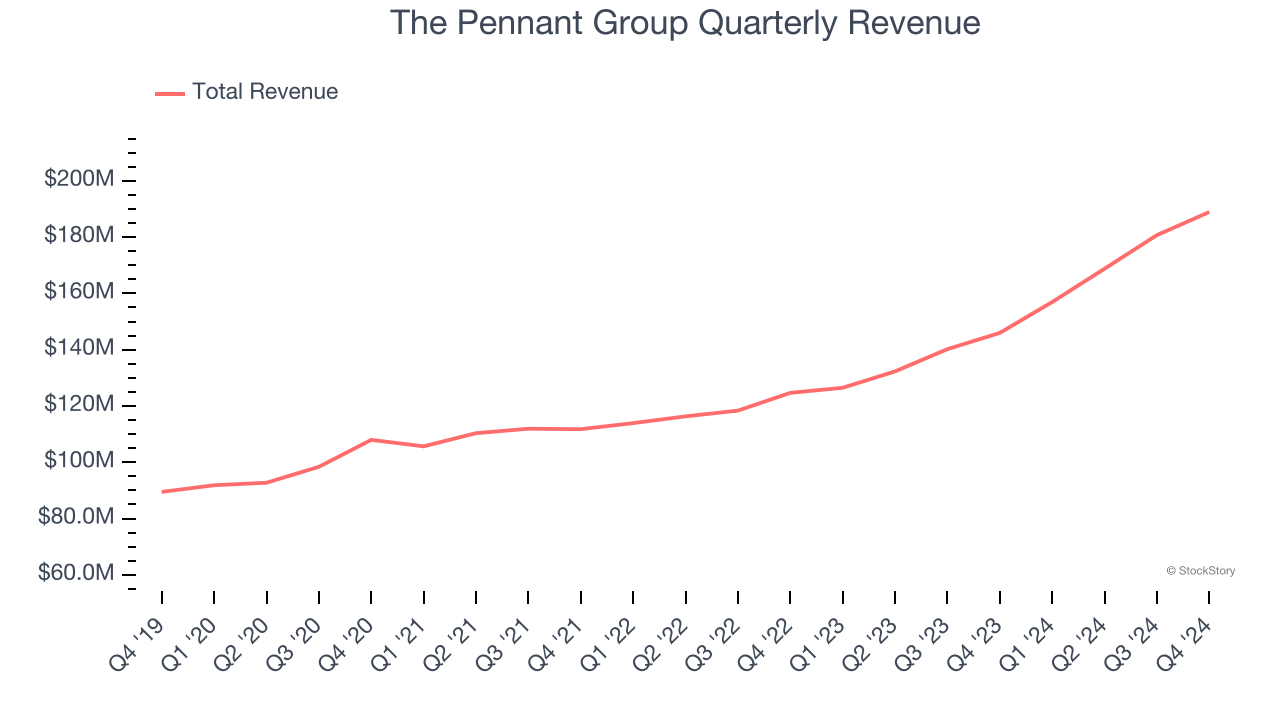

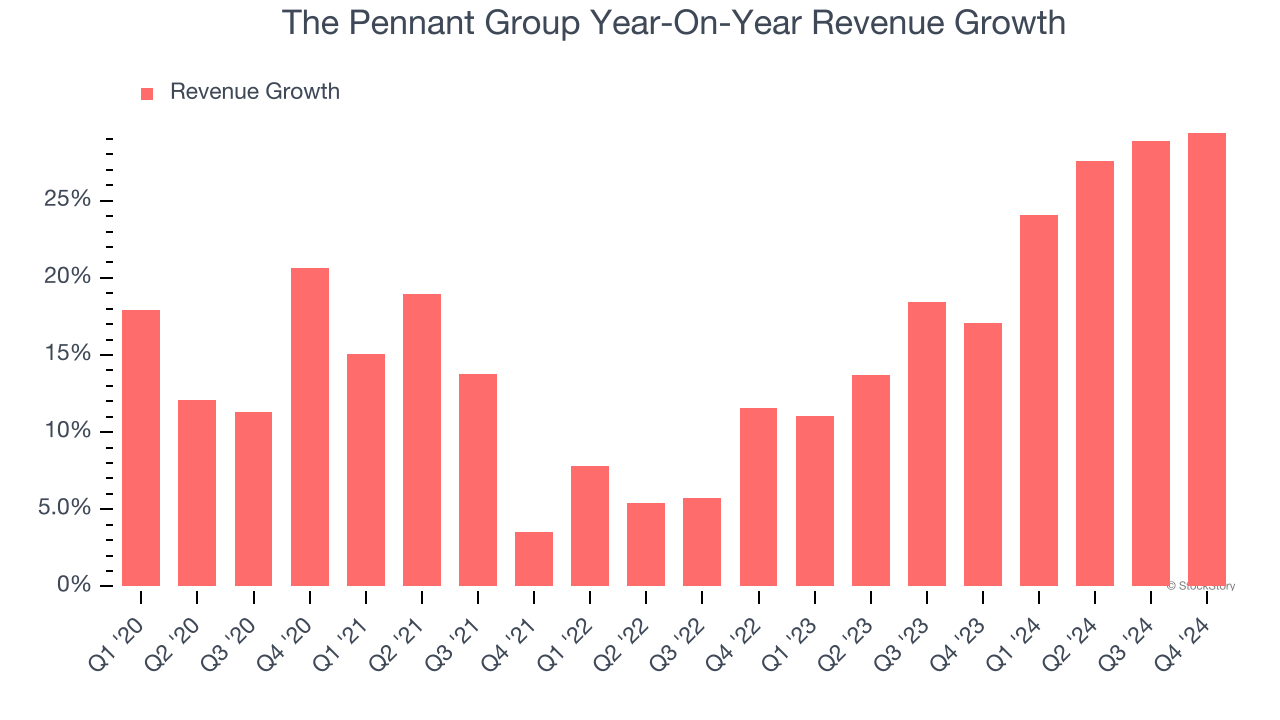

Senior living provider The Pennant Group (NASDAQ:PNTG) reported Q4 CY2024 results exceeding the market’s revenue expectations, with sales up 29.4% year on year to $188.9 million. The company’s full-year revenue guidance of $832.5 million at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $0.24 per share was in line with analysts’ consensus estimates.

Is now the time to buy The Pennant Group? Find out by accessing our full research report, it’s free.

The Pennant Group (PNTG) Q4 CY2024 Highlights:

- Revenue: $188.9 million vs analyst estimates of $186.3 million (29.4% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.24 vs analyst estimates of $0.24 (in line)

- Adjusted EBITDA: $13.76 million vs analyst estimates of $14.58 million (7.3% margin, 5.6% miss)

- Management’s revenue guidance for the upcoming financial year 2025 is $832.5 million at the midpoint, beating analyst estimates by 2% and implying 19.7% growth (vs 27.5% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $1.07 at the midpoint, missing analyst estimates by 0.7%

- EBITDA guidance for the upcoming financial year 2025 is $65.65 million at the midpoint, below analyst estimates of $66.18 million

