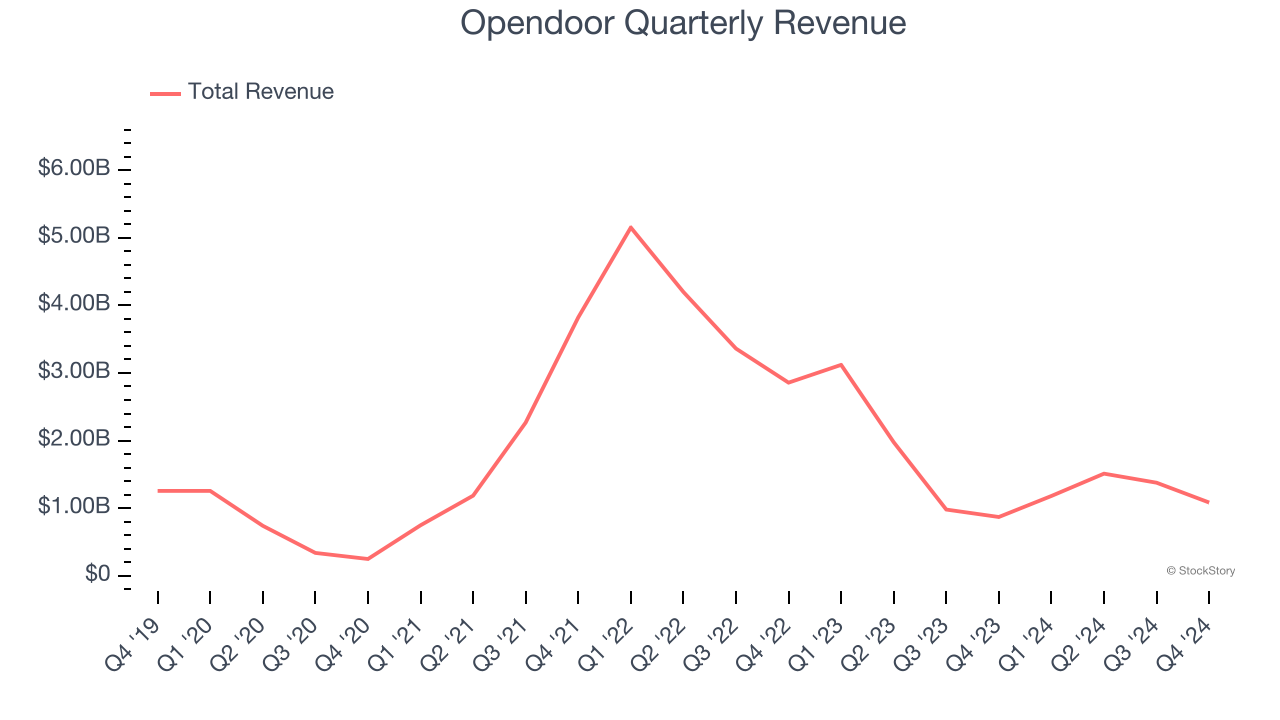

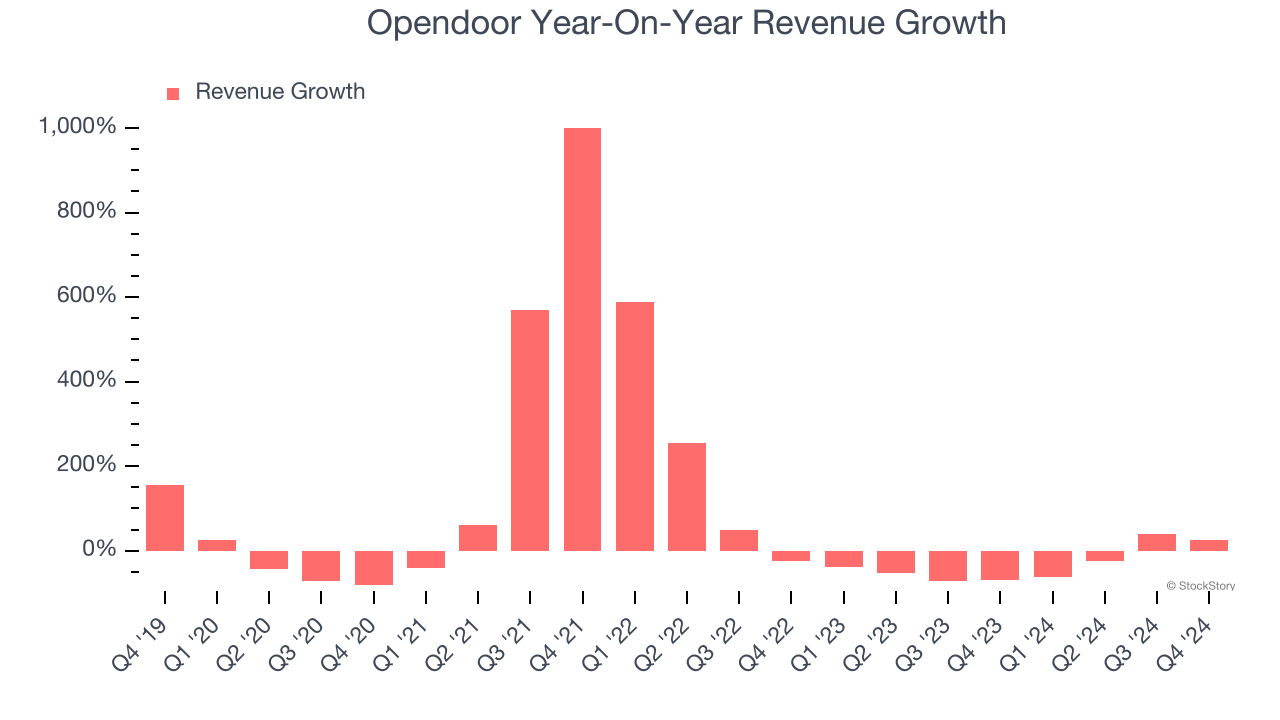

Technology real estate company Opendoor (NASDAQ:OPEN) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 24.6% year on year to $1.08 billion. On the other hand, next quarter’s revenue guidance of $1.04 billion was less impressive, coming in 18.4% below analysts’ estimates. Its GAAP loss of $0.16 per share was in line with analysts’ consensus estimates.

Is now the time to buy Opendoor? Find out by accessing our full research report, it’s free.

Opendoor (OPEN) Q4 CY2024 Highlights:

- Revenue: $1.08 billion vs analyst estimates of $977.9 million (24.6% year-on-year growth, 10.8% beat)

