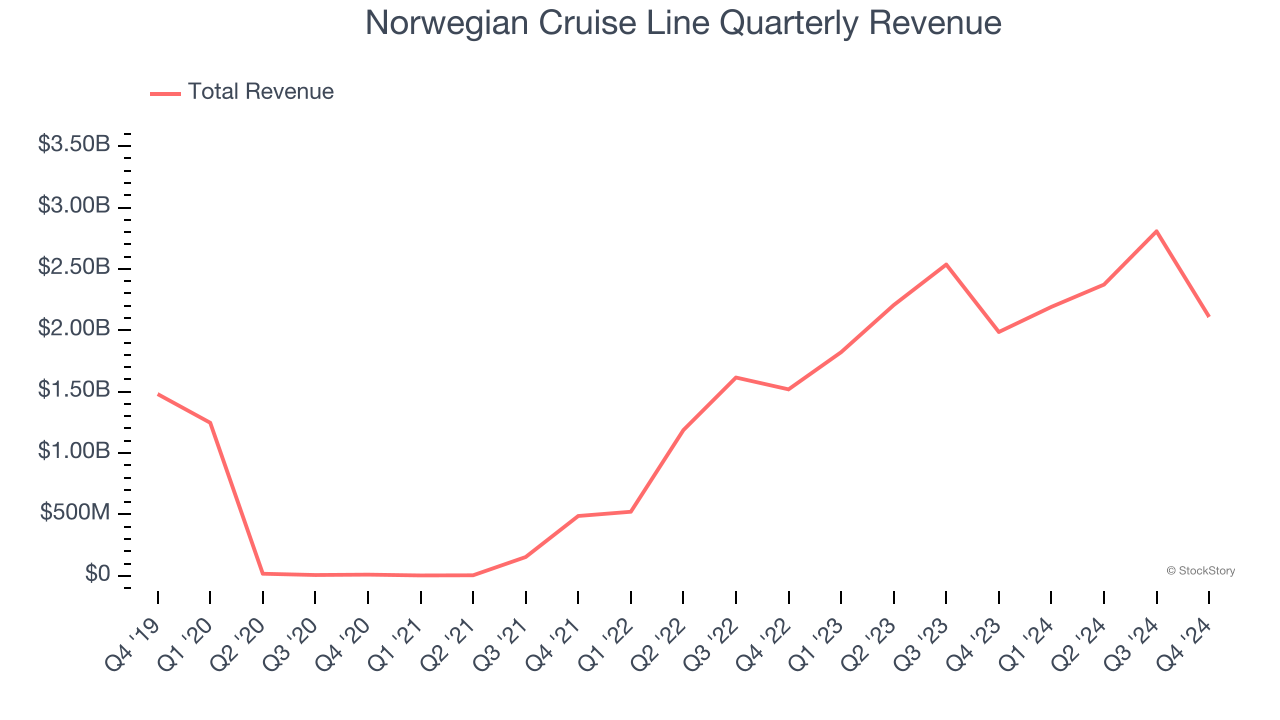

Cruise company Norwegian Cruise Line (NYSE:NCLH) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 6.2% year on year to $2.11 billion. Its non-GAAP profit of $0.26 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Norwegian Cruise Line? Find out by accessing our full research report, it’s free.

Norwegian Cruise Line (NCLH) Q4 CY2024 Highlights:

- Revenue: $2.11 billion vs analyst estimates of $2.10 billion (6.2% year-on-year growth, in line)

- Adjusted EPS: $0.26 vs analyst estimates of $0.11 (significant beat)

- Adjusted EBITDA: $468.2 million vs analyst estimates of $450.9 million (22.2% margin, 3.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $2.05 at the midpoint, missing analyst estimates by 2%

- EBITDA guidance for the upcoming financial year 2025 is $2.72 billion at the midpoint, below analyst estimates of $2.75 billion

