Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Henry Schein (NASDAQ:HSIC) and the best and worst performers in the dental equipment & technology industry.

The dental equipment and technology industry encompasses companies that manufacture orthodontic products, dental implants, imaging systems, and digital tools for dental professionals. These companies benefit from recurring revenue streams tied to consumables, ongoing maintenance, and growing demand for aesthetic and restorative dentistry. However, high R&D costs, significant capital investment requirements, and reliance on discretionary spending make them vulnerable to economic cycles. Over the next few years, tailwinds for the sector include innovation in digital workflows, such as 3D printing and AI-driven diagnostics, which enhance the efficiency and precision of dental care. However, headwinds include economic uncertainty, which could reduce patient spending on elective procedures, regulatory challenges, and potential pricing pressures from consolidated dental service organizations (DSOs).

The 4 dental equipment & technology stocks we track reported a softer Q4. As a group, revenues missed analysts’ consensus estimates by 0.9% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11.9% since the latest earnings results.

Henry Schein (NASDAQ:HSIC)

Founded in 1932, Henry Schein (NASDAQ:HSIC) is a distributor of healthcare products and services, offering a broad portfolio of medical, dental, and veterinary supplies.

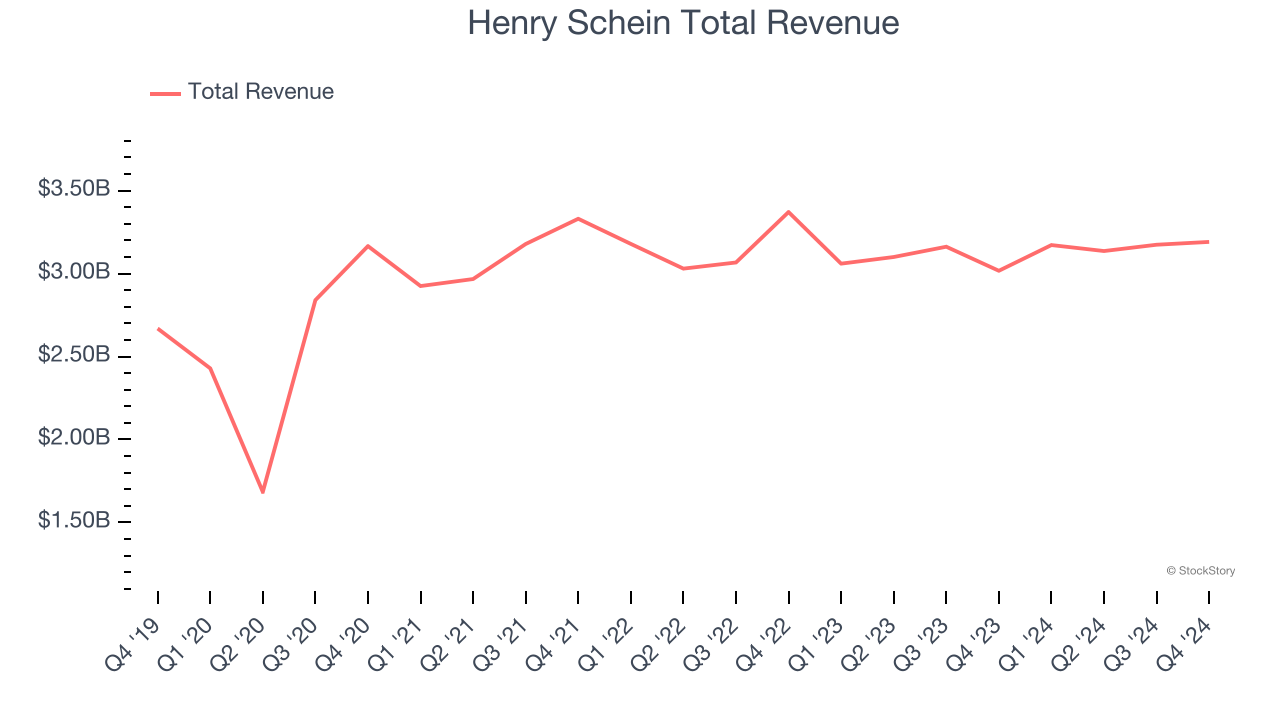

Henry Schein reported revenues of $3.19 billion, up 5.8% year on year. This print fell short of analysts’ expectations by 2.3%. Overall, it was a softer quarter for the company with a miss of analysts’ full-year EPS guidance estimates and a slight miss of analysts’ organic revenue estimates.

“Our fourth quarter financial results reflect relatively stable dental and medical end-markets. We continued to make progress on our 2022 to 2024 BOLD+1 Strategic Plan which we recently completed, exceeding our 2024 target of generating 40% of our worldwide operating income from high-growth, high-margin businesses,” said Stanley M. Bergman, Chairman of the Board and Chief Executive Officer of Henry Schein.

Henry Schein pulled off the fastest revenue growth but had the weakest performance against analyst estimates of the whole group. Still, the market seems discontent with the results. The stock is down 19.1% since reporting and currently trades at $72.07.