- EPS (GAAP): -$0.16 vs analyst estimates of -$0.16 (in line)

- Adjusted EBITDA: -$49 million vs analyst estimates of -$66.23 million (-4.5% margin, 26% beat)

- Revenue Guidance for Q1 CY2025 is $1.04 billion at the midpoint, below analyst estimates of $1.27 billion

- EBITDA guidance for Q1 CY2025 is -$45 million at the midpoint, below analyst estimates of -$18.94 million

- Operating Margin: -8.7%, up from -13.2% in the same quarter last year

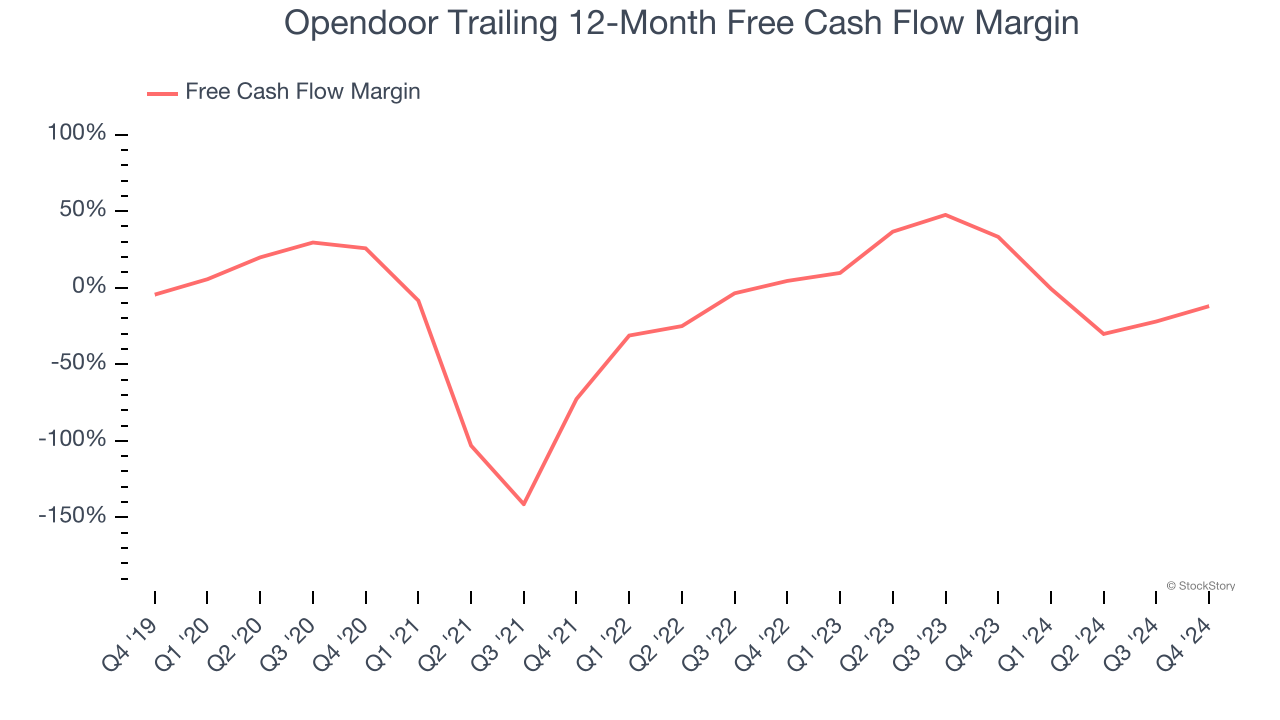

- Free Cash Flow was -$83 million compared to -$551 million in the same quarter last year