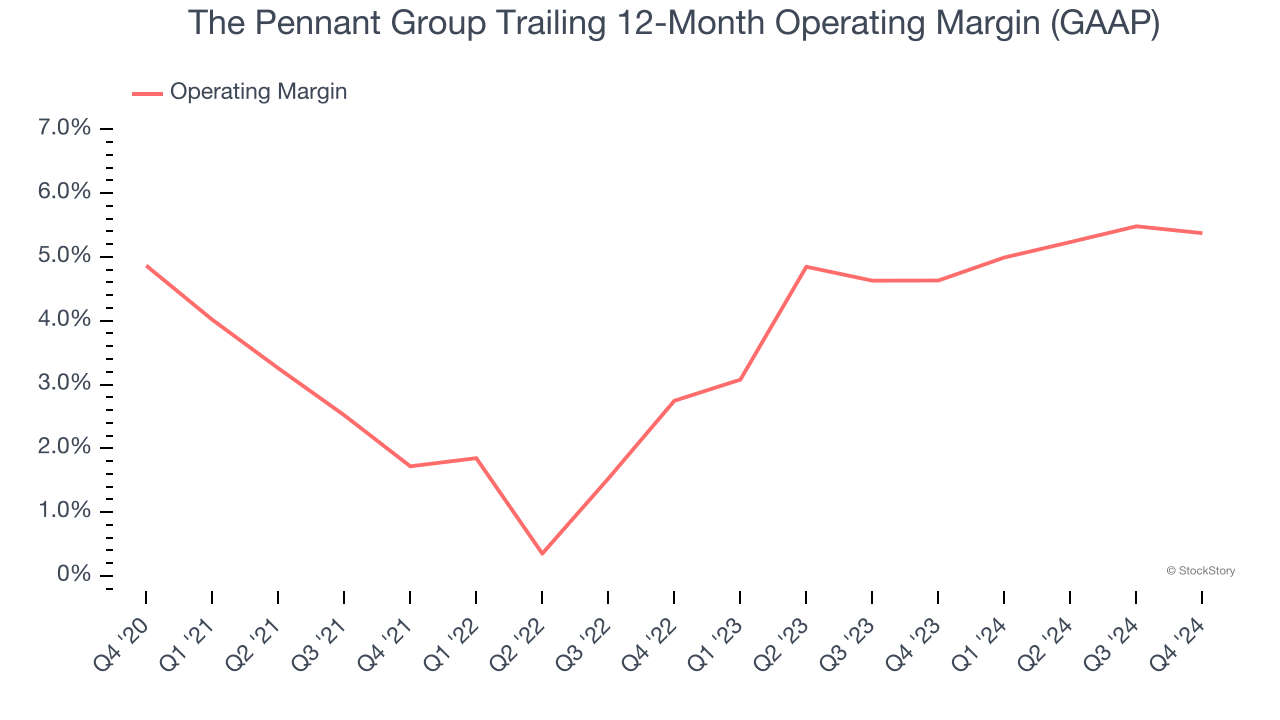

- Operating Margin: 4.9%, in line with the same quarter last year

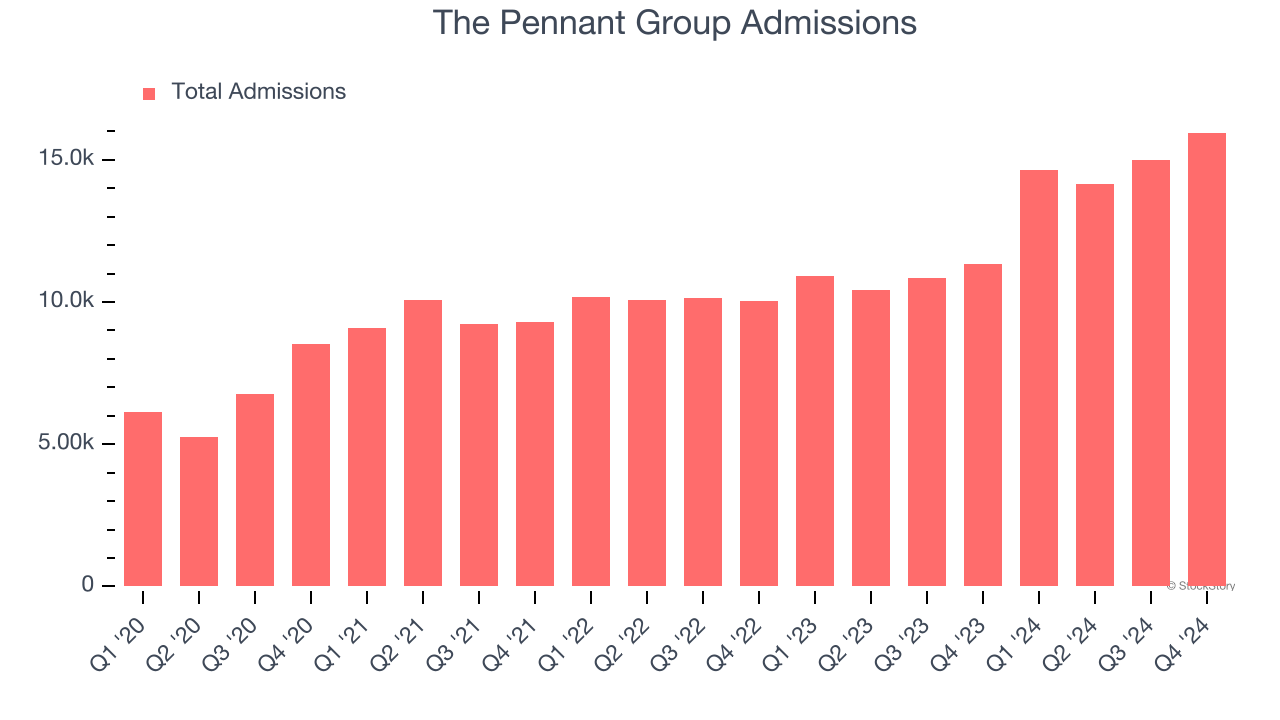

- Sales Volumes rose 40.9% year on year (12.8% in the same quarter last year)

- Market Capitalization: $875.9 million

“We are pleased to conclude a remarkable year, with strong performance in revenue, adjusted EBITDA, and adjusted earnings per share,” said Brent Guerisoli, the Company’s Chief Executive Officer.

