Since August 2024, U-Haul has been in a holding pattern, floating around $70.39. The stock also fell short of the S&P 500’s 6.4% gain during that period.

Is there a buying opportunity in U-Haul, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on U-Haul for now. Here are three reasons why we avoid UHAL and a stock we'd rather own.

Why Do We Think U-Haul Will Underperform?

Founded by a husband and wife duo, U-Haul (NYSE:UHAL) is a provider of rental trucks and storage facilities.

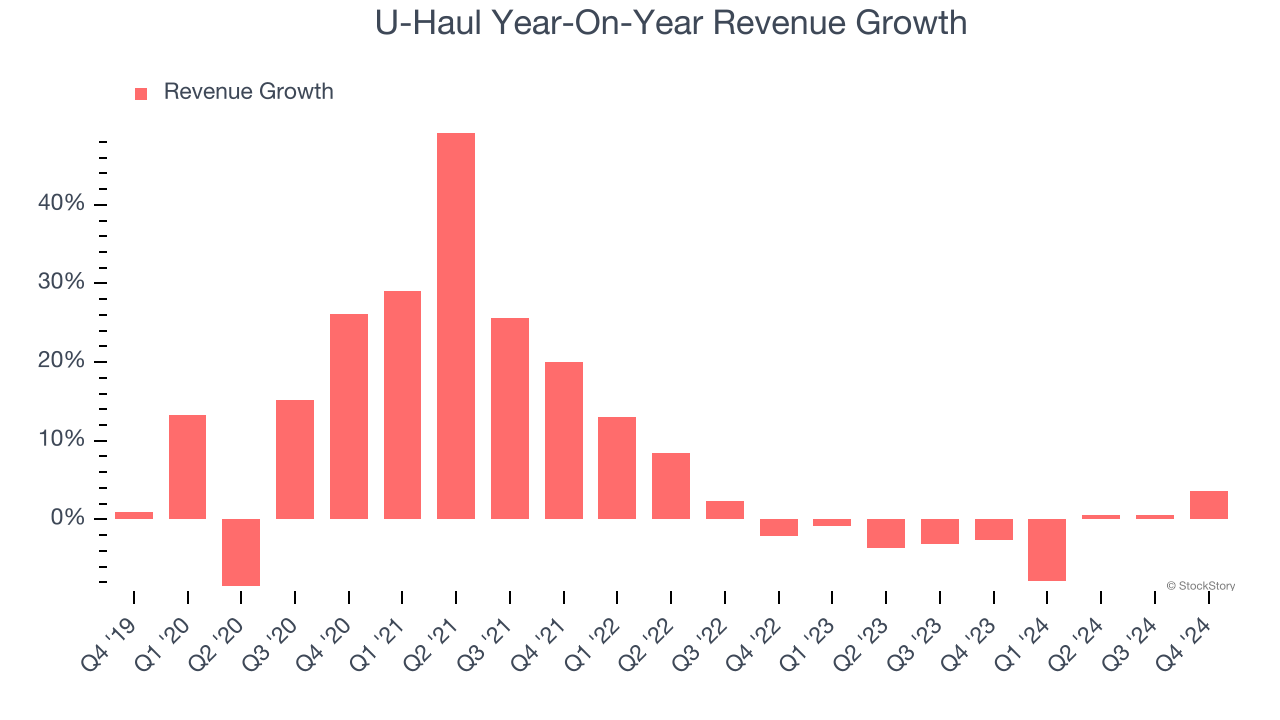

1. Revenue Tumbling Downwards

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. U-Haul’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.6% over the last two years. U-Haul isn’t alone in its struggles as the Ground Transportation industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