- Operating Margin: 10.2%, up from 6.3% in the same quarter last year

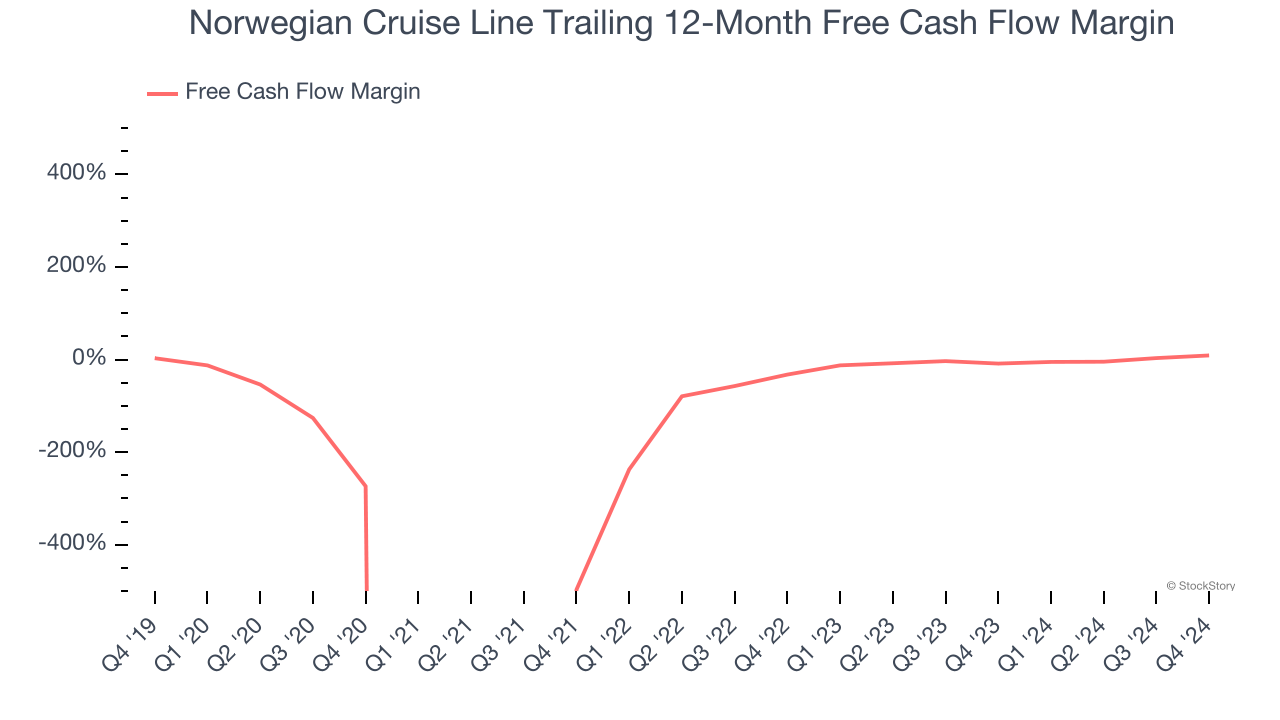

- Free Cash Flow was $155.8 million, up from -$388.7 million in the same quarter last year

- Passenger Cruise Days: 5.88 million, in line with the same quarter last year

- Market Capitalization: $11.01 billion

“2024 was marked by strategic and transformative milestones for Norwegian Cruise Line Holdings. From launching our Charting the Course strategy, announcing an ambitious newbuild program and the construction of our Great Stirrup Cay pier, and successfully executing brand initiatives and new guest experiences across our entire portfolio, we have laid out a solid foundation for an exciting future,” said Harry Sommer, president and chief executive officer of Norwegian Cruise Line Holdings Ltd.

Company Overview

With amenities like a full go-kart race track built into its ships, Norwegian Cruise Line (NYSE:NCLH) is a premier global cruise company.