Company Overview

Founded in 2019, The Pennant Group (NASDAQ:PNTG) offers senior living and home healthcare services with a focus on skilled nursing and assisted living.

Senior Health, Home Health & Hospice

The senior health, home care, and hospice care industries provide essential services to aging populations and patients with chronic or terminal conditions. These companies benefit from stable, recurring revenue driven by relationships with patients and families that can extend many months or even years. However, the labor-intensive nature of the business makes it vulnerable to rising labor costs and staffing shortages, while profitability is constrained by reimbursement rates from Medicare, Medicaid, and private insurers. Looking ahead, the industry is positioned for tailwinds from an aging population, increasing chronic disease prevalence, and a growing preference for personalized in-home care. Advancements in remote monitoring and telehealth are expected to enhance efficiency and care delivery. However, headwinds such as labor shortages, wage inflation, and regulatory uncertainty around reimbursement could pose challenges. Investments in digitization and technology-driven care will be critical for long-term success.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Thankfully, The Pennant Group’s 15.5% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. The Pennant Group’s annualized revenue growth of 21.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

The Pennant Group also reports its number of admissions, which reached 15,959 in the latest quarter. Over the last two years, The Pennant Group’s admissions averaged 22.4% year-on-year growth. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, The Pennant Group reported robust year-on-year revenue growth of 29.4%, and its $188.9 million of revenue topped Wall Street estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 17.7% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and implies the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

The Pennant Group was profitable over the last five years but held back by its large cost base. Its average operating margin of 4% was weak for a healthcare business.

Looking at the trend in its profitability, The Pennant Group’s operating margin of 5.4% for the trailing 12 months may be around the same as five years ago, but it has increased by 2.6 percentage points over the last two years.

In Q4, The Pennant Group generated an operating profit margin of 4.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

