Himax has been on fire lately. In the past six months alone, the company’s stock price has rocketed 67.4%, reaching $9.29 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Himax, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Despite the momentum, we're sitting this one out for now. Here are three reasons why HIMX doesn't excite us and a stock we'd rather own.

Why Is Himax Not Exciting?

Taiwan-based Himax Technologies (NASDAQ:HIMX) is a leading manufacturer of display driver chips and timing controllers used in TVs, laptops, and mobile phones.

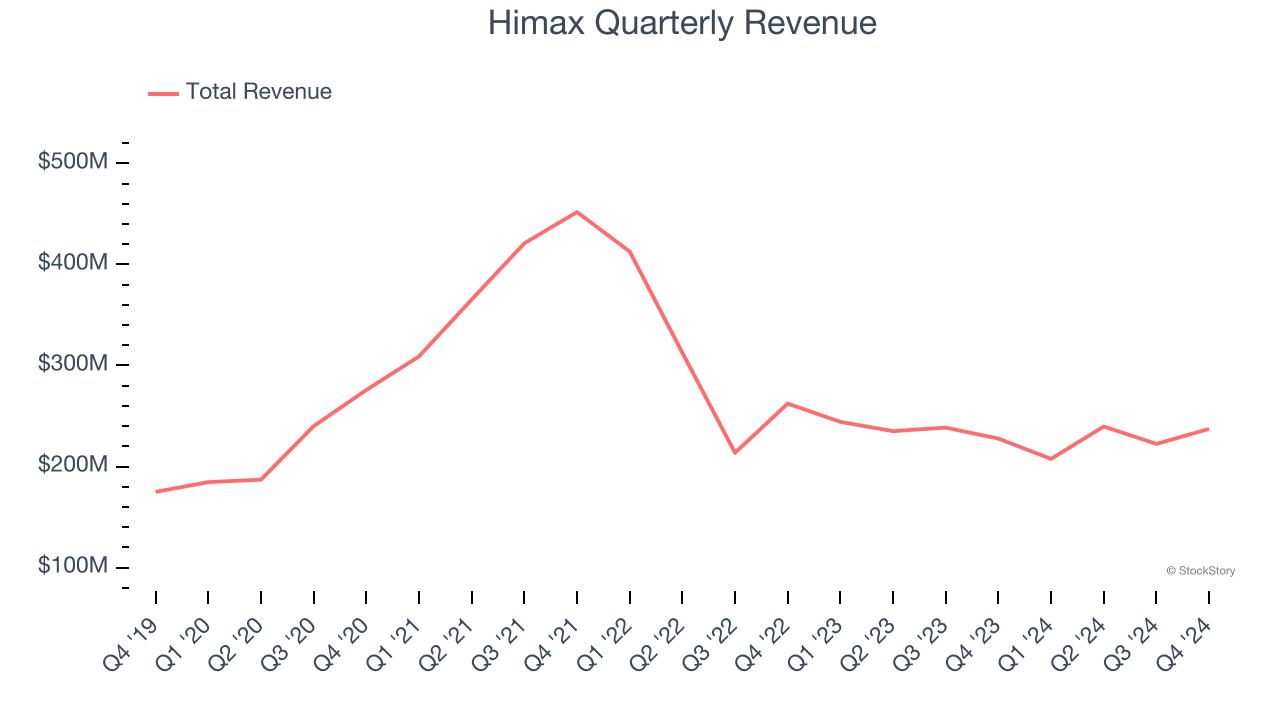

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Himax’s 6.2% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Himax’s revenue to drop by 15.5%, a decrease from its 13.1% annualized declines for the past two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

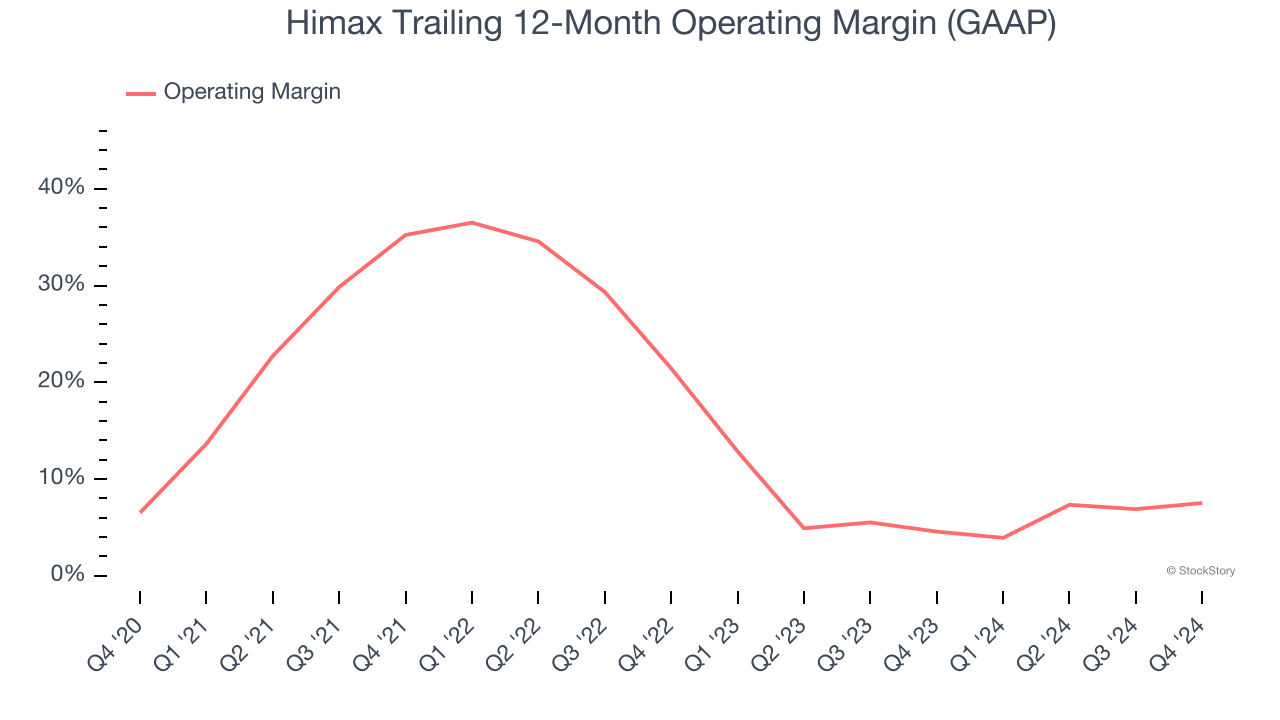

3. Weak Operating Margin Could Cause Trouble

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Himax was profitable over the last two years but held back by its large cost base. Its average operating margin of 6% was weak for a semiconductor business. This result isn’t too surprising given its low gross margin as a starting point.

Final Judgment

Himax isn’t a terrible business, but it doesn’t pass our bar. Following the recent rally, the stock trades at 46.5× forward price-to-earnings (or $9.29 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Himax

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.