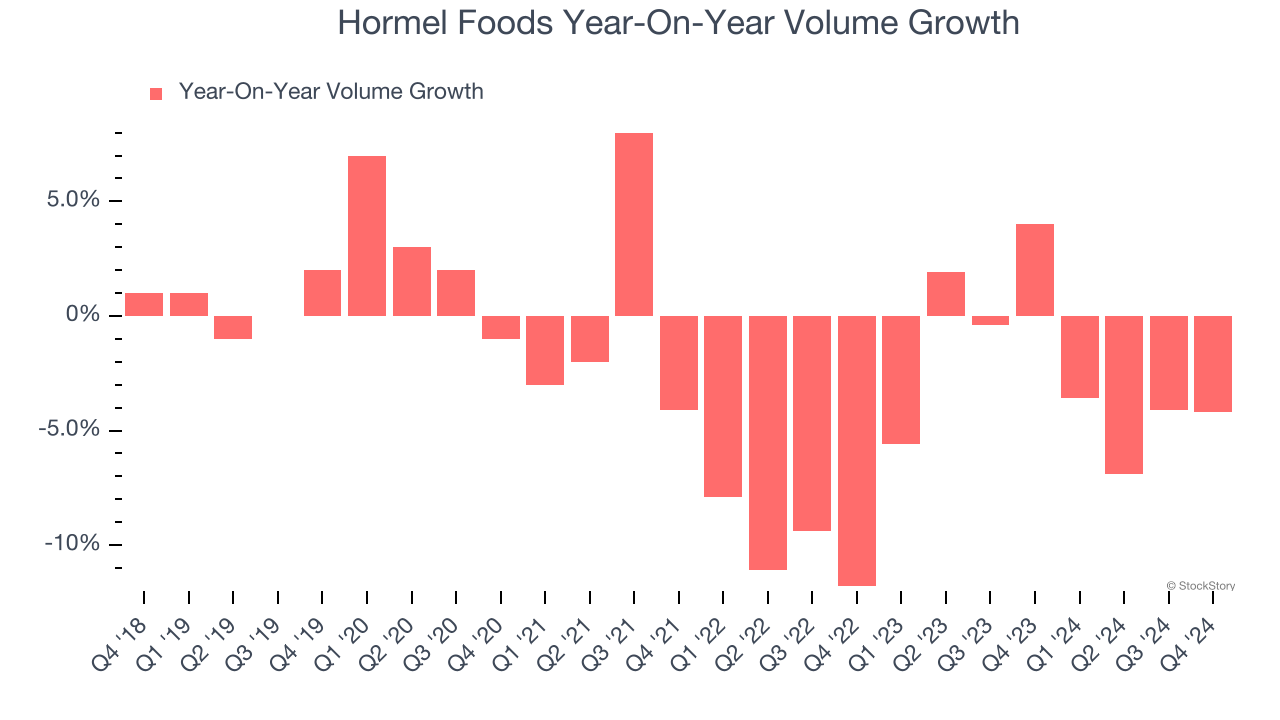

- Sales Volumes fell 4.2% year on year (4% in the same quarter last year)

- Market Capitalization: $15.77 billion

Company Overview

Best known for its SPAM brand, Hormel (NYSE:HRL) is a packaged foods company with products that span meat, poultry, shelf-stable foods, and spreads.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $11.91 billion in revenue over the past 12 months, Hormel Foods is one of the larger consumer staples companies and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To accelerate sales, Hormel Foods must lean into newer products.

As you can see below, Hormel Foods struggled to increase demand as its $11.91 billion of sales for the trailing 12 months was close to its revenue three years ago. This is mainly because consumers bought less of its products - we’ll explore what this means in the "Volume Growth" section.

This quarter, Hormel Foods’s $2.99 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months. While this projection suggests its newer products will fuel better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Hormel Foods’s average quarterly sales volumes have shrunk by 2.4% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

In Hormel Foods’s Q4 2025, sales volumes dropped 4.2% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from Hormel Foods’s Q4 Results

It was good to see Hormel Foods narrowly top analysts’ revenue expectations this quarter. The company also reaffirmed full-year guidance for revenue and EPS, a sign that the business is squarely on track with no surprises. Overall, this quarter wasn't perfect, but it was fine. The stock traded up 1.1% to $29.04 immediately following the results.

So do we think Hormel Foods is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.