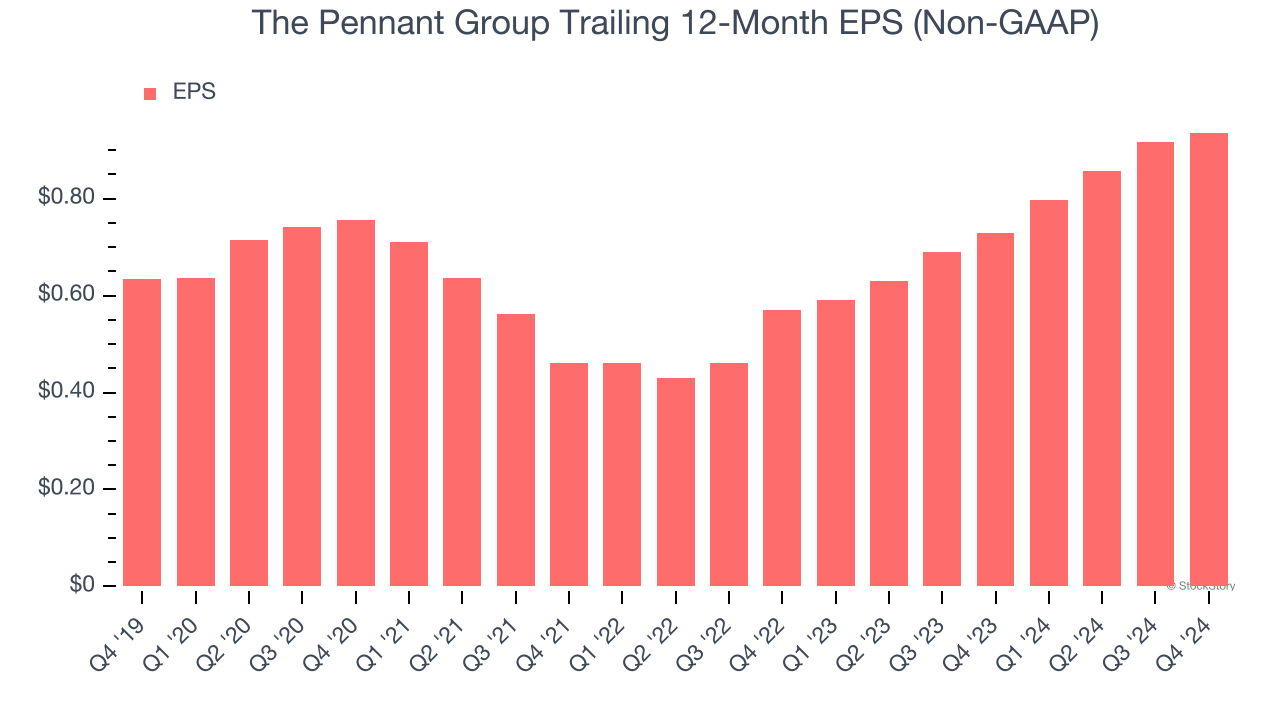

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

The Pennant Group’s EPS grew at a solid 8.1% compounded annual growth rate over the last five years. However, this performance was lower than its 15.5% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

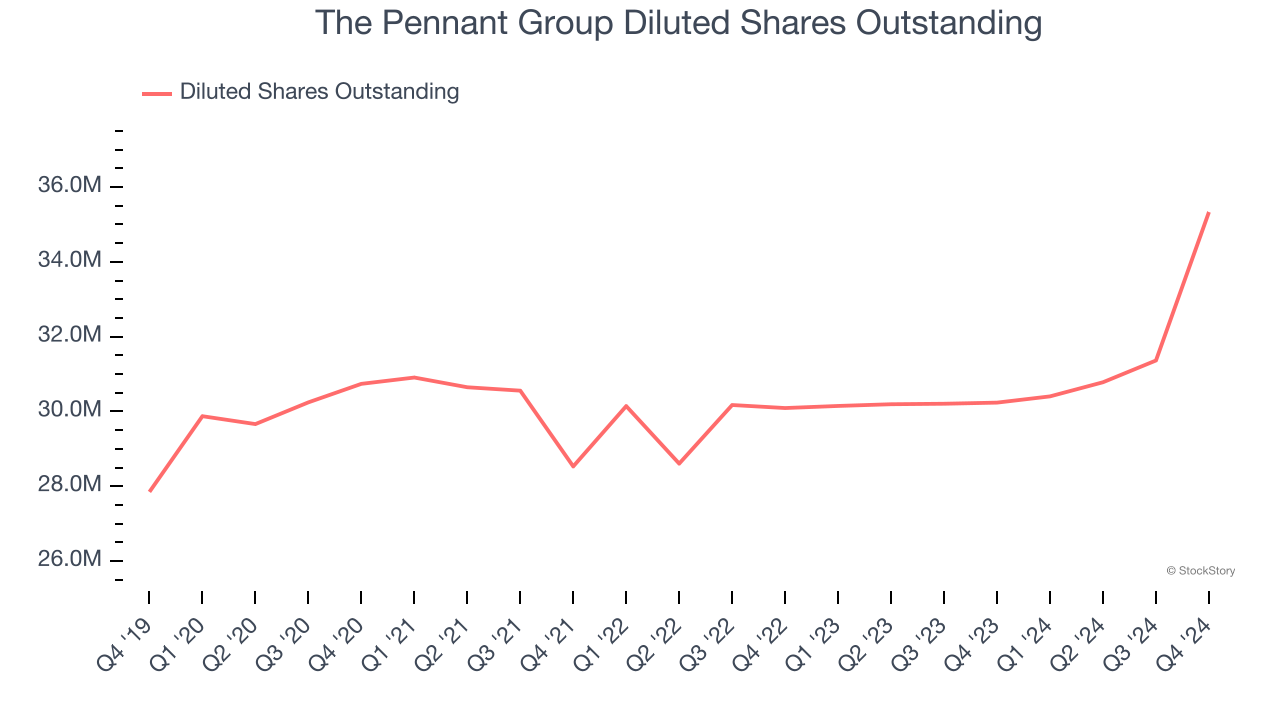

Diving into the nuances of The Pennant Group’s earnings can give us a better understanding of its performance. A five-year view shows The Pennant Group has diluted its shareholders, growing its share count by 26.9%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, The Pennant Group reported EPS at $0.24, up from $0.22 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects The Pennant Group’s full-year EPS of $0.94 to grow 16.4%.

Key Takeaways from The Pennant Group’s Q4 Results

We were impressed by how significantly The Pennant Group blew past analysts’ sales volume expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this quarter was mixed. The stock remained flat at $25.54 immediately following the results.

So should you invest in The Pennant Group right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.