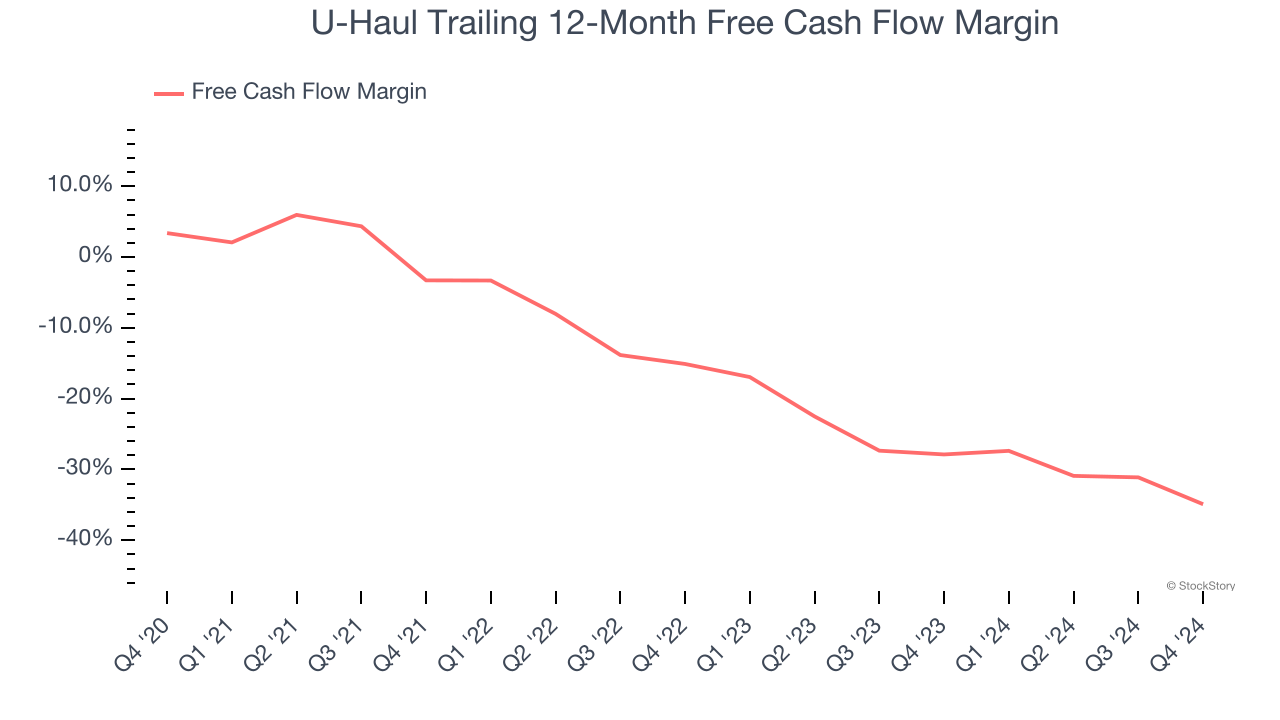

2. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, U-Haul’s margin dropped by 38.3 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business. U-Haul’s free cash flow margin for the trailing 12 months was negative 34.9%.

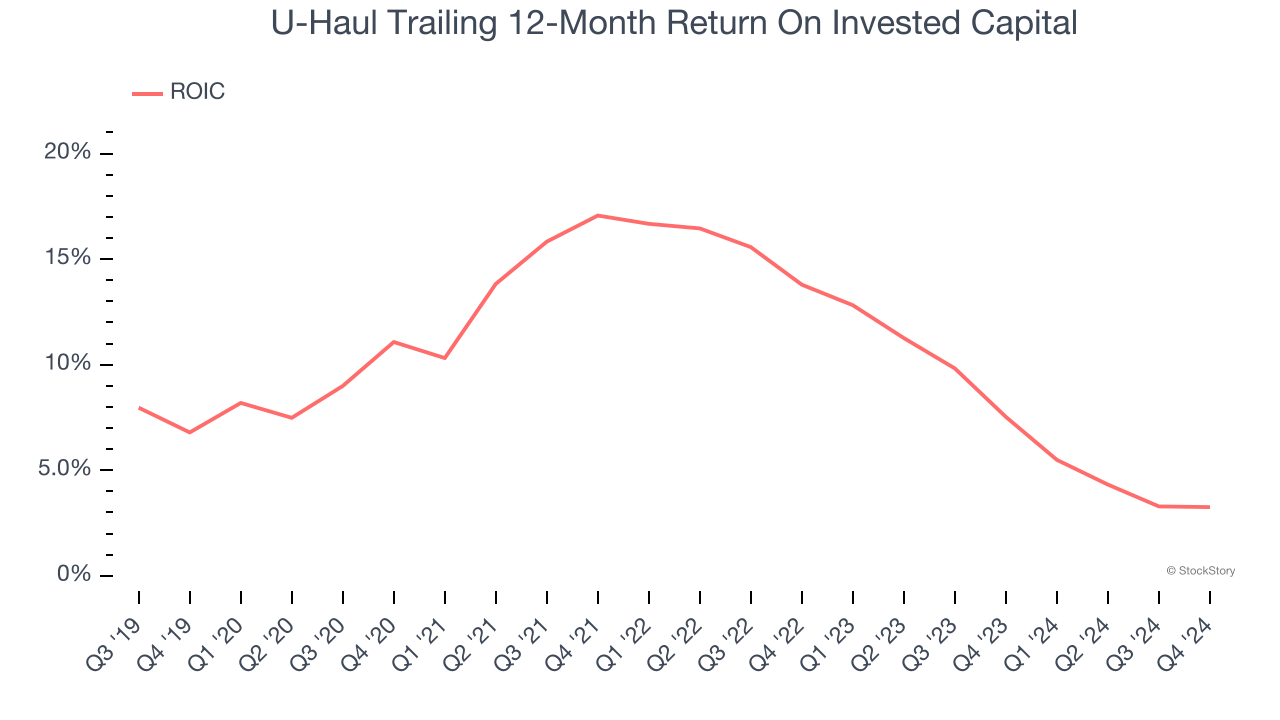

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, U-Haul’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

U-Haul falls short of our quality standards. With its shares lagging the market recently, the stock trades at $70.39 per share (or a 2.4× trailing 12-month price-to-sales ratio). The market typically values companies like U-Haul based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d recommend looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of U-Haul

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.