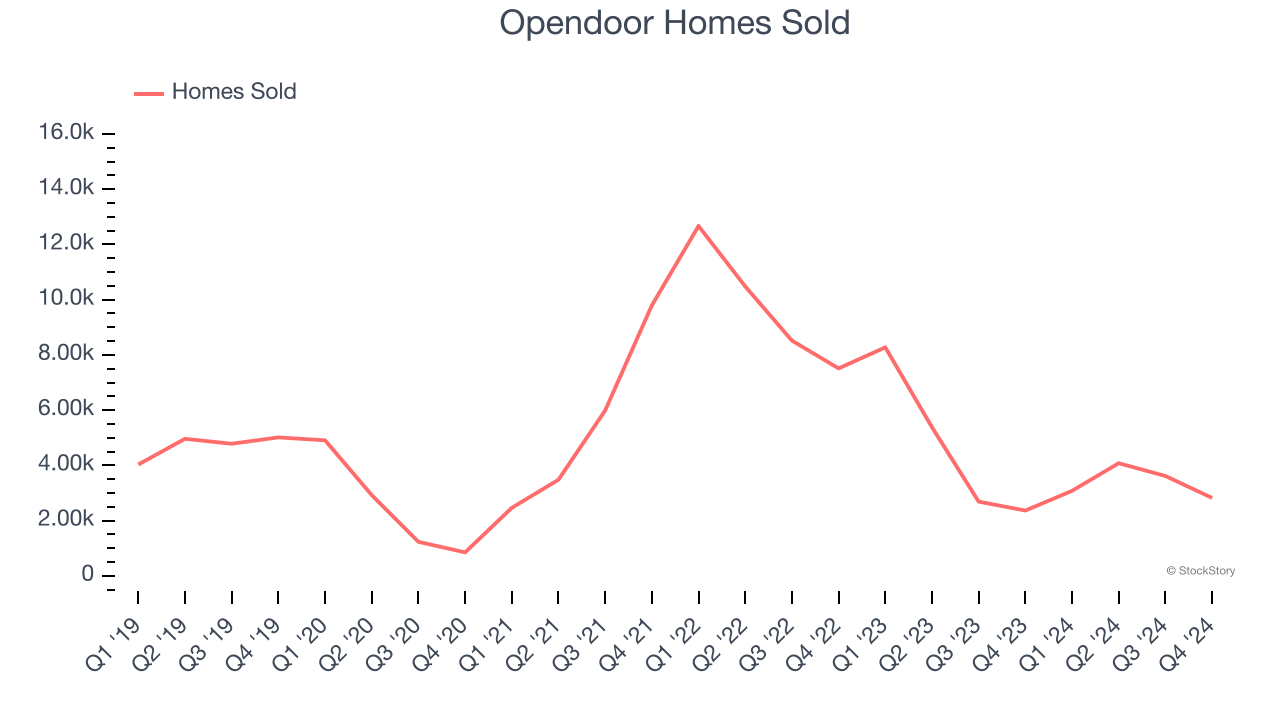

- Homes Sold: 2,822, up 458 year on year

- Market Capitalization: $1.10 billion

"In 2024, we took decisive actions to streamline operations and optimize our cost structure to better position the Company to navigate the persistent housing market headwinds and drive toward our longer-term profitability target. As a result, we significantly reduced Adjusted Net Losses in the fourth quarter and for the year while delivering year-over-year revenue growth and improvements to Contribution Profit and Adjusted EBITDA," said Carrie Wheeler, CEO of Opendoor.

Company Overview

Founded by real estate guru Eric Wu, Opendoor (NASDAQ:OPEN) offers a technology-driven, convenient, and streamlined process to buy and sell homes.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Opendoor’s sales grew at a weak 1.7% compounded annual growth rate over the last five years. This was below our standards and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Opendoor’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 42.5% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of homes sold, which reached 2,822 in the latest quarter. Over the last two years, Opendoor’s homes sold averaged 31.7% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Opendoor reported robust year-on-year revenue growth of 24.6%, and its $1.08 billion of revenue topped Wall Street estimates by 10.8%. Company management is currently guiding for a 12.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17.9% over the next 12 months, an improvement versus the last two years. This projection is admirable and suggests its newer products and services will catalyze better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Opendoor has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 13.9% over the last two years, better than the broader consumer discretionary sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Opendoor burned through $83 million of cash in Q4, equivalent to a negative 7.7% margin. The company’s cash burn slowed from $551 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Over the next year, analysts predict Opendoor will continue burning cash, albeit to a lesser extent. Their consensus estimates imply its free cash flow margin of negative 12% for the last 12 months will increase to negative 3.9%.

Key Takeaways from Opendoor’s Q4 Results

We were impressed by how significantly Opendoor blew past analysts’ revenue and EBITDA expectations this quarter. On the other hand, its quarterly guidance for both metrics fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.5% to $1.39 immediately after reporting.

Opendoor’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.