Over the past six months, Bristol-Myers Squibb has been a great trade, beating the S&P 500 by 13.7%. Its stock price has climbed to $58.28, representing a healthy 18.8% increase. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Bristol-Myers Squibb, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Bristol-Myers Squibb. Here are three reasons why BMY doesn't excite us and a stock we'd rather own.

Why Is Bristol-Myers Squibb Not Exciting?

Founded in 1887, Bristol-Myers Squibb (NYSE:BMY) is a global biopharmaceutical company that develops medicines to treat cancer, immune disorders, and cardiovascular conditions.

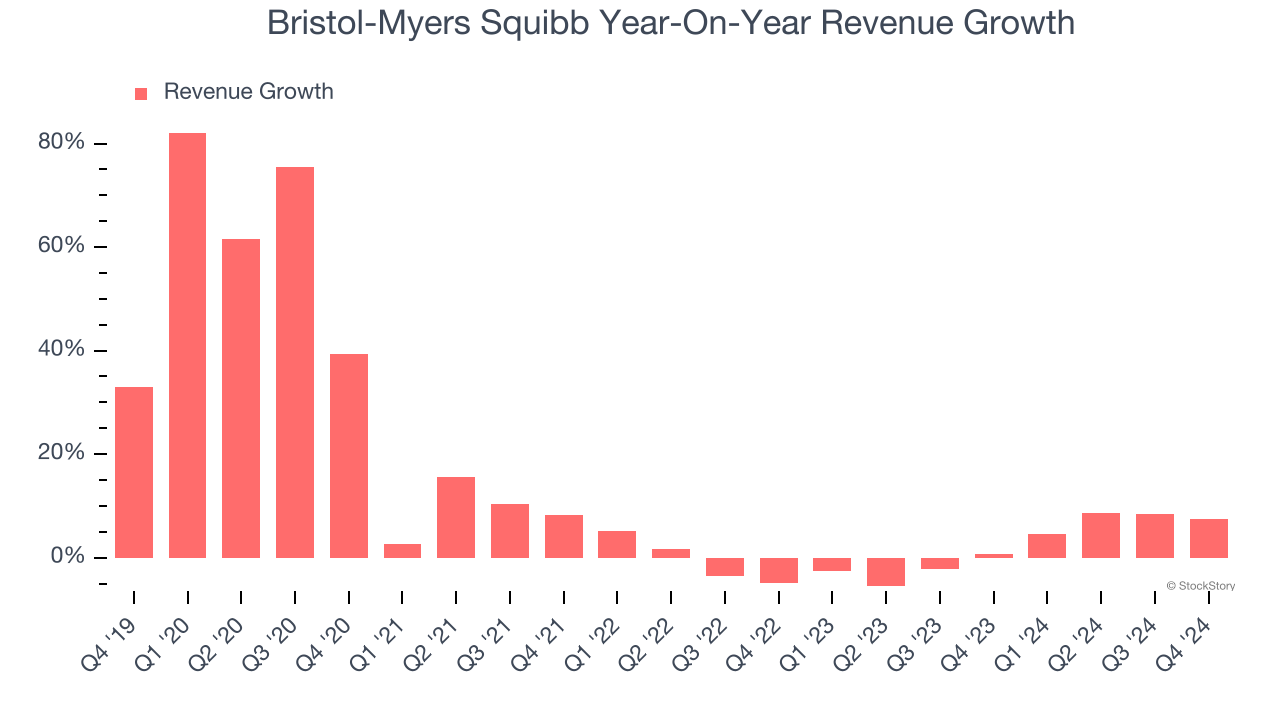

1. Lackluster Revenue Growth

Long-term growth is the most important, but within healthcare, a stretched historical view may miss new innovations or demand cycles. Bristol-Myers Squibb’s recent history shows its demand slowed as its annualized revenue growth of 2.3% over the last two years is below its five-year trend.

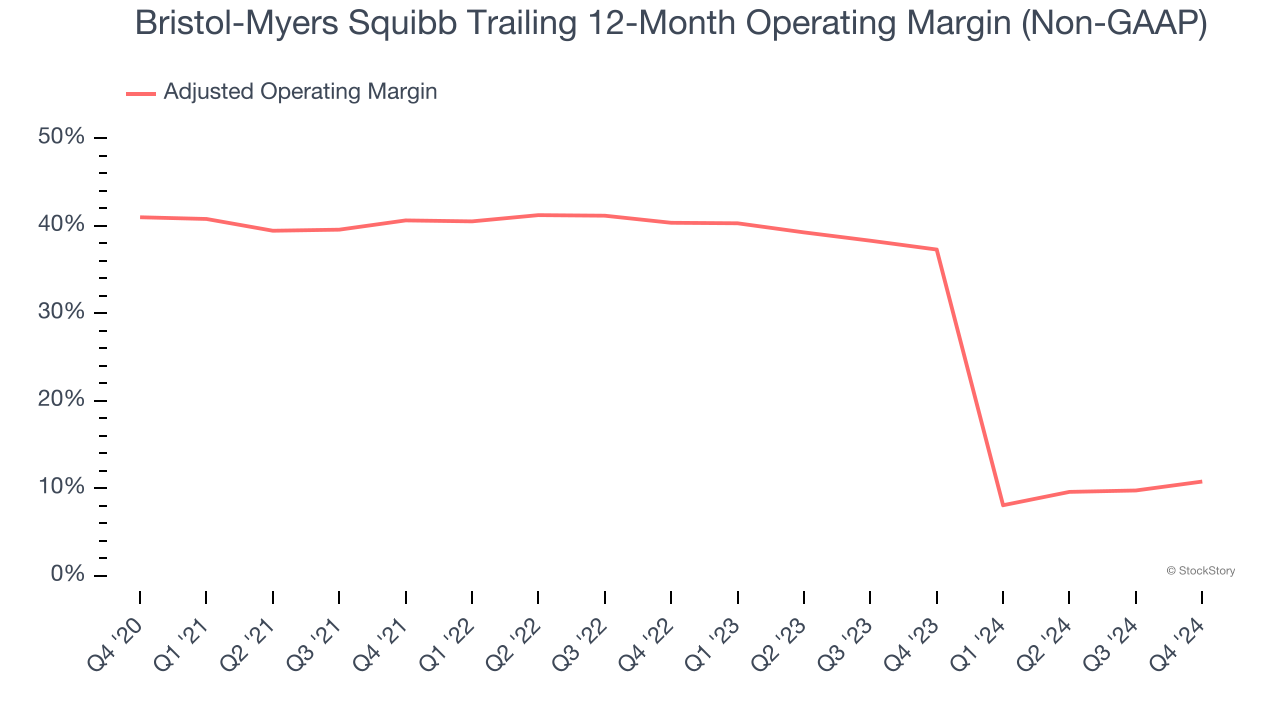

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Looking at the trend in its profitability, Bristol-Myers Squibb’s adjusted operating margin decreased by 30.2 percentage points over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 10.8%.

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Bristol-Myers Squibb, its EPS declined by 24.7% annually over the last five years while its revenue grew by 13.1%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Bristol-Myers Squibb isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 8.5× forward price-to-earnings (or $58.28 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Stocks We Would Buy Instead of Bristol-Myers Squibb

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.