Travel and Vacation Providers

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Sales Growth

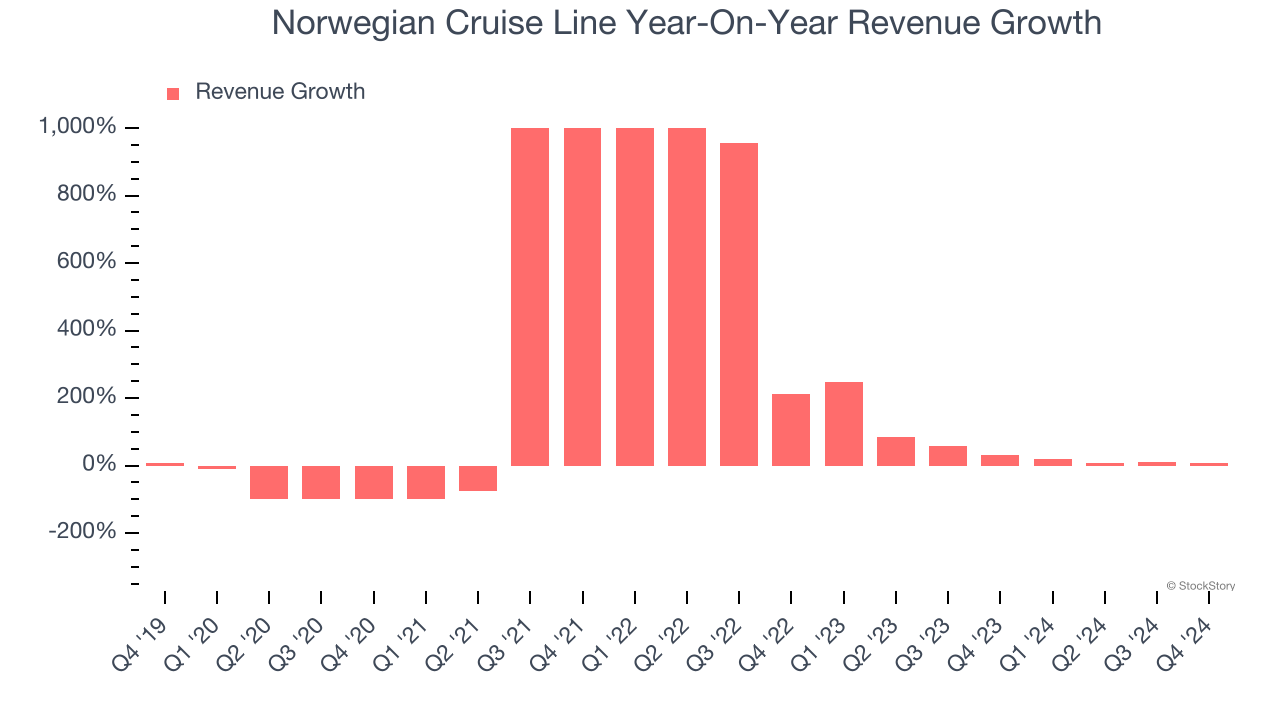

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Norwegian Cruise Line’s 8% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Norwegian Cruise Line’s annualized revenue growth of 39.9% over the last two years is above its five-year trend, suggesting its demand recently accelerated. Note that COVID hurt Norwegian Cruise Line’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its number of passenger cruise days, which reached 5.88 million in the latest quarter. Over the last two years, Norwegian Cruise Line’s passenger cruise days were flat. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Norwegian Cruise Line grew its revenue by 6.2% year on year, and its $2.11 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Norwegian Cruise Line broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders. The divergence from its good operating margin stems from its capital-intensive business model, which requires Norwegian Cruise Line to make large cash investments in working capital and capital expenditures.

Norwegian Cruise Line’s free cash flow clocked in at $155.8 million in Q4, equivalent to a 7.4% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Norwegian Cruise Line’s Q4 Results

We were impressed by that Norwegian Cruise Line beat analysts’ EBITDA and EPS expectations this quarter. On the other hand, its EBITDA guidance for next quarter missed. Overall, this quarter was mixed. The stock traded up 2.4% to $25.65 immediately following the results.

So do we think Norwegian Cruise Line is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.