Read our full report on Henry Schein here, it’s free.

Best Q4: Align Technology (NASDAQ:ALGN)

Founded in 1997, Align Technology (NASDAQ:ALGN) specializes in clear aligner therapy and digital dental solutions, offering products like the Invisalign system for teeth straightening and iTero scanners for precise digital imaging.

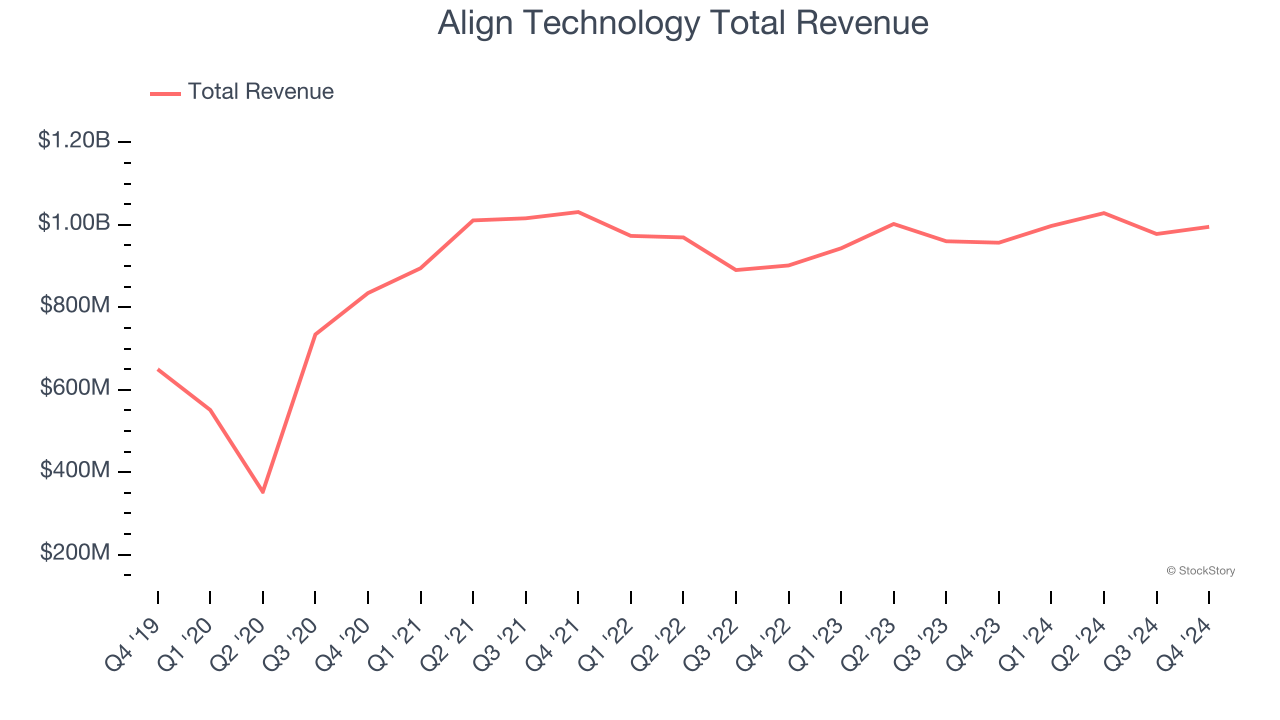

Align Technology reported revenues of $995.2 million, up 4% year on year, in line with analysts’ expectations. The business performed better than its peers, but it was unfortunately a slower quarter with revenue guidance for next quarter meeting analysts’ expectations and EPS in line with analysts’ estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 19.1% since reporting. It currently trades at $175.20.

Is now the time to buy Align Technology? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Dentsply Sirona (NASDAQ:XRAY)

Founded in 1899, Dentsply Sirona (NASDAQ:XRAY) is a leading manufacturer of dental equipment, consumables, and technology solutions.

Dentsply Sirona reported revenues of $905 million, down 10.6% year on year, falling short of analysts’ expectations by 1.6%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations and a significant miss of analysts’ EPS estimates.

Dentsply Sirona delivered the slowest revenue growth in the group. As expected, the stock is down 13.9% since the results and currently trades at $16.22.

Read our full analysis of Dentsply Sirona’s results here.

Envista (NYSE:NVST)

Spun off from Danaher in 2019, Envista Holdings (NYSE:NVST) designs, manufactures, and markets a wide range of dental solutions, including diagnostic tools, implants, orthodontics, and consumables.

Envista reported revenues of $652.9 million, up 1.1% year on year. This print topped analysts’ expectations by 0.8%. More broadly, it was a slower quarter as it recorded a significant miss of analysts’ full-year EPS guidance estimates.

Envista delivered the biggest analyst estimates beat among its peers. The stock is down 7.6% since reporting and currently trades at $19.02.

Read our full, actionable report on Envista here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.